Advertisement

- Australia

- /

- Basic Materials

- /

- ASX:JHX

3 ASX Stocks Estimated To Be Up To 42.8% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

Amidst recent market fluctuations, with Australian shares poised for a potential bounceback following one of the toughest trading days of 2025, investors are eyeing opportunities on the ASX. In such volatile times, identifying stocks that are perceived to be undervalued can be particularly appealing, offering potential value against current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Acrow (ASX:ACF) | A$1.09 | A$2.01 | 45.8% |

| Nido Education (ASX:NDO) | A$0.795 | A$1.57 | 49.3% |

| Nick Scali (ASX:NCK) | A$15.69 | A$27.51 | 43% |

| Environmental Group (ASX:EGL) | A$0.245 | A$0.46 | 46.9% |

| PolyNovo (ASX:PNV) | A$1.165 | A$2.12 | 44.9% |

| Charter Hall Group (ASX:CHC) | A$16.78 | A$31.89 | 47.4% |

| Genetic Signatures (ASX:GSS) | A$0.475 | A$0.88 | 45.8% |

| SciDev (ASX:SDV) | A$0.445 | A$0.82 | 45.5% |

| ReadyTech Holdings (ASX:RDY) | A$2.60 | A$5.13 | 49.3% |

| Polymetals Resources (ASX:POL) | A$0.87 | A$1.69 | 48.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

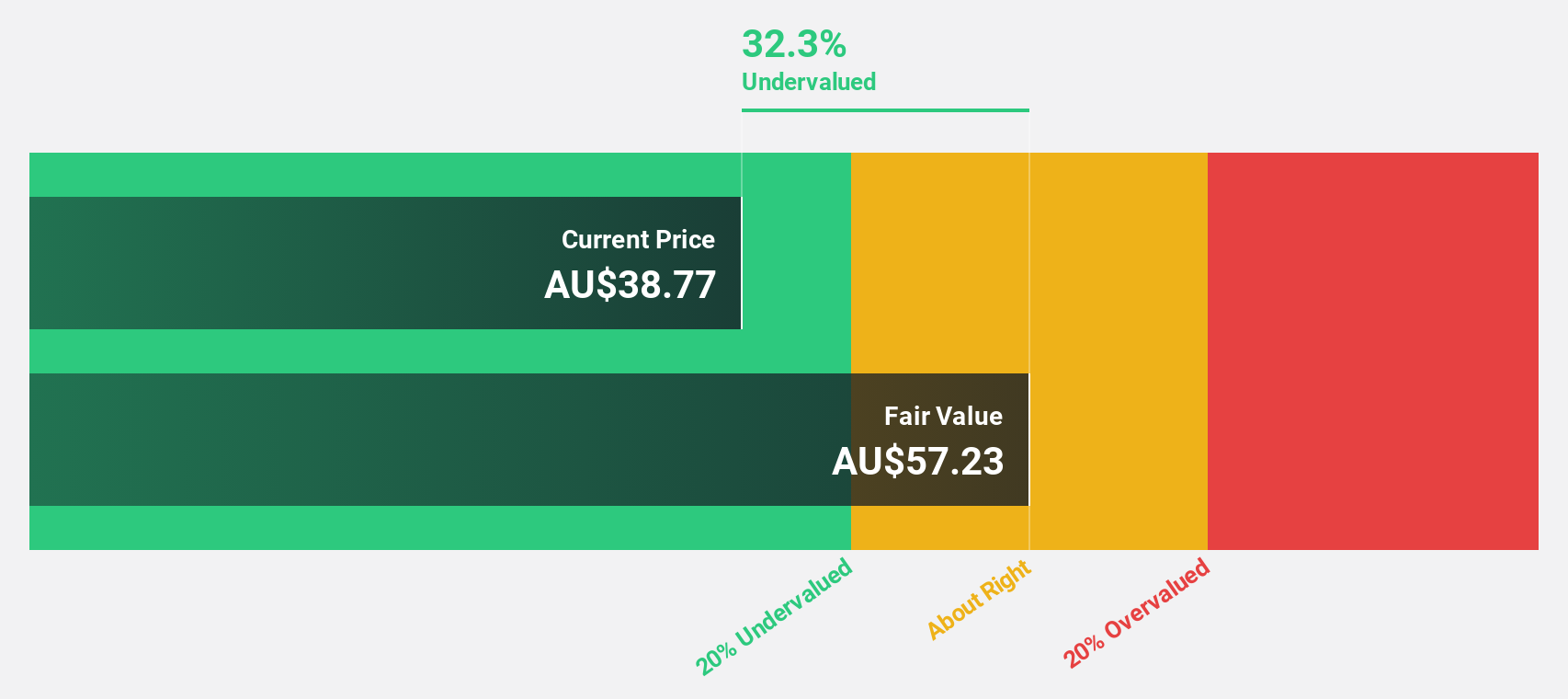

Integral Diagnostics (ASX:IDX)

Overview: Integral Diagnostics Limited is a healthcare services company that provides diagnostic imaging services to medical professionals and patients in Australia and New Zealand, with a market cap of A$843.54 million.

Operations: Revenue for Integral Diagnostics is primarily generated from the operation of diagnostic imaging facilities, amounting to A$491.32 million.

Estimated Discount To Fair Value: 42.8%

Integral Diagnostics (IDX) is trading at A$2.27, significantly below its estimated fair value of A$3.97, suggesting it may be undervalued based on cash flows. Despite a recent net loss of A$0.396 million for H1 2025, IDX's earnings are expected to grow substantially over the next three years at 40.2% per year, outpacing the Australian market's growth rate of 11.8%. However, interest payments are not well covered by earnings and private equity interest remains high following a drop in market value to A$837 million after recent results.

- Insights from our recent growth report point to a promising forecast for Integral Diagnostics' business outlook.

- Click to explore a detailed breakdown of our findings in Integral Diagnostics' balance sheet health report.

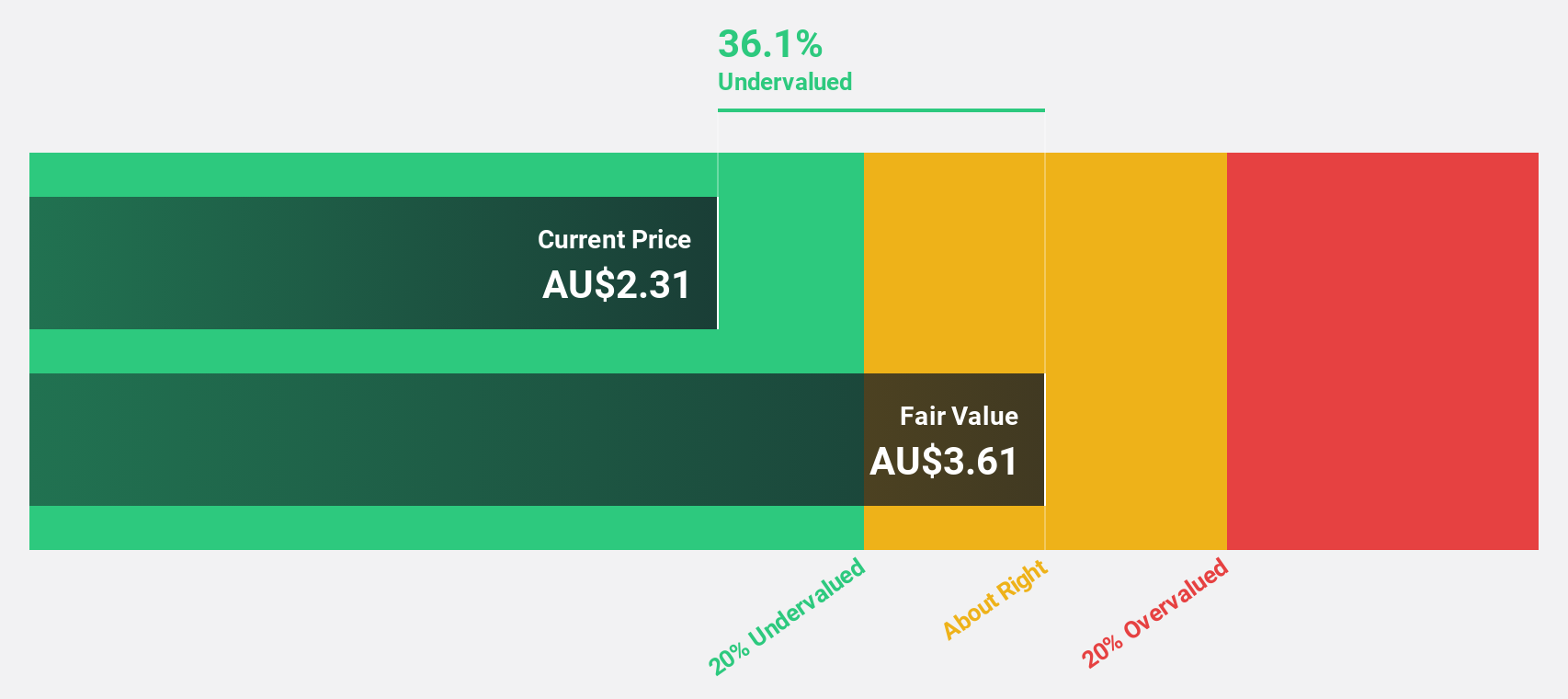

James Hardie Industries (ASX:JHX)

Overview: James Hardie Industries plc manufactures and sells fiber cement, fiber gypsum, and cement bonded building products for construction applications across the United States, Australia, Europe, New Zealand, and the Philippines with a market cap of A$15.89 billion.

Operations: The company's revenue segments are comprised of North America Fiber Cement at $2.88 billion, Asia Pacific Fiber Cement at $543.30 million, and Europe Building Products at $488 million.

Estimated Discount To Fair Value: 34.4%

James Hardie Industries, trading at A$36.98, is substantially below its estimated fair value of A$56.41, highlighting potential undervaluation based on cash flows. The company's earnings are projected to grow annually by 18.1%, outpacing the Australian market's 11.8% growth rate. Recent acquisition plans with The AZEK Company Inc., alongside a strategic partnership with David Weekley Homes, could enhance long-term growth prospects despite recent stable earnings performance and slight revenue decline year-over-year.

- Our growth report here indicates James Hardie Industries may be poised for an improving outlook.

- Click here to discover the nuances of James Hardie Industries with our detailed financial health report.

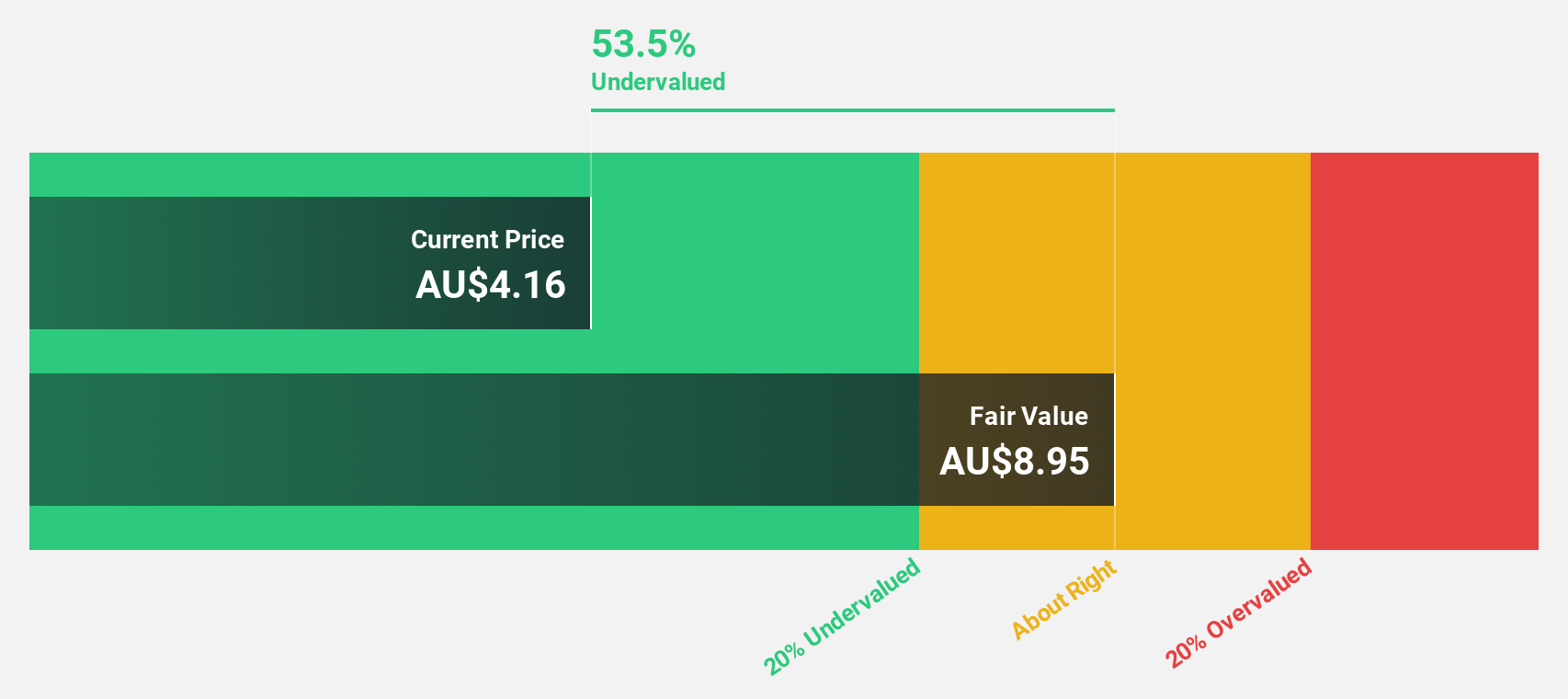

Select Harvests (ASX:SHV)

Overview: Select Harvests Limited is an Australian company involved in the cultivation, processing, packaging, and sale of almonds and its by-products, with a market cap of A$724.75 million.

Operations: The company's revenue is primarily derived from its almond segment, which generated A$337.29 million.

Estimated Discount To Fair Value: 18.3%

Select Harvests, trading at A$5.1, is undervalued compared to its fair value estimate of A$6.24 and offers significant earnings growth potential with a forecasted 34.3% annual increase, surpassing the Australian market's 11.8%. Despite recent shareholder dilution and large one-off items affecting earnings quality, revenue is expected to grow faster than the market at 9% annually. Recent executive changes include appointing Liam Nolan as CFO and Mark Rhys Davies as Joint Company Secretaries.

- The analysis detailed in our Select Harvests growth report hints at robust future financial performance.

- Navigate through the intricacies of Select Harvests with our comprehensive financial health report here.

Summing It All Up

- Discover the full array of 40 Undervalued ASX Stocks Based On Cash Flows right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:JHX

James Hardie Industries

Engages in the manufacture and sale of fiber cement, fiber gypsum, and cement bonded boards in the United States, Australia, Europe, and New Zealand.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor