- Australia

- /

- Metals and Mining

- /

- ASX:AKE

Analyst Estimates: Here's What Brokers Think Of Orocobre Limited (ASX:ORE) After Its Half-Yearly Report

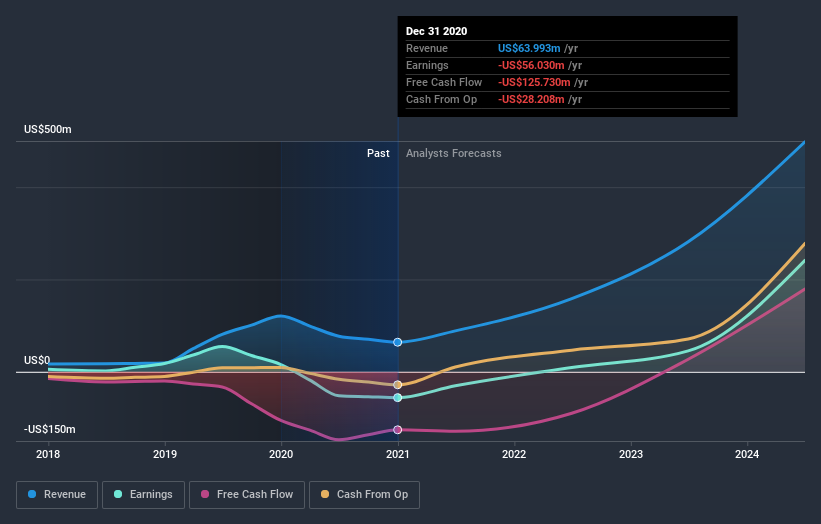

Orocobre Limited (ASX:ORE) shareholders are probably feeling a little disappointed, since its shares fell 8.3% to AU$4.66 in the week after its latest interim results. The result was fairly weak overall, with revenues of US$35m being 9.2% less than what the analysts had been modelling. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Orocobre

After the latest results, the eight analysts covering Orocobre are now predicting revenues of US$88.7m in 2021. If met, this would reflect a huge 39% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 50% to US$0.095. Before this latest report, the consensus had been expecting revenues of US$91.5m and US$0.071 per share in losses. So it's pretty clear the analysts have mixed opinions on Orocobre after this update; revenues were downgraded and per-share losses expected to increase.

The average price target was broadly unchanged at AU$5.15, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Orocobre analyst has a price target of AU$7.30 per share, while the most pessimistic values it at AU$2.00. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely different views on what kind of performance this business can generate. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Orocobre's past performance and to peers in the same industry. Next year brings more of the same, according to the analysts, with revenue forecast to grow 39%, in line with its 39% annual growth over the past five years. Compare this with the wider industry (in aggregate), which analyst estimates suggest will see revenues fall 3.1% next year. So not only is Orocobre expected to maintain its revenue growth despite the wider downturn, it's also forecast to grow faster than the industry as a whole.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Orocobre analysts - going out to 2024, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Orocobre , and understanding them should be part of your investment process.

When trading Orocobre or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Allkem, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:AKE

Allkem

Allkem Limited engages in the production and sale of lithium and boron in Argentina.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives