Advertisement

Rob Bills has been the CEO of Emmerson Resources Limited (ASX:ERM) since 2007, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

See our latest analysis for Emmerson Resources

How Does Total Compensation For Rob Bills Compare With Other Companies In The Industry?

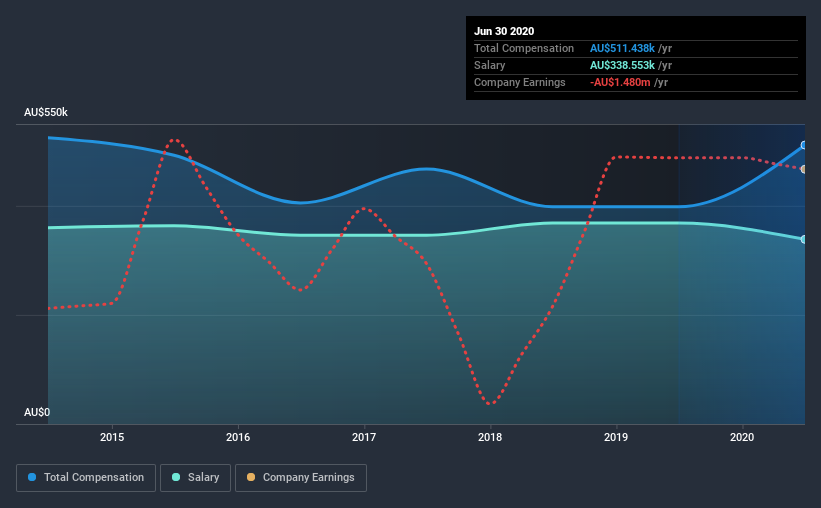

At the time of writing, our data shows that Emmerson Resources Limited has a market capitalization of AU$37m, and reported total annual CEO compensation of AU$511k for the year to June 2020. Notably, that's an increase of 28% over the year before. Notably, the salary which is AU$338.6k, represents most of the total compensation being paid.

For comparison, other companies in the industry with market capitalizations below AU$260m, reported a median total CEO compensation of AU$311k. Accordingly, our analysis reveals that Emmerson Resources Limited pays Rob Bills north of the industry median. Furthermore, Rob Bills directly owns AU$589k worth of shares in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$339k | AU$368k | 66% |

| Other | AU$173k | AU$30k | 34% |

| Total Compensation | AU$511k | AU$398k | 100% |

On an industry level, around 69% of total compensation represents salary and 31% is other remuneration. There isn't a significant difference between Emmerson Resources and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Emmerson Resources Limited's Growth Numbers

Emmerson Resources Limited has seen its earnings per share (EPS) increase by 60% a year over the past three years. It achieved revenue growth of 75% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Emmerson Resources Limited Been A Good Investment?

Given the total shareholder loss of 21% over three years, many shareholders in Emmerson Resources Limited are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be lessto generous with CEO compensation.

In Summary...

As we noted earlier, Emmerson Resources pays its CEO higher than the norm for similar-sized companies belonging to the same industry. But the company has impressed with its EPS growth, but we cannot say the same about the uninspiring shareholder returns (over the last three years). Considering overall performance, we can't say Rob is underpaid, in fact compensation is definitely on the higher side.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 3 warning signs for Emmerson Resources you should be aware of, and 1 of them is potentially serious.

Switching gears from Emmerson Resources, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

When trading Emmerson Resources or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emmerson Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:ERM

Emmerson Resources

Engages in the exploration and evaluation of mineral properties.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative