Advertisement

- Australia

- /

- Healthcare Services

- /

- ASX:RHC

Ramsay Health Care (ASX:RHC) May Have Issues Allocating Its Capital

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at Ramsay Health Care (ASX:RHC), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Ramsay Health Care, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

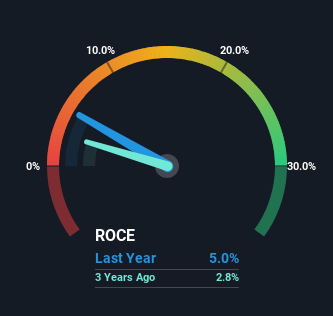

0.05 = AU$850m ÷ (AU$21b - AU$3.7b) (Based on the trailing twelve months to December 2023).

Thus, Ramsay Health Care has an ROCE of 5.0%. Ultimately, that's a low return and it under-performs the Healthcare industry average of 6.9%.

Check out our latest analysis for Ramsay Health Care

In the above chart we have measured Ramsay Health Care's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Ramsay Health Care .

How Are Returns Trending?

In terms of Ramsay Health Care's historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 10%, but since then they've fallen to 5.0%. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. If these investments prove successful, this can bode very well for long term stock performance.

On a related note, Ramsay Health Care has decreased its current liabilities to 18% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

What We Can Learn From Ramsay Health Care's ROCE

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for Ramsay Health Care. These growth trends haven't led to growth returns though, since the stock has fallen 30% over the last five years. As a result, we'd recommend researching this stock further to uncover what other fundamentals of the business can show us.

If you'd like to know more about Ramsay Health Care, we've spotted 2 warning signs, and 1 of them can't be ignored.

While Ramsay Health Care may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:RHC

Ramsay Health Care

Owns and operates hospitals in Australia, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor