Advertisement

- Australia

- /

- Medical Equipment

- /

- ASX:IMR

Does Imricor Medical Systems (ASX:IMR) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Imricor Medical Systems, Inc. (ASX:IMR) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Imricor Medical Systems

How Much Debt Does Imricor Medical Systems Carry?

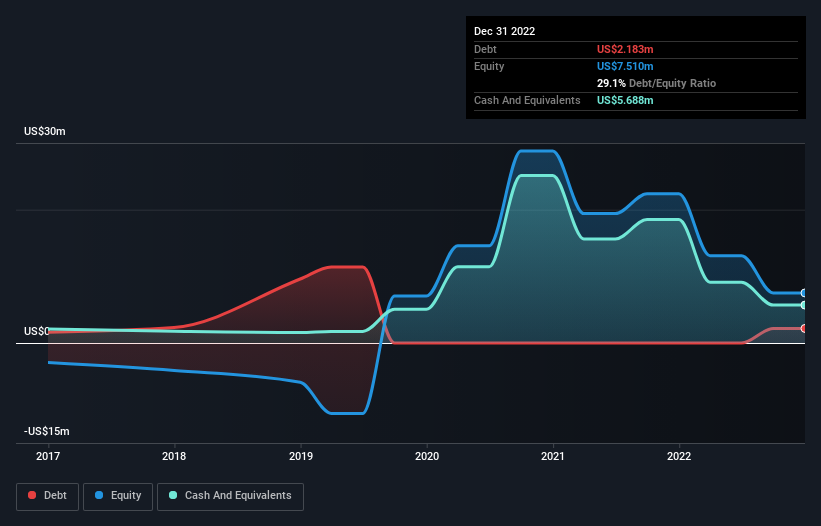

You can click the graphic below for the historical numbers, but it shows that as of December 2022 Imricor Medical Systems had US$2.18m of debt, an increase on none, over one year. But on the other hand it also has US$5.69m in cash, leading to a US$3.50m net cash position.

A Look At Imricor Medical Systems' Liabilities

We can see from the most recent balance sheet that Imricor Medical Systems had liabilities of US$2.07m falling due within a year, and liabilities of US$4.12m due beyond that. Offsetting this, it had US$5.69m in cash and US$125.5k in receivables that were due within 12 months. So its liabilities total US$377.1k more than the combination of its cash and short-term receivables.

This state of affairs indicates that Imricor Medical Systems' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$38.6m company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Imricor Medical Systems also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is Imricor Medical Systems's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Imricor Medical Systems wasn't profitable at an EBIT level, but managed to grow its revenue by 17%, to US$816k. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Imricor Medical Systems?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Imricor Medical Systems had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$17m and booked a US$17m accounting loss. With only US$3.50m on the balance sheet, it would appear that its going to need to raise capital again soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 6 warning signs for Imricor Medical Systems (3 are potentially serious!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:IMR

Imricor Medical Systems

A medical device company, designs, manufactures, sells, and distributes magnetic resonance imaging (MRI) compatible products for cardiac catheter ablation procedures in the United States, Europe, and the Middle East.

High growth potential low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor