- Australia

- /

- Personal Products

- /

- ASX:CCO

This Is Why The Calmer Co International Limited's (ASX:CCO) CEO Compensation Looks Appropriate

Key Insights

- Calmer Co International will host its Annual General Meeting on 20th of November

- Total pay for CEO Anthony Noble includes AU$217.5k salary

- Total compensation is 49% below industry average

- Calmer Co International's EPS grew by 17% over the past three years while total shareholder loss over the past three years was 98%

Performance at The Calmer Co International Limited (ASX:CCO) has been rather uninspiring recently and shareholders may be wondering how CEO Anthony Noble plans to fix this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 20th of November. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for Calmer Co International

Comparing The Calmer Co International Limited's CEO Compensation With The Industry

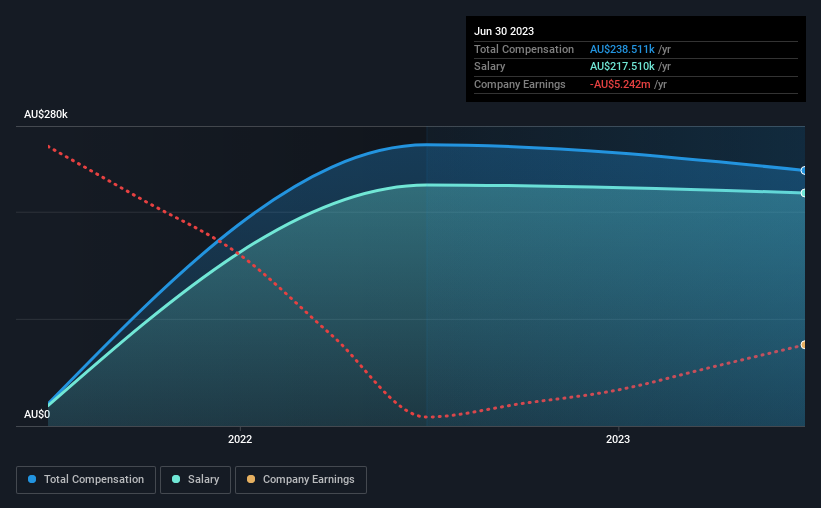

At the time of writing, our data shows that The Calmer Co International Limited has a market capitalization of AU$3.6m, and reported total annual CEO compensation of AU$239k for the year to June 2023. Notably, that's a decrease of 9.1% over the year before. Notably, the salary which is AU$217.5k, represents most of the total compensation being paid.

In comparison with other companies in the Australia Personal Products industry with market capitalizations under AU$314m, the reported median total CEO compensation was AU$464k. This suggests that Anthony Noble is paid below the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$218k | AU$225k | 91% |

| Other | AU$21k | AU$38k | 9% |

| Total Compensation | AU$239k | AU$263k | 100% |

Talking in terms of the industry, salary represented approximately 35% of total compensation out of all the companies we analyzed, while other remuneration made up 65% of the pie. Calmer Co International pays out 91% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

The Calmer Co International Limited's Growth

Over the past three years, The Calmer Co International Limited has seen its earnings per share (EPS) grow by 17% per year. It saw its revenue drop 13% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. While it would be good to see revenue growth, profits matter more in the end. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has The Calmer Co International Limited Been A Good Investment?

Few The Calmer Co International Limited shareholders would feel satisfied with the return of -98% over three years. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The fact that shareholders have earned a negative share price return is certainly disconcerting. This diverges with the robust growth in EPS, suggesting that there is a large discrepancy between share price and fundamentals. A key question may be why the fundamentals have not yet been reflected into the share price. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 7 warning signs for Calmer Co International (of which 6 are a bit concerning!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Calmer Co International, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CCO

Calmer Co International

Operates as a health and wellness company in Australia, Fiji, the United States, and internationally.

Excellent balance sheet moderate.

Market Insights

Community Narratives