Advertisement

Here's Why Shareholders May Want To Be Cautious With Increasing ClearView Wealth Limited's (ASX:CVW) CEO Pay Packet

Shareholders of ClearView Wealth Limited (ASX:CVW) will have been dismayed by the negative share price return over the last three years. Per share earnings growth is also poor, despite revenues growing. Shareholders will have a chance to take their concerns to the board at the next AGM on 10 November 2021 and vote on resolutions including executive compensation, which studies show may have an impact on company performance. Here's our take on why we think shareholders might be hesitant about approving a raise at the moment.

View our latest analysis for ClearView Wealth

How Does Total Compensation For Simon Swanson Compare With Other Companies In The Industry?

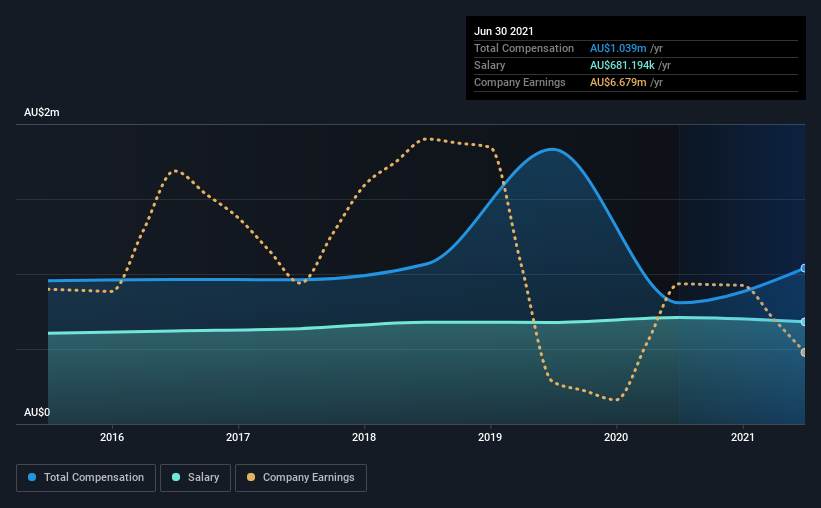

According to our data, ClearView Wealth Limited has a market capitalization of AU$495m, and paid its CEO total annual compensation worth AU$1.0m over the year to June 2021. Notably, that's an increase of 29% over the year before. In particular, the salary of AU$681.2k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between AU$269m and AU$1.1b had a median total CEO compensation of AU$1.1m. So it looks like ClearView Wealth compensates Simon Swanson in line with the median for the industry. What's more, Simon Swanson holds AU$12m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | AU$681k | AU$710k | 66% |

| Other | AU$358k | AU$98k | 34% |

| Total Compensation | AU$1.0m | AU$808k | 100% |

On an industry level, around 59% of total compensation represents salary and 41% is other remuneration. According to our research, ClearView Wealth has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at ClearView Wealth Limited's Growth Numbers

Over the last three years, ClearView Wealth Limited has shrunk its earnings per share by 39% per year. It achieved revenue growth of 103% over the last year.

Investors would be a bit wary of companies that have lower EPS But in contrast the revenue growth is strong, suggesting future potential for EPS growth. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has ClearView Wealth Limited Been A Good Investment?

Given the total shareholder loss of 16% over three years, many shareholders in ClearView Wealth Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The company's earnings haven't grown and possibly because of that, the stock has performed poorly, resulting in a loss for the company's shareholders. In the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan is in line with their expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 4 warning signs for ClearView Wealth (of which 1 is significant!) that you should know about in order to have a holistic understanding of the stock.

Important note: ClearView Wealth is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:CVW

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor