- Australia

- /

- Metals and Mining

- /

- ASX:PLG

Pearl Gull Iron (ASX:PLG) delivers shareholders 1.6% return over 1 year, surging 10% in the last week alone

It's nice to see the Pearl Gull Iron Limited (ASX:PLG) share price up 10% in a week. But in truth the last year hasn't been good for the share price. After all, the share price is down 11% in the last year, significantly under-performing the market.

Although the past week has been more reassuring for shareholders, they're still in the red over the last year, so let's see if the underlying business has been responsible for the decline.

View our latest analysis for Pearl Gull Iron

SWOT Analysis for Pearl Gull Iron

- Currently debt free.

- Shareholders have been diluted in the past year.

- PLG's financial characteristics indicate limited near-term opportunities for shareholders.

- Lack of analyst coverage makes it difficult to determine PLG's earnings prospects.

- Has less than 3 years of cash runway based on current free cash flow.

Pearl Gull Iron hasn't yet reported any revenue, so it's as much a business idea as an actual business. You have to wonder why venture capitalists aren't funding it. So it seems shareholders are too busy dreaming about the progress to come than dwelling on the current (lack of) revenue. For example, investors may be hoping that Pearl Gull Iron finds some valuable resources, before it runs out of money.

We think companies that have neither significant revenues nor profits are pretty high risk. There is almost always a chance they will need to raise more capital, and their progress - and share price - will dictate how dilutive that is to current holders. While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt.

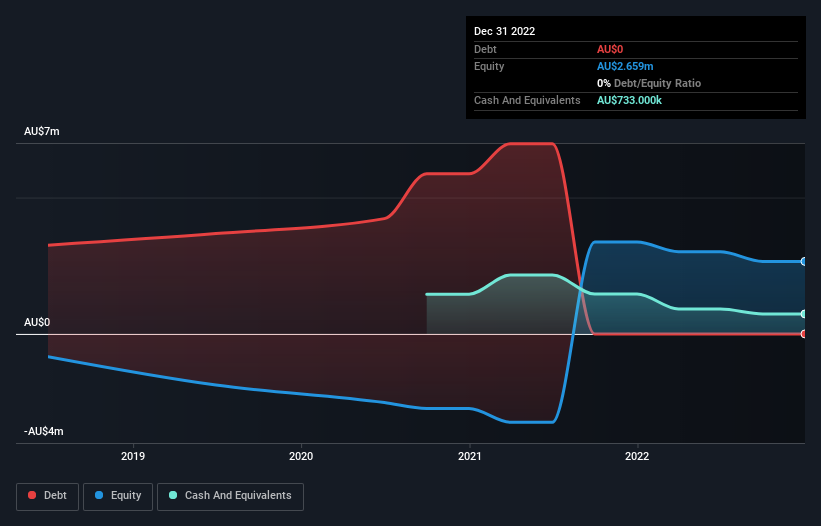

Our data indicates that Pearl Gull Iron had AU$7.0m more in total liabilities than it had cash, when it last reported in December 2022. That puts it in the highest risk category, according to our analysis. But with the share price diving 11% in the last year , it's probably fair to say that some shareholders no longer believe the company will succeed. The image below shows how Pearl Gull Iron's balance sheet has changed over time; if you want to see the precise values, simply click on the image.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. Would it bother you if insiders were selling the stock? I'd like that just about as much as I like to drink milk and fruit juice mixed together. It costs nothing but a moment of your time to see if we are picking up on any insider selling.

What About The Total Shareholder Return (TSR)?

We've already covered Pearl Gull Iron's share price action, but we should also mention its total shareholder return (TSR). Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. We note that Pearl Gull Iron's TSR, at 1.6% is higher than its share price return of -11%. When you consider it hasn't been paying a dividend, this data suggests shareholders have benefitted from a spin-off, or had the opportunity to acquire attractively priced shares in a discounted capital raising.

A Different Perspective

Pearl Gull Iron shareholders have gained 1.6% for the year. The bad news is that's no better than the average market return, which was roughly 4.1%. The stock trailed the market by 20% in that time, testament to the power of passive investing. It might be that investors are more concerned about the business lately due to some fundamental change (or else the share price simply got ahead of itself, previously). It's always interesting to track share price performance over the longer term. But to understand Pearl Gull Iron better, we need to consider many other factors. For instance, we've identified 6 warning signs for Pearl Gull Iron that you should be aware of.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PLG

Pearl Gull Iron

A mineral exploration company, focuses on exploration and development of iron ore properties in Australia.

Slight with imperfect balance sheet.

Market Insights

Community Narratives