- Australia

- /

- Specialty Stores

- /

- ASX:TPW

Exploring Three ASX Growth Companies With Significant Insider Ownership

Reviewed by Simply Wall St

In the past year, the Australian market has shown a positive trajectory with an 8.2% increase, while remaining stable over the last seven days. In this context of expected annual earnings growth of 14%, stocks with high insider ownership can be particularly appealing as they often indicate confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 29.9% |

| Gratifii (ASX:GTI) | 14.9% | 112.4% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Doctor Care Anywhere Group (ASX:DOC) | 28.4% | 96.4% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Change Financial (ASX:CCA) | 26.6% | 85.4% |

| Botanix Pharmaceuticals (ASX:BOT) | 11.4% | 120.9% |

| Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

Let's explore several standout options from the results in the screener.

Mesoblast (ASX:MSB)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mesoblast Limited, operating in Australia, the United States, Singapore, and Switzerland, focuses on developing regenerative medicine products with a market capitalization of approximately A$1.24 billion.

Operations: The company generates revenue primarily from its development of adult stem cell technology platform, totaling A$7.47 million.

Insider Ownership: 22.2%

Mesoblast, a growth company in Australia with high insider ownership, has shown a highly volatile share price recently. Despite shareholder dilution over the past year, insider activities have been positive with more substantial buying than selling. The company's revenue growth is forecasted at 55.3% annually, outpacing the Australian market significantly. Mesoblast is expected to become profitable within three years, supported by an earnings growth forecast of 56.65% per year. Recent leadership changes and significant regulatory advancements highlight its strategic efforts to stabilize and grow further.

- Delve into the full analysis future growth report here for a deeper understanding of Mesoblast.

- Insights from our recent valuation report point to the potential undervaluation of Mesoblast shares in the market.

Ora Banda Mining (ASX:OBM)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ora Banda Mining Limited is an Australian company focused on the exploration, operation, and development of mineral properties, with a market capitalization of approximately A$686.94 million.

Operations: The company generates revenue primarily from its gold mining activities, totaling A$166.66 million.

Insider Ownership: 10.2%

Ora Banda Mining, recently added to the S&P/ASX All Ordinaries Index, reported a significant turnaround with half-year sales reaching A$96.35 million and net income of A$10.79 million, contrasting sharply with last year's loss. The company is poised for robust growth with revenue expected to increase by 41.9% annually, outperforming the broader Australian market's 5.4% growth rate. Despite past shareholder dilution, Ora Banda is trading at a substantial discount to its estimated fair value and forecasts indicate profitability within three years.

- Click here to discover the nuances of Ora Banda Mining with our detailed analytical future growth report.

- According our valuation report, there's an indication that Ora Banda Mining's share price might be on the cheaper side.

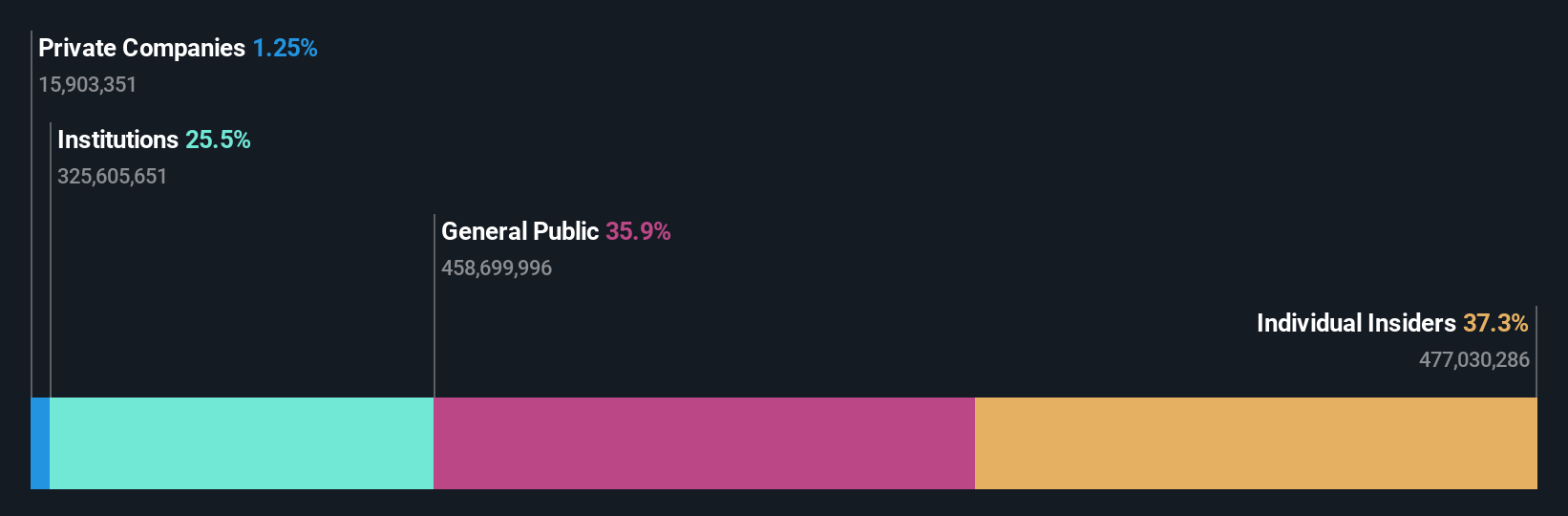

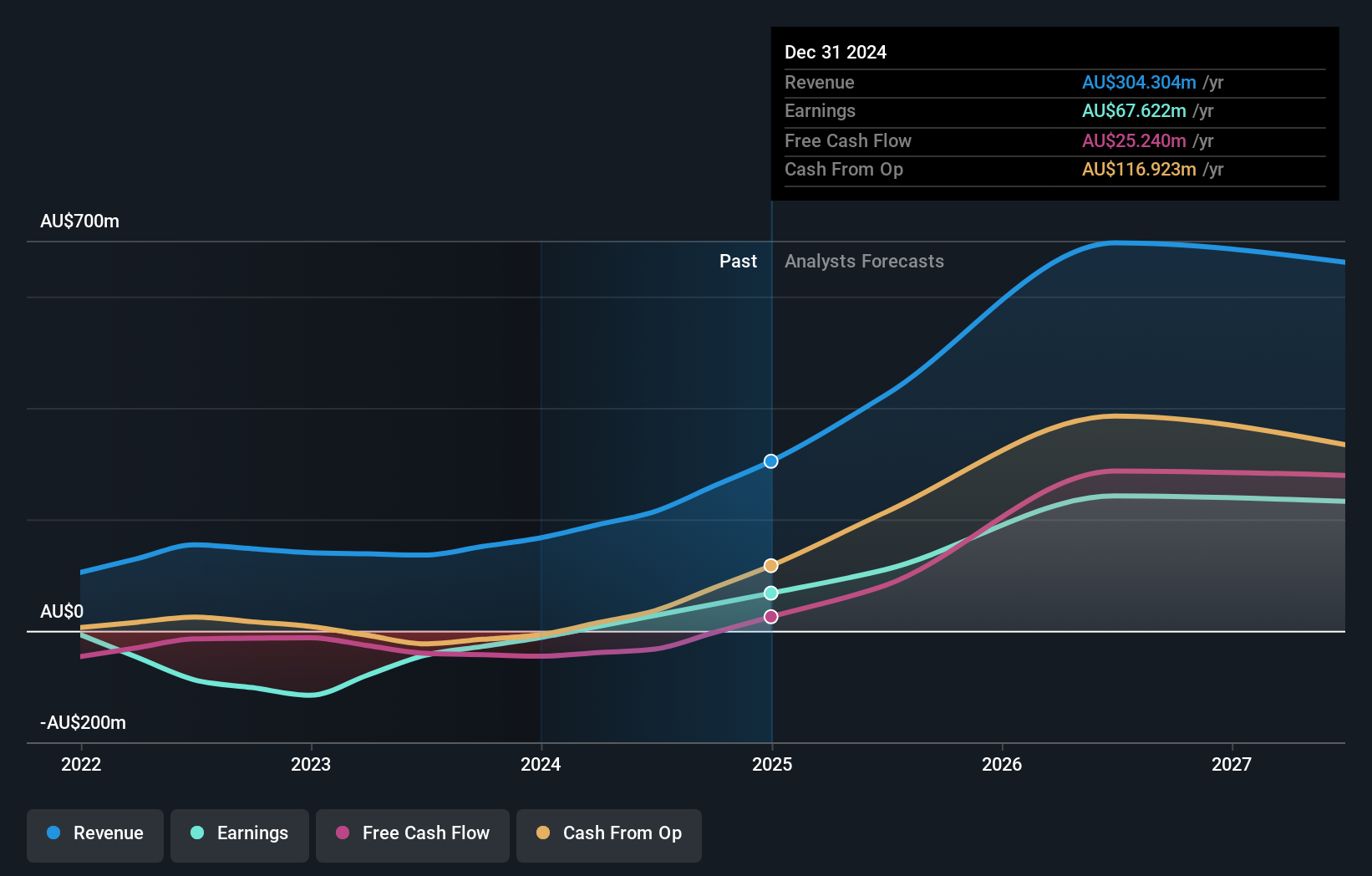

Temple & Webster Group (ASX:TPW)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Temple & Webster Group Ltd operates as an online retailer specializing in furniture, homewares, and home improvement products across Australia, with a market capitalization of approximately A$1.19 billion.

Operations: The company's revenue, totaling A$442.25 million, primarily derives from the online sales of furniture, homewares, and home improvement items.

Insider Ownership: 12.9%

Temple & Webster Group is projected to experience robust growth, with earnings expected to increase by 35.08% annually and revenue forecasted to grow at 20.9% per year, outpacing the Australian market's average. However, its Return on Equity is anticipated to be low at 19.4% in three years. Recent strategic moves include a share buyback program where up to A$30 million worth of shares will be repurchased and cancelled by May 2025, aiming for effective capital management and supporting growth opportunities.

- Dive into the specifics of Temple & Webster Group here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential overvaluation of Temple & Webster Group shares in the market.

Make It Happen

- Click this link to deep-dive into the 90 companies within our Fast Growing ASX Companies With High Insider Ownership screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Temple & Webster Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TPW

Temple & Webster Group

Engages in the online retail of furniture, homewares, and home improvement products in Australia.

Flawless balance sheet with high growth potential.