- Australia

- /

- Metals and Mining

- /

- ASX:CIA

Champion Iron Full Year 2024 Earnings: EPS Beats Expectations, Revenues Lag

Champion Iron (ASX:CIA) Full Year 2024 Results

Key Financial Results

- Revenue: CA$1.52b (up 9.3% from FY 2023).

- Net income: CA$234.2m (up 17% from FY 2023).

- Profit margin: 15% (up from 14% in FY 2023). The increase in margin was driven by higher revenue.

- EPS: CA$0.45 (up from CA$0.39 in FY 2023).

CIA Production and Reserves

Iron- Production: 14.16 Mt (11.19 Mt in FY 2023)

- Proved and probable reserves (ore): 1,798 Mt (1,695 Mt in FY 2023)

- Number of mines: 1 (1 in FY 2023)

All figures shown in the chart above are for the trailing 12 month (TTM) period

Champion Iron EPS Beats Expectations, Revenues Fall Short

Revenue missed analyst estimates by 1.7%. Earnings per share (EPS) exceeded analyst estimates by 1.5%.

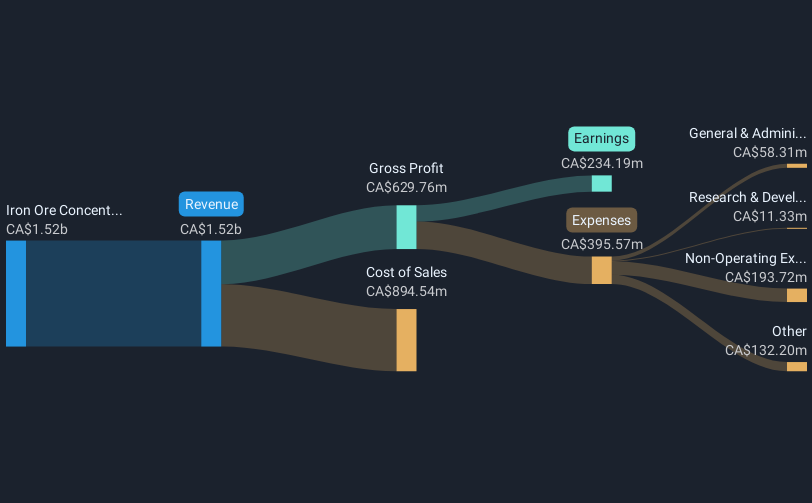

In the last 12 months, the only revenue segment was Iron Ore Concentrate contributing CA$1.52b. Notably, cost of sales worth CA$894.5m amounted to 59% of total revenue thereby underscoring the impact on earnings. The most substantial expense, totaling CA$193.7m were related to Non-Operating costs. This indicates that a significant portion of the company's costs is related to non-core activities. Explore how CIA's revenue and expenses shape its earnings.

Looking ahead, revenue is forecast to grow 3.7% p.a. on average during the next 3 years, while revenues in the Metals and Mining industry in Australia are expected to remain flat.

Performance of the Australian Metals and Mining industry.

The company's shares are down 7.0% from a week ago.

Valuation

Our analysis of these results suggests Champion Iron may be undervalued based on 6 important criteria we look at. You can access our in-depth analysis and discover what the outlook is like for the stock by clicking here.

If you're looking to trade Champion Iron, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CIA

Champion Iron

Engages in the acquisition, exploration, development, and production of iron ore deposits in Canada.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives