- Australia

- /

- Healthtech

- /

- ASX:ALC

Alcidion Group Limited (ASX:ALC) Held Back By Insufficient Growth Even After Shares Climb 41%

Alcidion Group Limited (ASX:ALC) shareholders have had their patience rewarded with a 41% share price jump in the last month. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 28% over that time.

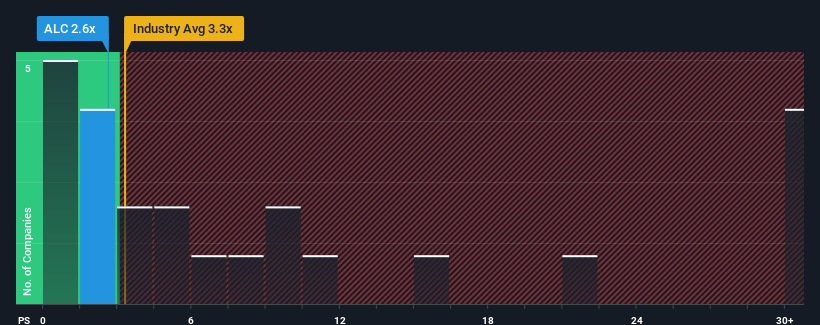

Even after such a large jump in price, Alcidion Group's price-to-sales (or "P/S") ratio of 2.6x might still make it look like a buy right now compared to the Healthcare Services industry in Australia, where around half of the companies have P/S ratios above 5.2x and even P/S above 15x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Alcidion Group

What Does Alcidion Group's P/S Mean For Shareholders?

Alcidion Group could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Alcidion Group will help you uncover what's on the horizon.How Is Alcidion Group's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Alcidion Group's to be considered reasonable.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period has seen an excellent 88% overall rise in revenue, in spite of its uninspiring short-term performance. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

Looking ahead now, revenue is anticipated to climb by 7.8% per year during the coming three years according to the three analysts following the company. That's shaping up to be materially lower than the 25% per year growth forecast for the broader industry.

In light of this, it's understandable that Alcidion Group's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Alcidion Group's P/S?

Despite Alcidion Group's share price climbing recently, its P/S still lags most other companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Alcidion Group's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Alcidion Group that you need to be mindful of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ALC

Alcidion Group

Engages in the development and licensing of healthcare software products in Australia, New Zealand, and the United Kingdom.

Reasonable growth potential with adequate balance sheet.

Market Insights

Community Narratives