Advertisement

Exploring Three ASX Stocks Estimated To Be Up To 41.4% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

The Australian stock market has seen a recent dip, dropping 2.0% over the last week, yet it maintains a positive trajectory with a 6.1% increase over the past year and earnings expected to grow by 14% annually. In such a fluctuating environment, identifying stocks that are trading below their intrinsic value could present opportunities for investors looking for potential growth at reduced prices.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| LaserBond (ASX:LBL) | A$0.70 | A$1.21 | 42.1% |

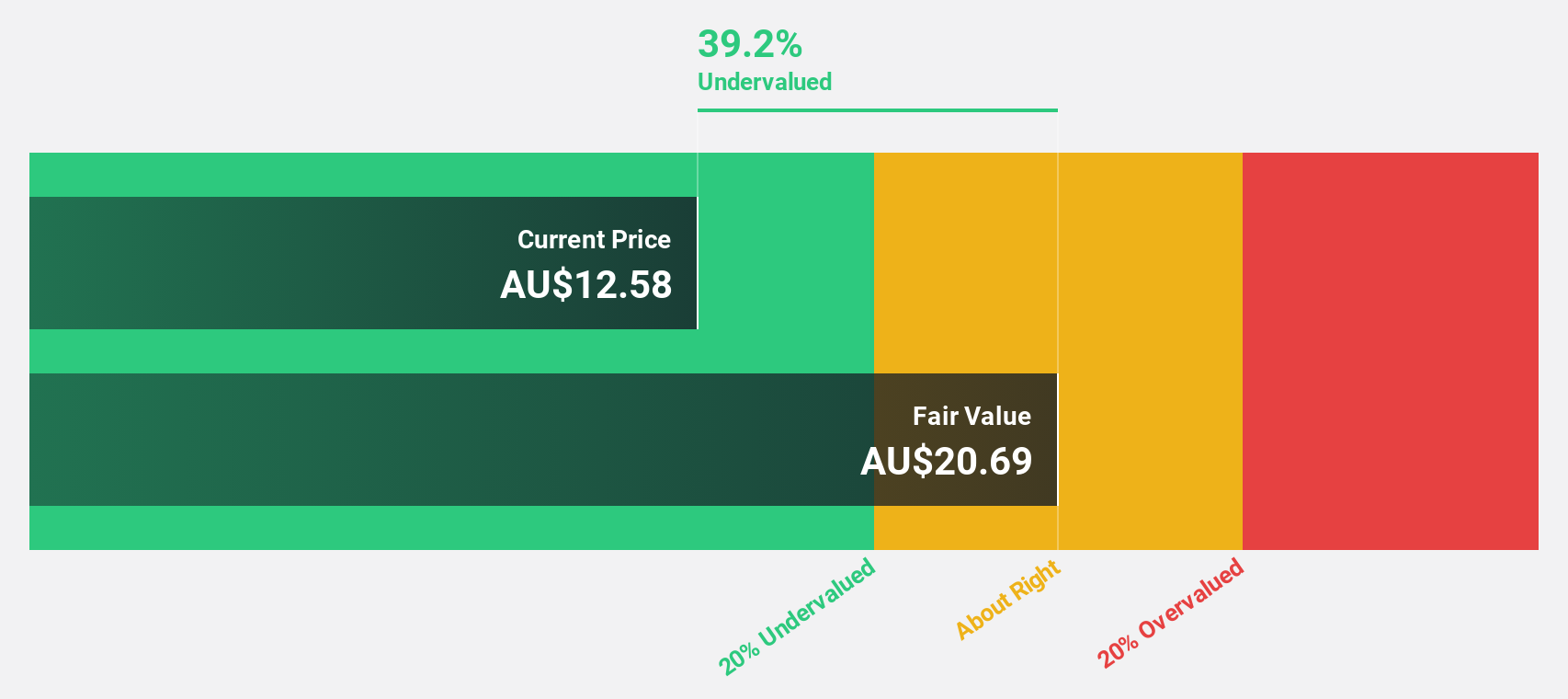

| Charter Hall Group (ASX:CHC) | A$12.50 | A$22.77 | 45.1% |

| HMC Capital (ASX:HMC) | A$7.42 | A$14.23 | 47.9% |

| ReadyTech Holdings (ASX:RDY) | A$3.22 | A$5.95 | 45.9% |

| Atturra (ASX:ATA) | A$0.74 | A$1.51 | 51% |

| hipages Group Holdings (ASX:HPG) | A$1.04 | A$1.94 | 46.4% |

| IPH (ASX:IPH) | A$6.20 | A$11.37 | 45.5% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| SiteMinder (ASX:SDR) | A$4.99 | A$8.34 | 40.2% |

| Treasury Wine Estates (ASX:TWE) | A$12.08 | A$20.61 | 41.4% |

We'll examine a selection from our screener results

Flight Centre Travel Group (ASX:FLT)

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally with a market capitalization of A$4.39 billion.

Operations: The company generates revenue primarily through its leisure and corporate travel services, amounting to A$1.28 billion and A$1.06 billion respectively.

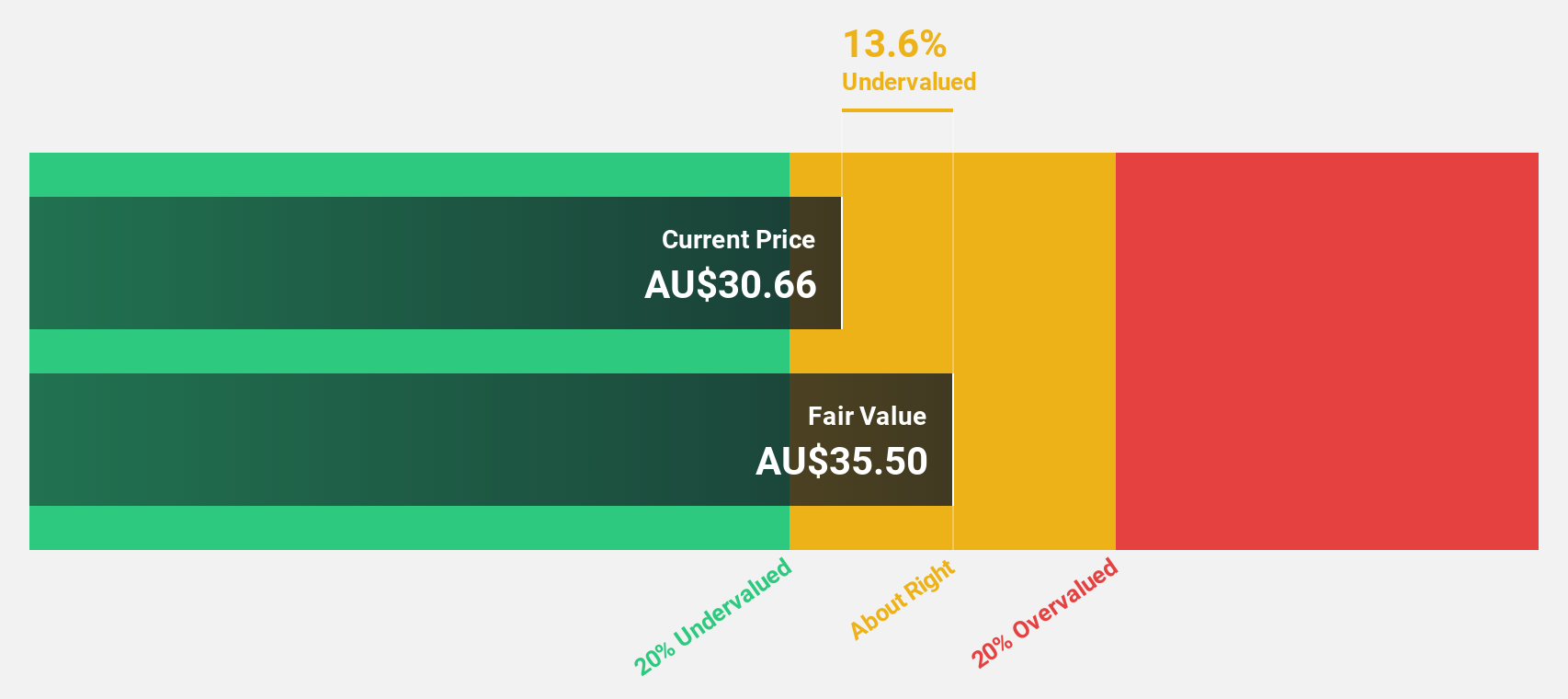

Estimated Discount To Fair Value: 19.7%

Flight Centre Travel Group is positioned intriguingly in the Australian market with its earnings expected to grow at 18.8% annually, outpacing the broader market's 13.7%. While its revenue growth forecast of 9.7% per year also exceeds the Australian market average of 5.4%, it doesn’t reach the high growth benchmark of over 20%. Additionally, a projected return on equity of 21.7% in three years suggests strong potential for efficient capital management.

- Our earnings growth report unveils the potential for significant increases in Flight Centre Travel Group's future results.

- Unlock comprehensive insights into our analysis of Flight Centre Travel Group stock in this financial health report.

Lovisa Holdings (ASX:LOV)

Overview: Lovisa Holdings Limited is a retailer specializing in fashion jewelry and accessories, with a market capitalization of approximately A$3.43 billion.

Operations: The company generates its revenue primarily from the retail sale of fashion jewelry and accessories, totaling approximately A$654 million.

Estimated Discount To Fair Value: 32.6%

Lovisa Holdings, trading at A$32.15, is valued below its estimated fair value of A$47.67, indicating a significant undervaluation based on cash flows. Forecasted to grow earnings by 19.23% annually, Lovisa's projected growth outstrips the Australian market's 13.7%. Additionally, its revenue growth rate of 14.3% annually surpasses the market average of 5.4%. Despite these positives, its earnings growth does not meet the high-growth threshold of over 20% per year.

- Our expertly prepared growth report on Lovisa Holdings implies its future financial outlook may be stronger than recent results.

- Take a closer look at Lovisa Holdings' balance sheet health here in our report.

Treasury Wine Estates (ASX:TWE)

Overview: Treasury Wine Estates Limited is a global wine company with operations across Australia, New Zealand, Asia, Europe, the UK, the Middle East, Africa, and the Americas, boasting a market capitalization of approximately A$9.73 billion.

Operations: The company's revenue is primarily generated through three segments: Penfolds at A$893.30 million, Treasury Americas at A$825.40 million, and Treasury Premium Brands at A$768.30 million.

Estimated Discount To Fair Value: 41.4%

Treasury Wine Estates (TWE) is projected to outpace the Australian market with its revenue expected to increase by 10.1% annually, compared to the market's 5.4%. Earnings are also set to rise significantly at a rate of 22.5% per year over the next three years. However, challenges include a dividend coverage issue, as current payouts are not well supported by earnings or cash flows. Additionally, TWE has experienced shareholder dilution and declining profit margins year-over-year, alongside significant one-off items affecting financial results. Recently, TWE expanded its distribution in China through an exclusive agreement with Season Global Trading for its Penfolds Champagne series, potentially boosting future revenues.

- The growth report we've compiled suggests that Treasury Wine Estates' future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Treasury Wine Estates.

Turning Ideas Into Actions

- Get an in-depth perspective on all 48 Undervalued ASX Stocks Based On Cash Flows by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Treasury Wine Estates might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TWE

Treasury Wine Estates

Operates as a wine company primarily in Australia, the United States, the United Kingdom, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor