- Australia

- /

- Metals and Mining

- /

- ASX:AUC

Ausgold Limited (ASX:AUC) surges 13%; retail investors who own 57% shares profited along with institutions

Key Insights

- Significant control over Ausgold by retail investors implies that the general public has more power to influence management and governance-related decisions

- A total of 21 investors have a majority stake in the company with 43% ownership

- 33% of Ausgold is held by Institutions

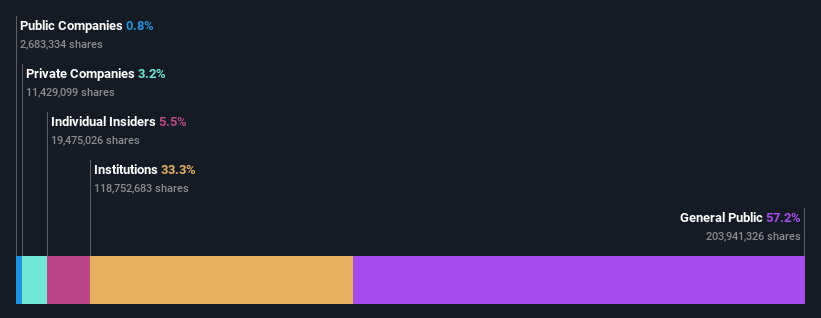

To get a sense of who is truly in control of Ausgold Limited (ASX:AUC), it is important to understand the ownership structure of the business. And the group that holds the biggest piece of the pie are retail investors with 57% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

While retail investors were the group that benefitted the most from last week’s AU$20m market cap gain, institutions too had a 33% share in those profits.

In the chart below, we zoom in on the different ownership groups of Ausgold.

View our latest analysis for Ausgold

What Does The Institutional Ownership Tell Us About Ausgold?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

We can see that Ausgold does have institutional investors; and they hold a good portion of the company's stock. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. If multiple institutions change their view on a stock at the same time, you could see the share price drop fast. It's therefore worth looking at Ausgold's earnings history below. Of course, the future is what really matters.

We note that hedge funds don't have a meaningful investment in Ausgold. Looking at our data, we can see that the largest shareholder is Jupiter Fund Management Plc with 13% of shares outstanding. With 11% and 4.7% of the shares outstanding respectively, Dundee Resources Limited and Franklin Resources, Inc. are the second and third largest shareholders.

On studying our ownership data, we found that 21 of the top shareholders collectively own less than 50% of the share register, implying that no single individual has a majority interest.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Ausgold

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

We can report that insiders do own shares in Ausgold Limited. It has a market capitalization of just AU$176m, and insiders have AU$9.6m worth of shares, in their own names. Some would say this shows alignment of interests between shareholders and the board, though we generally prefer to see bigger insider holdings. But it might be worth checking if those insiders have been selling.

General Public Ownership

The general public, who are usually individual investors, hold a substantial 57% stake in Ausgold, suggesting it is a fairly popular stock. This size of ownership gives investors from the general public some collective power. They can and probably do influence decisions on executive compensation, dividend policies and proposed business acquisitions.

Private Company Ownership

It seems that Private Companies own 3.2%, of the Ausgold stock. It might be worth looking deeper into this. If related parties, such as insiders, have an interest in one of these private companies, that should be disclosed in the annual report. Private companies may also have a strategic interest in the company.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Take risks for example - Ausgold has 3 warning signs we think you should be aware of.

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, backed by strong financial data.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:AUC

Excellent balance sheet low.

Market Insights

Community Narratives