- Australia

- /

- Metals and Mining

- /

- ASX:LTR

Liontown Resources (ASX:LTR): Evaluating Valuation After Major Capital Raise and New Share Issuance

Reviewed by Simply Wall St

Liontown Resources (ASX:LTR) has just concluded a sizable capital raising, securing over A$56 million by issuing more than 76 million new shares at A$0.73 each. Completed follow-on equity offerings often spark debate among investors, especially given their immediate impact on a company's share count and the potential implications for future growth projects. For those watching Liontown’s next move, this capital raise may be interpreted both as a vote of confidence in expansion plans and as a new test of market sentiment.

The timing of this offering is notable. Liontown’s stock climbed 6% over the past day and has increased by 69% in the last three months, outpacing much of the local mining sector. Even over the past year, shares have posted a 25% gain, suggesting ongoing momentum despite the considerable share dilution. This influx of new capital follows a year marked by swings in commodity prices and changing risk perceptions across Australia’s mining space. Liontown has managed to keep investors engaged with its ambitious growth forecasts and improving top-line results.

With new shares entering the market and recent gains accumulating, some may ask whether Liontown is undervalued after the raise or if the market is already factoring in significant expectations for future developments.

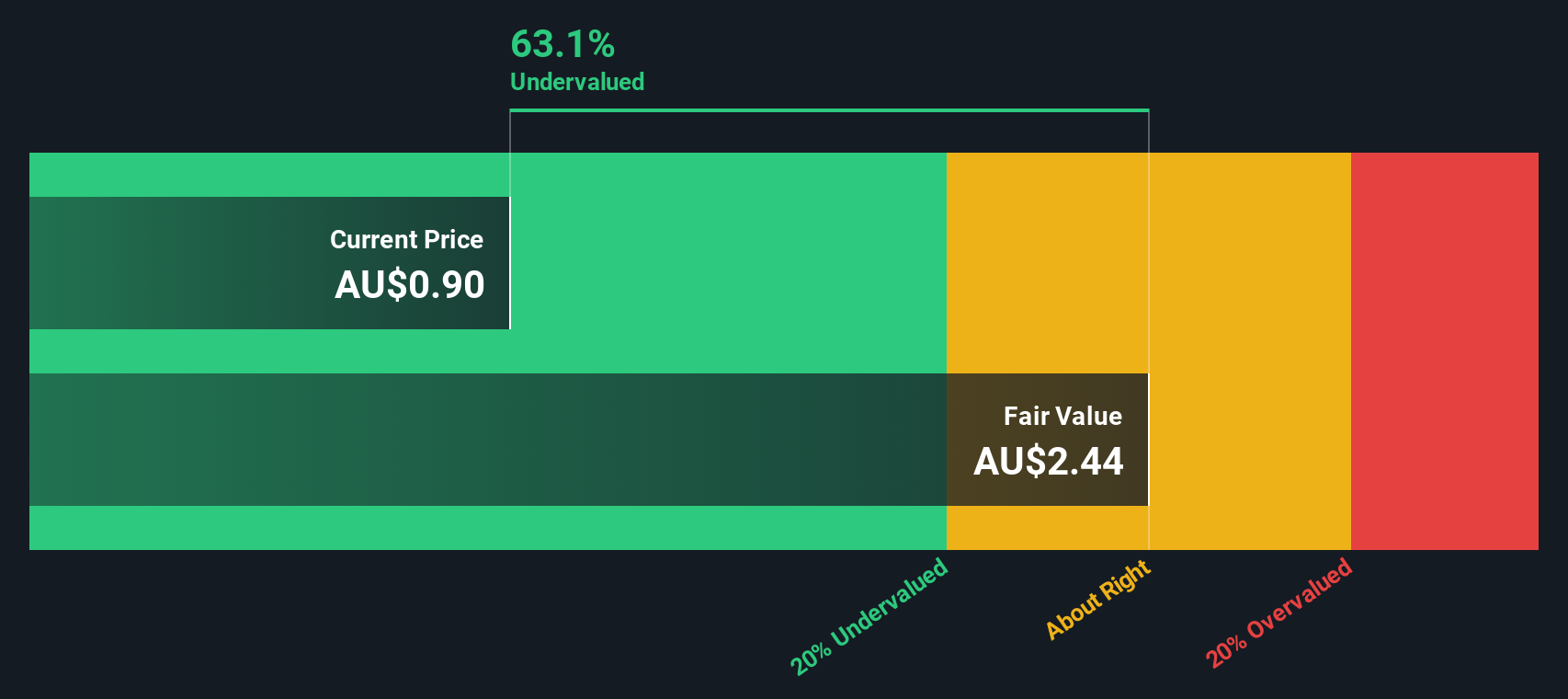

Most Popular Narrative: 51% Overvalued

According to analyst consensus, Liontown Resources is currently trading at a significant premium to its fair value. The prevailing outlook suggests that, while the business has compelling growth forecasts, market expectations may have run too far ahead of fundamentals.

"Analysts are assuming Liontown Resources's revenue will grow by 92.7% annually over the next 3 years. Analysts assume that profit margins will increase from -48.8% today to 6.7% in 3 years time."

Curious about what is driving this bold analyst call? The key factor is rapid revenue growth and a turnaround in profitability that is unusual for a miner. You might wonder what profit multiple is being used to justify such a high price. The answer may be surprising, and it is worth exploring how these aggressive targets are combined.

Result: Fair Value of $0.62 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising lithium competition and higher underground operating costs could undermine Liontown’s optimistic forecasts. These factors may create headwinds for its revenue and profit outlook.

Find out about the key risks to this Liontown Resources narrative.Another View: What Does the DCF Model Show?

While analysts think Liontown is expensive based on market ratios, our SWS DCF model suggests a completely different outcome. According to this approach, the shares might actually be undervalued. Can a cash flow view really tell a different story?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Liontown Resources Narrative

If you have a different take or want to dive deeper into the numbers, you can build your own Liontown Resources narrative in just a couple of minutes. Do it your way

A great starting point for your Liontown Resources research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Don’t limit yourself to one story. Expand your portfolio by targeting trends others might miss. Simply Wall Street’s advanced screener makes it easy to uncover stocks with big potential. Here’s where your next smart move could start:

- Accelerate your strategy with bargain shares by using our tool for undervalued stocks based on cash flows. This highlights companies trading below intrinsic value and ready for savvy investors to act.

- Harness the wave of medical innovation and tap into healthcare AI stocks to find leaders blending artificial intelligence with healthcare for future-shaping results and strong potential.

- Boost your income stream and secure long-term gains by accessing picks in dividend stocks with yields > 3%, featuring stocks delivering attractive yields over 3% for consistent earnings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About ASX:LTR

Liontown

Engages in the exploration, evaluation, and development of mineral properties in Australia.

High growth potential and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion