- Australia

- /

- Hospitality

- /

- ASX:PBH

BNK Banking Leads 3 ASX Penny Stocks To Consider

Reviewed by Simply Wall St

The Australian market has seen a mix of ups and downs recently, with notable events such as Qantas paying its first dividend in years and Coles showing consistent growth, even as the XJO remains below its February highs. In this context, investors might consider penny stocks—traditionally smaller or newer companies—as potential opportunities for growth. Despite the term's outdated feel, these stocks can still offer value when backed by strong financials and sound business models.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Financial Health Rating |

| GTN (ASX:GTN) | A$0.54 | A$106.04M | ★★★★★★ |

| Bisalloy Steel Group (ASX:BIS) | A$3.20 | A$153.29M | ★★★★★★ |

| Helloworld Travel (ASX:HLO) | A$1.695 | A$275.98M | ★★★★★★ |

| Austin Engineering (ASX:ANG) | A$0.435 | A$269.76M | ★★★★★☆ |

| IVE Group (ASX:IGL) | A$2.34 | A$362.44M | ★★★★★☆ |

| Southern Cross Electrical Engineering (ASX:SXE) | A$1.77 | A$467.76M | ★★★★★★ |

| Perenti (ASX:PRN) | A$1.25 | A$1.17B | ★★★★★★ |

| Regal Partners (ASX:RPL) | A$3.80 | A$1.27B | ★★★★★★ |

| EZZ Life Science Holdings (ASX:EZZ) | A$2.17 | A$102.37M | ★★★★★★ |

| SHAPE Australia (ASX:SHA) | A$3.05 | A$252.35M | ★★★★★★ |

Click here to see the full list of 1,028 stocks from our ASX Penny Stocks screener.

Let's uncover some gems from our specialized screener.

BNK Banking (ASX:BBC)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: BNK Banking Corporation Limited offers a range of retail and commercial banking products and financial services in Australia, with a market cap of A$37.99 million.

Operations: BNK Banking Corporation Limited has not reported any specific revenue segments.

Market Cap: A$37.99M

BNK Banking Corporation Limited, with a market cap of A$37.99 million, has shown improvement in its financial performance despite being unprofitable over recent years. The company reported net interest income of A$11.05 million for the half year ending December 31, 2024, up from A$8.56 million the previous year, and achieved a net income of A$0.32 million compared to a loss previously. While BNK's Loans to Deposits ratio is high at 126%, it maintains an appropriate level of bad loans at 0% and has not significantly diluted shareholders recently. However, management experience remains limited with an average tenure of 1.3 years.

- Jump into the full analysis health report here for a deeper understanding of BNK Banking.

- Gain insights into BNK Banking's past trends and performance with our report on the company's historical track record.

PointsBet Holdings (ASX:PBH)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: PointsBet Holdings Limited operates a cloud-based technology platform offering sports, racing, and iGaming betting products and services in Australia with a market cap of A$368.22 million.

Operations: PointsBet Holdings Limited does not report distinct revenue segments.

Market Cap: A$368.22M

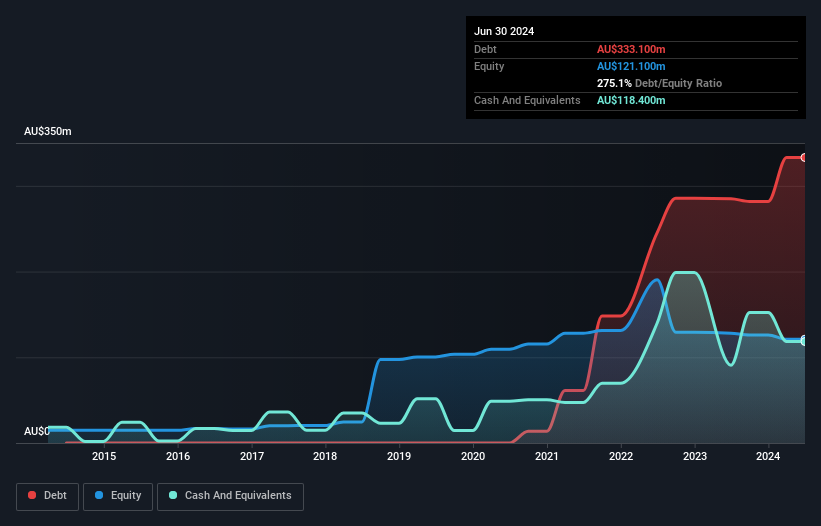

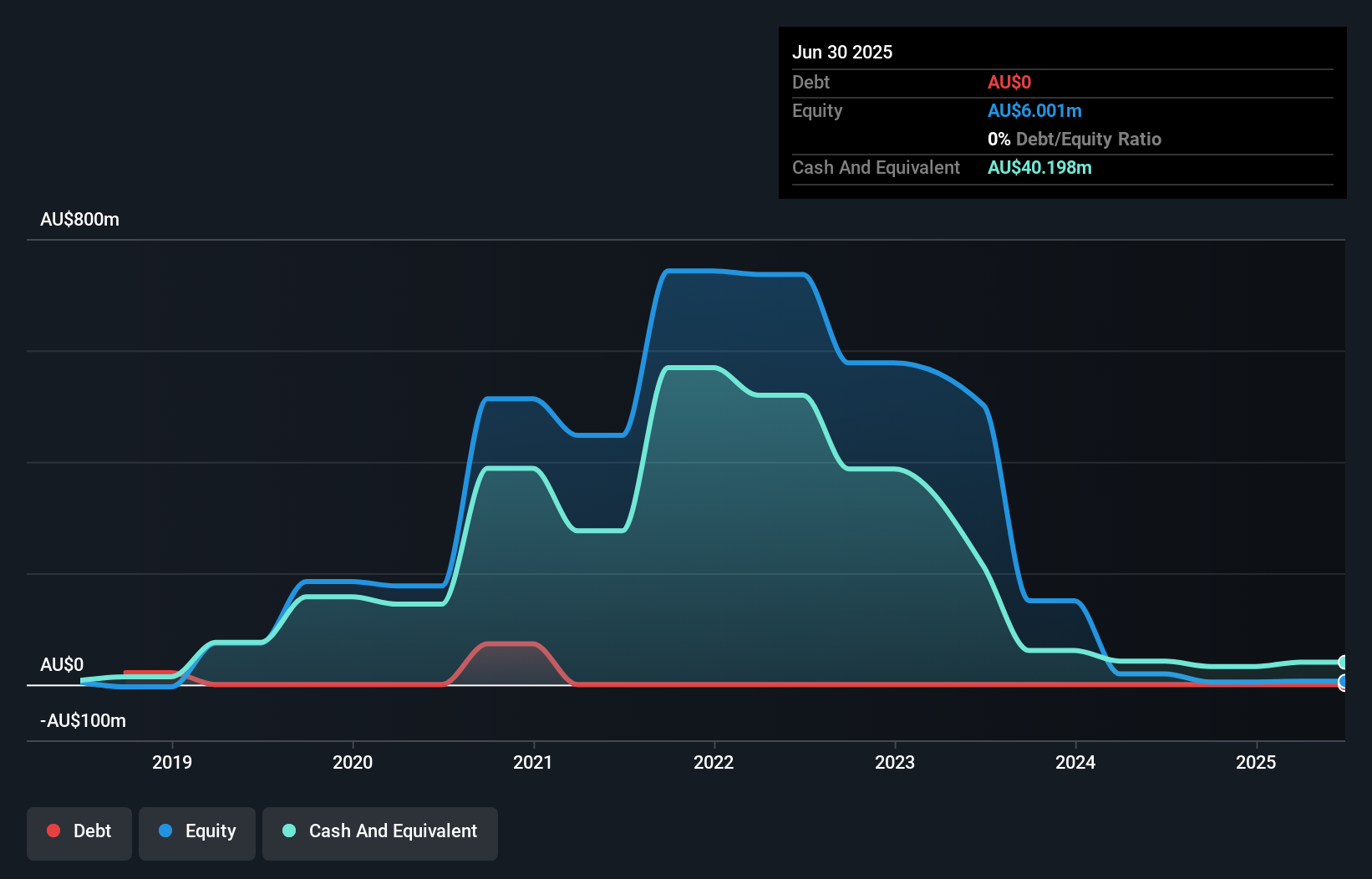

PointsBet Holdings Limited, with a market cap of A$368.22 million, is currently undergoing significant developments as MIXI Australia Pty Ltd has agreed to acquire it for approximately A$370 million. The deal values PointsBet at A$1.06 per share and awaits regulatory and shareholder approvals, with completion expected by mid-June 2025. Despite being unprofitable, the company reported improved earnings for the half year ending December 31, 2024, with sales increasing to A$124.36 million and net losses narrowing from the previous year. PointsBet remains debt-free but faces challenges covering short-term liabilities with its current assets.

- Get an in-depth perspective on PointsBet Holdings' performance by reading our balance sheet health report here.

- Gain insights into PointsBet Holdings' outlook and expected performance with our report on the company's earnings estimates.

Ridley (ASX:RIC)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Ridley Corporation Limited, with a market cap of A$856.20 million, provides animal nutrition solutions in Australia through its subsidiaries.

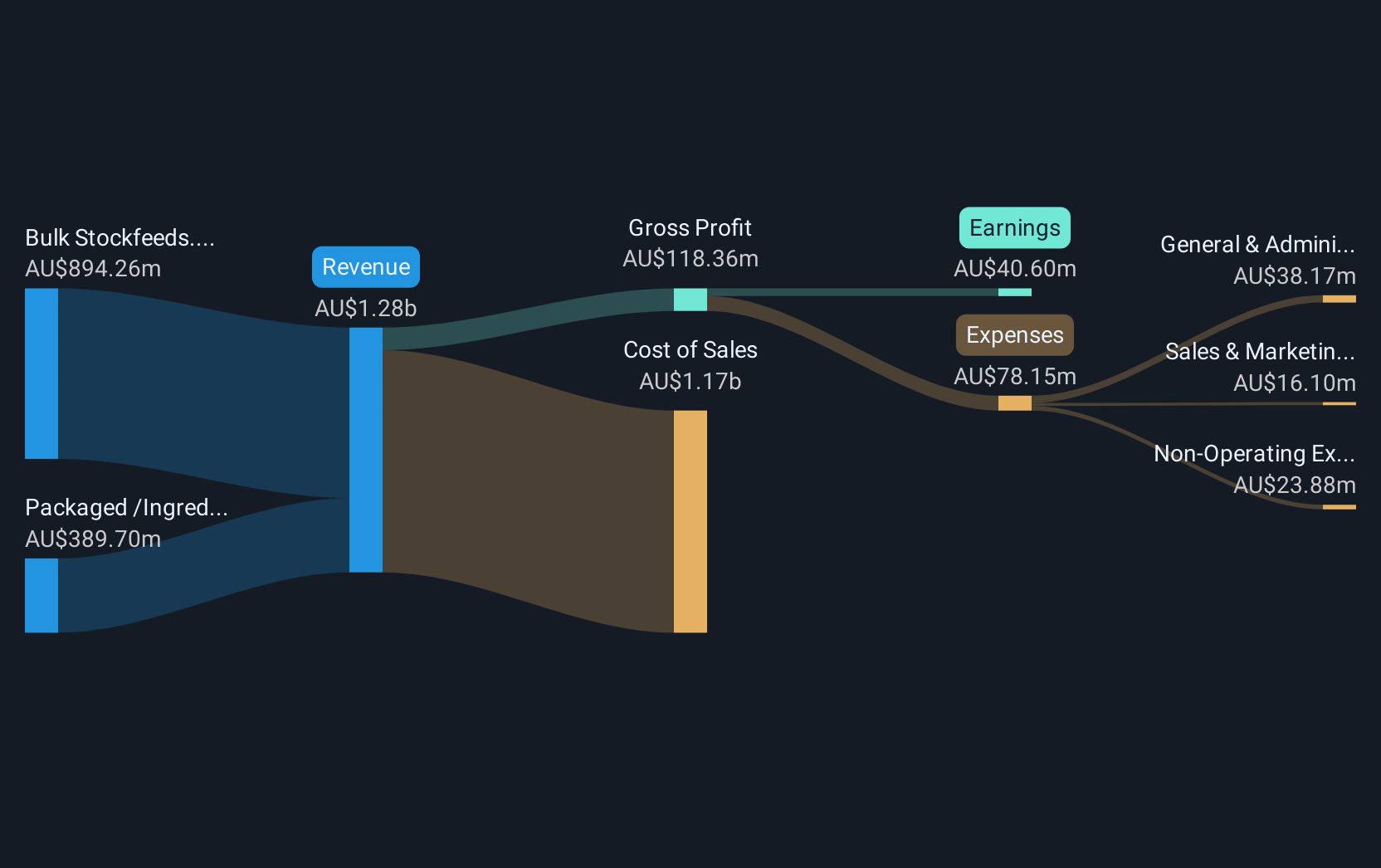

Operations: The company generates revenue from two main segments: Bulk Stockfeeds, contributing A$894.26 million, and Packaged/Ingredients, accounting for A$389.70 million.

Market Cap: A$856.2M

Ridley Corporation Limited, with a market cap of A$856.20 million, has shown consistent revenue generation from its Bulk Stockfeeds and Packaged/Ingredients segments. Recent earnings for the half year ended December 31, 2024, reported sales of A$658.85 million and net income of A$22.19 million. Despite a slight dip in profit margins to 3.2%, Ridley's financial health appears robust with short-term assets exceeding liabilities and debt well-covered by operating cash flow (107.1%). The company increased its dividend to A$0.0475 per share, reflecting stable cash flow management amidst industry challenges and modest earnings growth forecasts at 12.22% annually.

- Click to explore a detailed breakdown of our findings in Ridley's financial health report.

- Explore Ridley's analyst forecasts in our growth report.

Summing It All Up

- Click through to start exploring the rest of the 1,025 ASX Penny Stocks now.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:PBH

PointsBet Holdings

Provides sports, racing, and iGaming betting products and services through its cloud-based technology platform in Australia.

High growth potential and good value.

Similar Companies

Market Insights

Community Narratives