Advertisement

- Australia

- /

- Food and Staples Retail

- /

- ASX:CLB

Is Candy Club Holdings (ASX:CLB) Using Debt In A Risky Way?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Candy Club Holdings Limited (ASX:CLB) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Candy Club Holdings

How Much Debt Does Candy Club Holdings Carry?

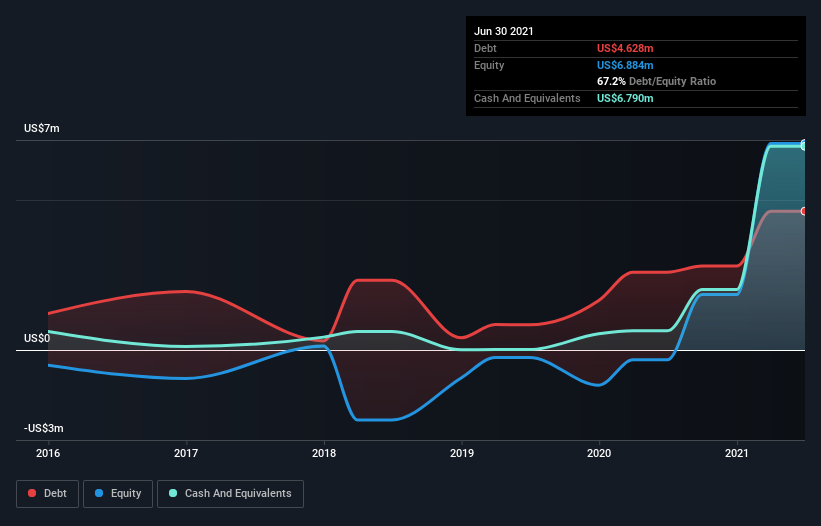

As you can see below, at the end of June 2021, Candy Club Holdings had US$4.63m of debt, up from US$2.60m a year ago. Click the image for more detail. However, it does have US$6.79m in cash offsetting this, leading to net cash of US$2.16m.

A Look At Candy Club Holdings' Liabilities

According to the last reported balance sheet, Candy Club Holdings had liabilities of US$3.49m due within 12 months, and liabilities of US$3.46m due beyond 12 months. Offsetting this, it had US$6.79m in cash and US$668.5k in receivables that were due within 12 months. So it actually has US$508.2k more liquid assets than total liabilities.

Having regard to Candy Club Holdings' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$40.4m company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that Candy Club Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Candy Club Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Candy Club Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 124%, to US$12m. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Candy Club Holdings?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Candy Club Holdings lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$8.4m and booked a US$6.1m accounting loss. Given it only has net cash of US$2.16m, the company may need to raise more capital if it doesn't reach break-even soon. The good news for shareholders is that Candy Club Holdings has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Candy Club Holdings (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:CLB

Candy Club Holdings

Candy Club Holdings Limited, a specialty market confectionery company, engages in the business-to-business, online, and business-to-customer candy wholesale business in the United States.

Low with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor