Stock Analysis

- Australia

- /

- Hospitality

- /

- ASX:FLT

ASX Growth Companies With High Insider Ownership And Up To 26% Earnings Growth

Reviewed by Simply Wall St

Over the past year, the Australian market has shown a modest uptick, increasing by 6.2%, although it has remained flat over the last 7 days. In this context of moderate growth and positive earnings forecasts, companies with high insider ownership can be particularly appealing as they often indicate a strong alignment between company management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 30.1% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Doctor Care Anywhere Group (ASX:DOC) | 28.4% | 96.4% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Change Financial (ASX:CCA) | 26.6% | 85.4% |

| Botanix Pharmaceuticals (ASX:BOT) | 11.4% | 120.9% |

| Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

| Argosy Minerals (ASX:AGY) | 14.5% | 129.6% |

Here we highlight a subset of our preferred stocks from the screener.

Capricorn Metals (ASX:CMM)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Capricorn Metals Ltd is an Australian company focused on the evaluation, exploration, development, and production of gold properties, with a market capitalization of approximately A$1.82 billion.

Operations: The company generates its revenue primarily from the Karlawinda segment, totaling A$356.94 million.

Insider Ownership: 12.3%

Earnings Growth Forecast: 26.5% p.a.

Capricorn Metals, a growth-focused company in Australia, exhibits mixed signals regarding insider ownership and financial performance. Despite substantial insider buying activity recently, the company's profit margins have declined from 25.4% to 5.2%. However, Capricorn Metals is expected to outpace the Australian market with its revenue growth forecast at 14.1% per year and earnings anticipated to increase by a significant 26.5% annually, showcasing robust potential for future profitability despite current margin pressures.

- Navigate through the intricacies of Capricorn Metals with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Capricorn Metals is priced higher than what may be justified by its financials.

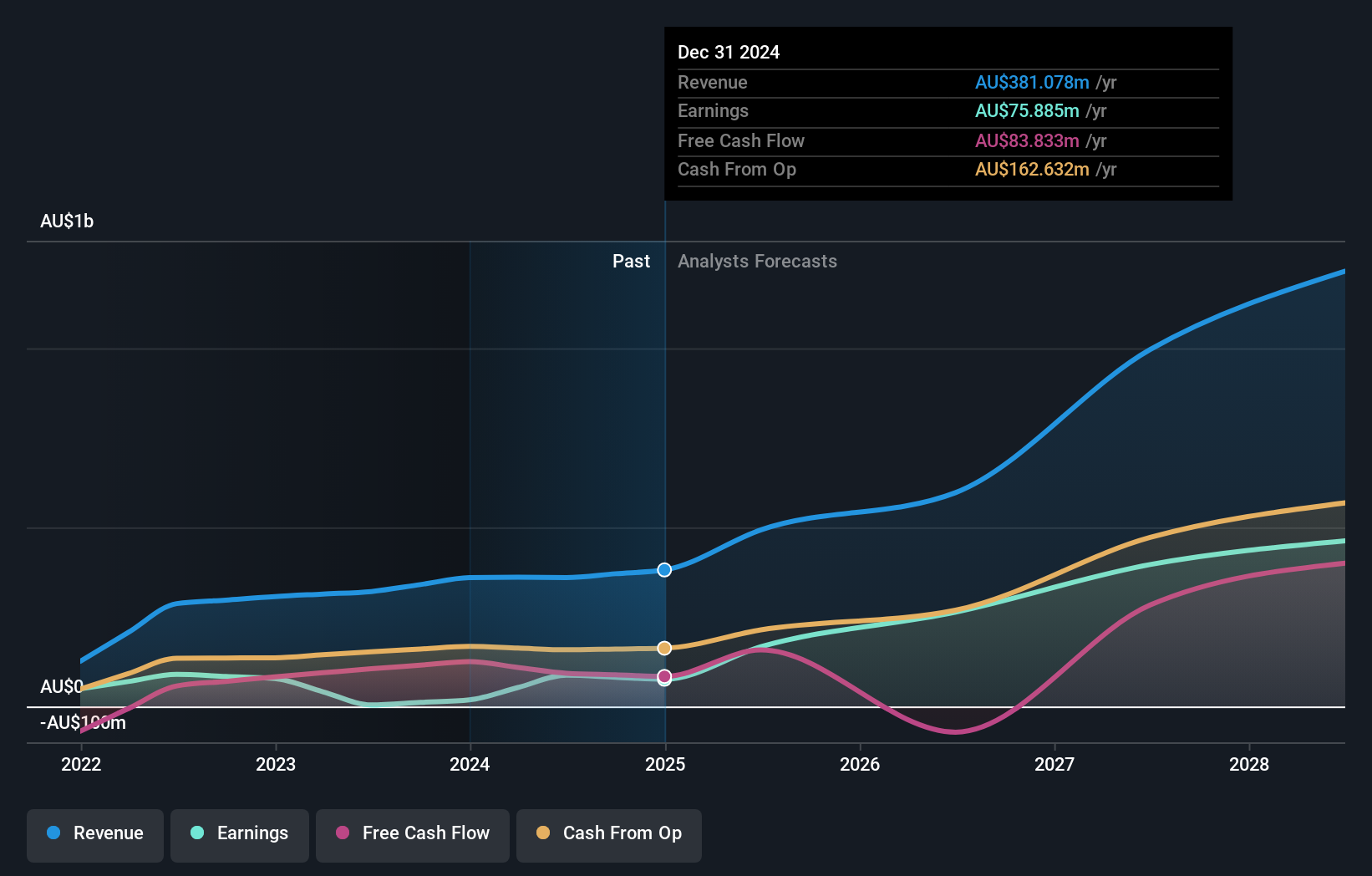

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across various regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of approximately A$4.37 billion.

Operations: The company generates revenue primarily through its leisure and corporate travel segments, with A$1.28 billion from leisure and A$1.06 billion from corporate services.

Insider Ownership: 13.3%

Earnings Growth Forecast: 18.8% p.a.

Flight Centre Travel Group, while trading 20.8% below its estimated fair value, shows promising financial forecasts with earnings expected to grow by 18.81% annually and revenue projected to increase at 9.7% per year—both metrics outpacing the Australian market averages of 13.7% and 5.4%, respectively. Despite this growth, the company's revenue growth does not meet the high benchmark of over 20%. Additionally, there is no recent insider trading data available to gauge current sentiment among insiders directly.

- Click to explore a detailed breakdown of our findings in Flight Centre Travel Group's earnings growth report.

- Upon reviewing our latest valuation report, Flight Centre Travel Group's share price might be too pessimistic.

Technology One (ASX:TNE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Technology One Limited is a company that develops, markets, sells, implements, and supports integrated enterprise business software solutions both in Australia and internationally, with a market capitalization of approximately A$5.96 billion.

Operations: The company generates revenue through three primary segments: Software (A$317.24 million), Corporate (A$83.83 million), and Consulting (A$68.13 million).

Insider Ownership: 12.3%

Earnings Growth Forecast: 14.3% p.a.

Technology One, a growth-oriented firm with high insider ownership, reported a substantial increase in half-year revenue to A$240.83 million and net income to A$48 million. This performance underscores its solid growth trajectory, with earnings expected to rise by 14.3% annually—slightly above the Australian market average. Despite this positive outlook, its revenue growth of 11.1% per year, although surpassing the market average of 5.4%, remains below the high-growth benchmark of 20%. The company's return on equity is also projected to be robust at 32.6% in three years' time, reflecting efficient management and potentially lucrative returns for shareholders.

- Get an in-depth perspective on Technology One's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Technology One's share price might be on the expensive side.

Turning Ideas Into Actions

- Take a closer look at our Fast Growing ASX Companies With High Insider Ownership list of 92 companies by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Flight Centre Travel Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Excellent balance sheet with reasonable growth potential.