The Australian stock market has shown robust performance recently, with a 1.1% increase over the last week and a notable 9.4% rise over the past year, alongside forecasts predicting annual earnings growth of 14%. In this context, high-yield dividend stocks can be particularly appealing for investors looking for both income and potential capital appreciation in a growing market.

Top 10 Dividend Stocks In Australia

| Name | Dividend Yield | Dividend Rating |

| Lindsay Australia (ASX:LAU) | 6.38% | ★★★★★☆ |

| Fiducian Group (ASX:FID) | 4.01% | ★★★★★☆ |

| Nick Scali (ASX:NCK) | 5.07% | ★★★★★☆ |

| Eagers Automotive (ASX:APE) | 7.09% | ★★★★★☆ |

| Centuria Capital Group (ASX:CNI) | 6.61% | ★★★★★☆ |

| Charter Hall Group (ASX:CHC) | 3.44% | ★★★★★☆ |

| Premier Investments (ASX:PMV) | 4.67% | ★★★★★☆ |

| Fortescue (ASX:FMG) | 7.44% | ★★★★★☆ |

| Diversified United Investment (ASX:DUI) | 3.17% | ★★★★★☆ |

| Australian United Investment (ASX:AUI) | 3.59% | ★★★★☆☆ |

Click here to see the full list of 30 stocks from our Top ASX Dividend Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

nib holdings (ASX:NHF)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: nib holdings limited operates as an underwriter and distributor of private health insurance for residents, international students, and visitors in Australia and New Zealand, with a market capitalization of approximately A$3.46 billion.

Operations: nib holdings limited generates revenue primarily through Australian Residents Health Insurance (A$2.55 billion), followed by New Zealand Insurance (A$351.90 million), NIB Travel (A$109.10 million), and International (Inbound) Health Insurance (A$173.20 million).

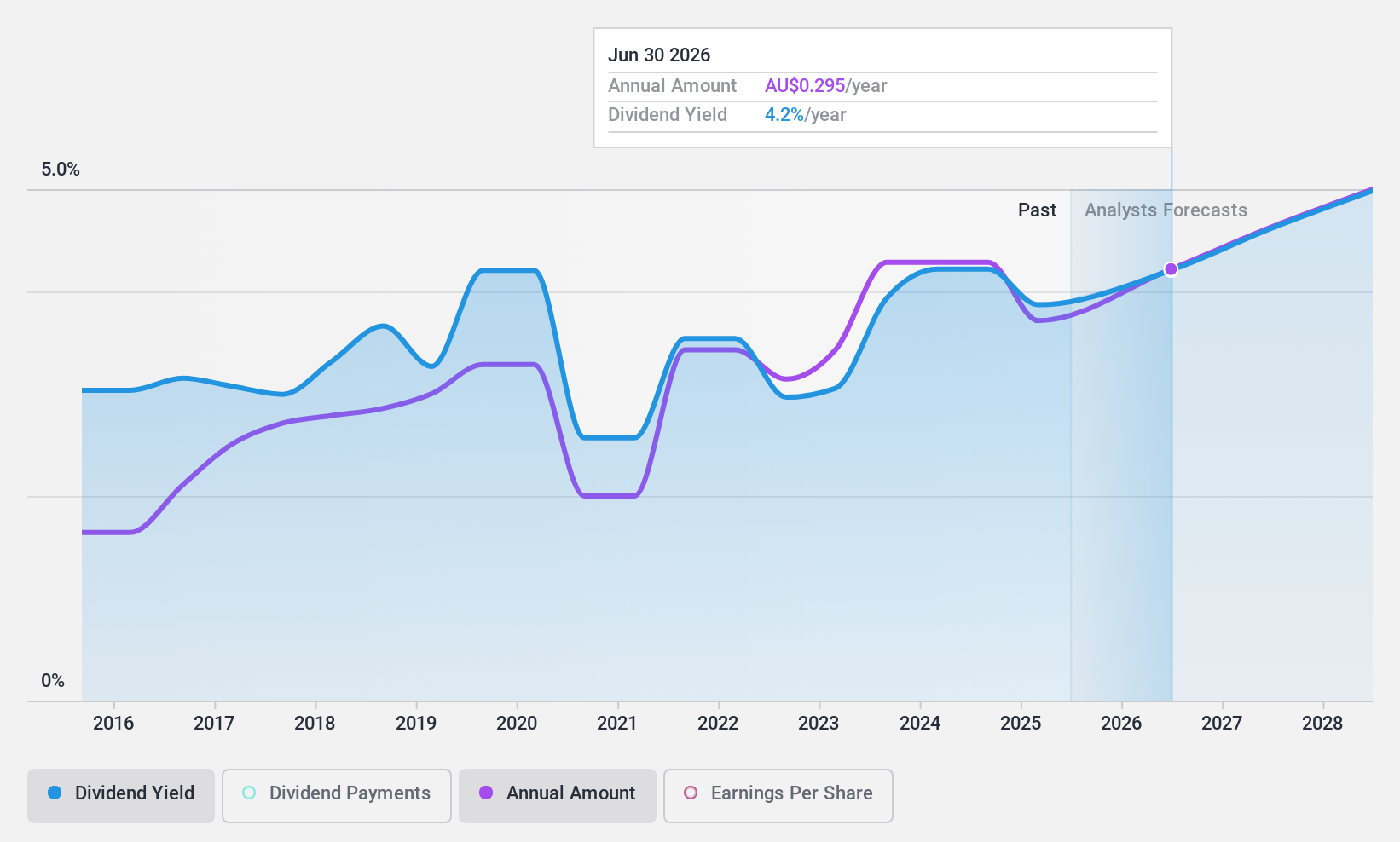

Dividend Yield: 4.2%

Nib Holdings' recent financial performance shows a net income increase to A$106.4 million, up from A$89.2 million year-over-year, with earnings per share rising to A$0.22 from A$0.19. Despite this growth, the company's dividend history is marked by volatility and a low yield of 4.2%, underperforming against Australia's top dividend payers at 6.33%. The dividends are well-covered by both earnings and cash flows, with payout ratios of 67.5% and 57.9%, respectively, suggesting sustainability despite past inconsistencies in payment growth and reliability.

- Navigate through the intricacies of nib holdings with our comprehensive dividend report here.

- The analysis detailed in our nib holdings valuation report hints at an deflated share price compared to its estimated value.

QBE Insurance Group (ASX:QBE)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: QBE Insurance Group Limited operates globally, underwriting general insurance and reinsurance risks across the Australia Pacific and North America, with a market capitalization of approximately A$27.12 billion.

Operations: QBE Insurance Group Limited generates revenue primarily through three geographic segments: North America (A$11.12 billion), International (A$9.56 billion), and Australia Pacific (A$5.97 billion).

Dividend Yield: 3.3%

QBE Insurance Group's dividend profile shows a history of fluctuations with an unstable track record, despite recent increases. Currently trading 59.5% below its estimated fair value, the company offers a dividend yield of 3.31%, which is lower than the top Australian payers. However, dividends are sustainably covered by both earnings and cash flows with payout ratios of 48.3% and 44.7%, respectively. Recent corporate guidance confirms expectations for moderate premium growth in FY24, supported by rate increases.

- Unlock comprehensive insights into our analysis of QBE Insurance Group stock in this dividend report.

- According our valuation report, there's an indication that QBE Insurance Group's share price might be on the cheaper side.

Ricegrowers (ASX:SGLLV)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Ricegrowers Limited, trading as SGLLV on the ASX, is a rice food company with operations in Australia and internationally, boasting a market capitalization of approximately A$460.29 million.

Operations: Ricegrowers Limited generates revenue through several key segments: Riviana at A$219.12 million, Cop Rice at A$253.52 million, Rice Food at A$115.93 million, Rice Pool at A$487 million, and International Rice at A$821.54 million.

Dividend Yield: 7.7%

Ricegrowers has experienced earnings growth of 16.2% annually over the past five years, yet its dividend history is marked by volatility and inconsistency, with payments not steadily increasing during its nine-year dividend history. Despite this, the dividend yield stands at a competitive 7.69%, well above the Australian market average of 6.33%. The dividends are financially sustainable, backed by a cash payout ratio of 43.1% and an earnings payout ratio of 53.9%, indicating good coverage from both profits and cash flows.

- Click here to discover the nuances of Ricegrowers with our detailed analytical dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Ricegrowers shares in the market.

Make It Happen

- Click here to access our complete index of 30 Top ASX Dividend Stocks.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if QBE Insurance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:QBE

QBE Insurance Group

Engages in underwriting general insurance and reinsurance risks in the Australia Pacific, North America, and internationally.

Undervalued with solid track record and pays a dividend.