Advertisement

Even though Experience Co Limited (ASX:EXP) has fallen by 13% over the past week , insiders who sold AU$327k worth of stock over the past year have had less luck. Insiders would probably have been better off holding on to their shares given that the average selling price of AU$0.19 is still lower than the current share price.

Although we don't think shareholders should simply follow insider transactions, logic dictates you should pay some attention to whether insiders are buying or selling shares.

View our latest analysis for Experience Co

The Last 12 Months Of Insider Transactions At Experience Co

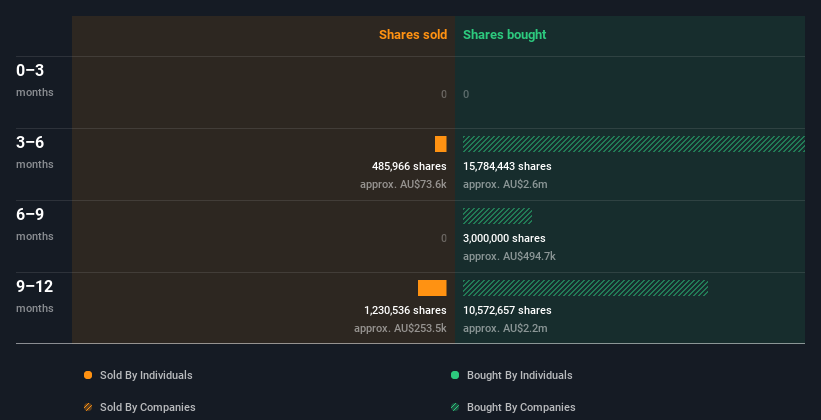

Over the last year, we can see that the biggest insider sale was by the Founder & Non-Executive Director, Anthony Boucaut, for AU$191k worth of shares, at about AU$0.21 per share. We generally don't like to see insider selling, but the lower the sale price, the more it concerns us. The silver lining is that this sell-down took place above the latest price (AU$0.14). So it may not shed much light on insider confidence at current levels. Anthony Boucaut was the only individual insider to sell shares in the last twelve months. Notably Anthony Boucaut was also the biggest buyer, having purchased AU$4.1k worth of shares.

Anthony Boucaut divested 1.72m shares over the last 12 months at an average price of AU$0.19. You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. By clicking on the graph below, you can see the precise details of each insider transaction!

I will like Experience Co better if I see some big insider buys. While we wait, check out this free list of undervalued and small cap stocks with considerable, recent, insider buying.

Does Experience Co Boast High Insider Ownership?

Another way to test the alignment between the leaders of a company and other shareholders is to look at how many shares they own. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Experience Co insiders own about AU$42m worth of shares. That equates to 40% of the company. This level of insider ownership is good but just short of being particularly stand-out. It certainly does suggest a reasonable degree of alignment.

What Might The Insider Transactions At Experience Co Tell Us?

It doesn't really mean much that no insider has traded Experience Co shares in the last quarter. Still, the insider transactions at Experience Co in the last 12 months are not very heartening. The modest level of insider ownership is, at least, some comfort. So while it's helpful to know what insiders are doing in terms of buying or selling, it's also helpful to know the risks that a particular company is facing. Every company has risks, and we've spotted 1 warning sign for Experience Co you should know about.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Valuation is complex, but we're here to simplify it.

Discover if Experience Co might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:EXP

Experience Co

Engages in adventure tourism and leisure business in Australia and New Zealand.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor