- Australia

- /

- Oil and Gas

- /

- ASX:WDS

Revenues Working Against Woodside Energy Group Ltd's (ASX:WDS) Share Price

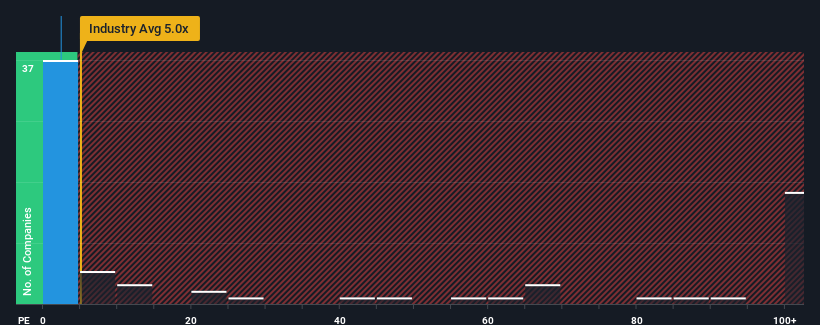

You may think that with a price-to-sales (or "P/S") ratio of 2.4x Woodside Energy Group Ltd (ASX:WDS) is definitely a stock worth checking out, seeing as almost half of all the Oil and Gas companies in Australia have P/S ratios greater than 5x and even P/S above 85x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Woodside Energy Group

What Does Woodside Energy Group's Recent Performance Look Like?

With revenue that's retreating more than the industry's average of late, Woodside Energy Group has been very sluggish. It seems that many are expecting the dismal revenue performance to persist, which has repressed the P/S. You'd much rather the company improve its revenue performance if you still believe in the business. Or at the very least, you'd be hoping the revenue slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Woodside Energy Group will help you uncover what's on the horizon.Is There Any Revenue Growth Forecasted For Woodside Energy Group?

In order to justify its P/S ratio, Woodside Energy Group would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered a frustrating 17% decrease to the company's top line. Even so, admirably revenue has lifted 289% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should bring diminished returns, with revenue decreasing 2.1% per annum as estimated by the analysts watching the company. That's not great when the rest of the industry is expected to grow by 155% per year.

With this in consideration, we find it intriguing that Woodside Energy Group's P/S is closely matching its industry peers. However, shrinking revenues are unlikely to lead to a stable P/S over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It's clear to see that Woodside Energy Group maintains its low P/S on the weakness of its forecast for sliding revenue, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about these 2 warning signs we've spotted with Woodside Energy Group (including 1 which makes us a bit uncomfortable).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Woodside Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:WDS

Woodside Energy Group

Engages in the exploration, evaluation, development, production, and marketing of hydrocarbons in the Asia Pacific, Africa, the Americas, and the Europe.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives