Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:NST

Will Northern Star Resources’ (ASX:NST) Steady Guidance Signal Enduring Cost Control Confidence?

Simply Wall St

Reviewed by Sasha Jovanovic

- Northern Star Resources Limited recently released its operating results for the September 2025 quarter, reporting sales of 381,000 ounces of gold at an all-in sustaining cost of A$2,522 per ounce, and reaffirmed its fiscal year 2026 guidance for total gold sold and costs.

- Despite mixed quarterly production performance, management’s decision to uphold full-year targets highlights ongoing confidence in operational stability and cost control initiatives.

- We’ll explore how the reaffirmed full-year gold production guidance shapes Northern Star’s investment narrative and future project outlook.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Northern Star Resources Investment Narrative Recap

At its core, holding Northern Star Resources stock is about confidence in the company’s ability to deliver consistent gold production while maintaining cost discipline during periods of sector-wide inflation. The latest quarterly results, with reaffirmed full-year guidance despite mixed production, do not materially impact the immediate focus: sustaining output at key assets and managing cost pressures, while the main risk continues to be successful execution and integration of large-scale expansion projects.

Among recent announcements, the confirmation of fiscal year 2026 production and cost guidance stands out as most relevant. This assurance, following a quarter with both operational positives and challenges, reinforces the company’s emphasis on stability and operational reliability, important for supporting longer-term objectives such as the Fimiston mill expansion and the Hemi project ramp-up.

Yet, in contrast to steady guidance, investors should be aware of ongoing uncertainties tied to capital project execution and...

Read the full narrative on Northern Star Resources (it's free!)

Northern Star Resources is forecast to achieve A$9.1 billion in revenue and A$2.0 billion in earnings by 2028. This outlook assumes annual revenue growth of 12.3% and a rise in earnings of A$0.7 billion from current earnings of A$1.3 billion.

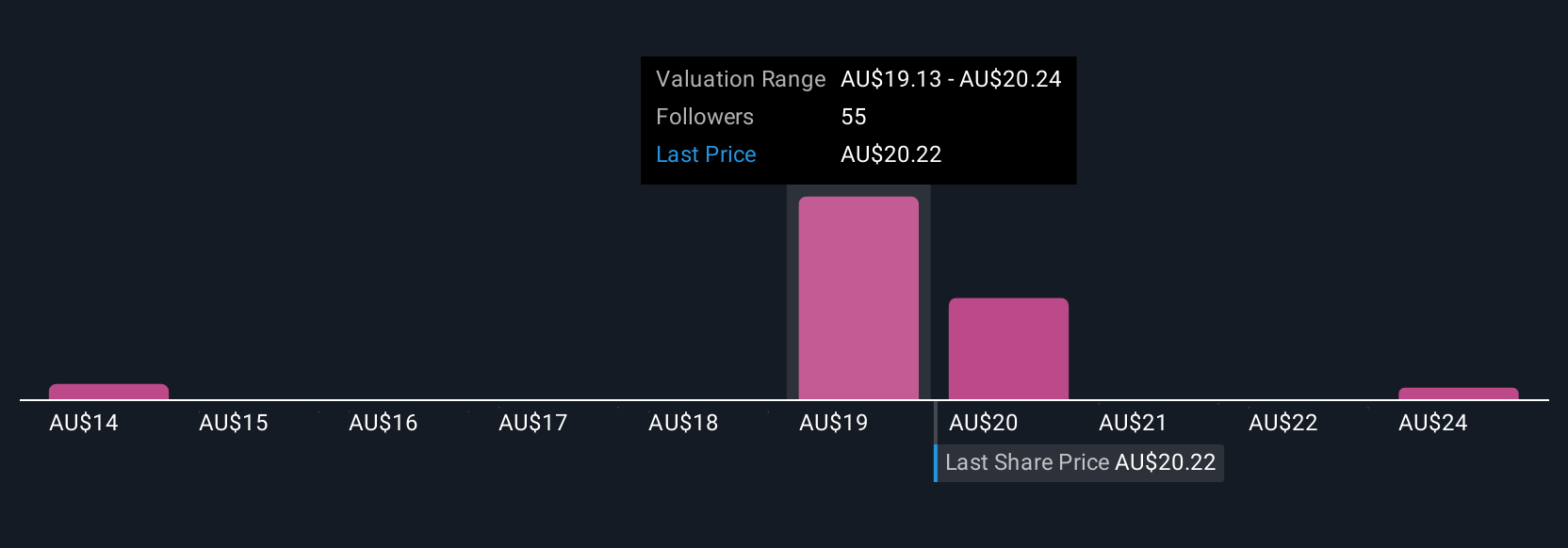

Uncover how Northern Star Resources' forecasts yield a A$25.11 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Thirteen estimates from the Simply Wall St Community indicate fair values between A$13.56 and A$46.34 per share. While opinions are diverse, the reaffirmed 2026 production outlook underscores how closely near-term guidance can shape expectations for Northern Star’s future performance. Explore these differing viewpoints to see how your outlook compares.

Explore 13 other fair value estimates on Northern Star Resources - why the stock might be worth 44% less than the current price!

Build Your Own Northern Star Resources Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Northern Star Resources research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Northern Star Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Northern Star Resources' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Northern Star Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:NST

Northern Star Resources

Engages in the exploration, development, mining, and processing of gold deposits.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor