Advertisement

- Australia

- /

- Professional Services

- /

- ASX:QIP

QANTM Intellectual Property Limited (ASX:QIP) Investors Should Think About This Before Buying It For Its Dividend

Could QANTM Intellectual Property Limited (ASX:QIP) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

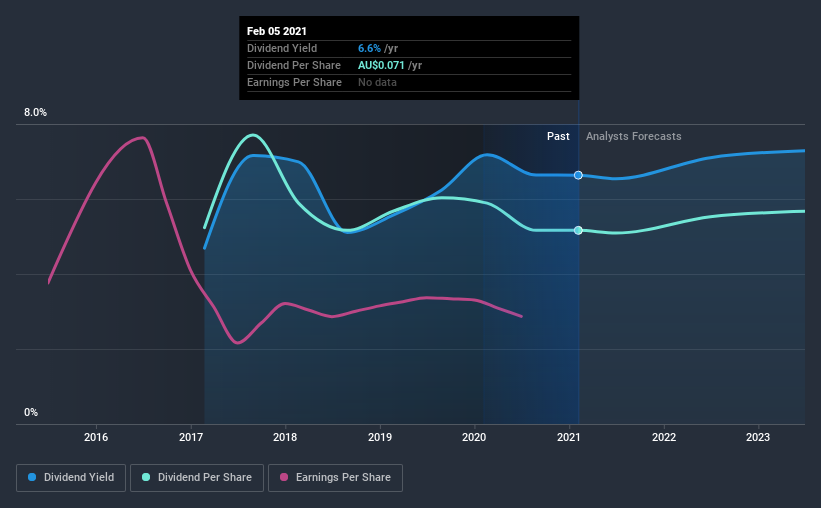

In this case, QANTM Intellectual Property likely looks attractive to dividend investors, given its 6.6% dividend yield and four-year payment history. We'd agree the yield does look enticing. Some simple analysis can reduce the risk of holding QANTM Intellectual Property for its dividend, and we'll focus on the most important aspects below.

Explore this interactive chart for our latest analysis on QANTM Intellectual Property!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Looking at the data, we can see that 99% of QANTM Intellectual Property's profits were paid out as dividends in the last 12 months. This is quite a high payout ratio that suggests the dividend is not well covered by earnings.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. QANTM Intellectual Property paid out 78% of its cash flow last year. This may be sustainable but it does not leave much of a buffer for unexpected circumstances. While the dividend was not well covered by profits, at least they were covered by free cash flow. Even so, if the company were to continue paying out almost all of its profits, we'd be concerned about whether the dividend is sustainable in a downturn.

We update our data on QANTM Intellectual Property every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. QANTM Intellectual Property has been paying a dividend for the past four years. This company's dividend has been unstable, and with a relatively short history, we think it's a little soon to draw strong conclusions about its long term dividend potential. During the past four-year period, the first annual payment was AU$0.07 in 2017, compared to AU$0.07 last year. Dividend payments have shrunk at a rate of less than 1% per annum over this time frame.

We struggle to make a case for buying QANTM Intellectual Property for its dividend, given that payments have shrunk over the past four years.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share (EPS) are growing - it's not worth taking the risk on a dividend getting cut, unless you might be rewarded with larger dividends in future. It's not great to see that QANTM Intellectual Property's have fallen at approximately 5.3% over the past five years. Declining earnings per share over a number of years is not a great sign for the dividend investor. Without some improvement, this does not bode well for the long term value of a company's dividend.

Conclusion

To summarise, shareholders should always check that QANTM Intellectual Property's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. We're a bit uncomfortable with its high payout ratio, although at least the dividend was covered by free cash flow. Second, earnings per share have been in decline, and its dividend has been cut at least once in the past. There are a few too many issues for us to get comfortable with QANTM Intellectual Property from a dividend perspective. Businesses can change, but we would struggle to identify why an investor should rely on this stock for their income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for QANTM Intellectual Property that investors should take into consideration.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you’re looking to trade QANTM Intellectual Property, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if QANTM Intellectual Property might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:QIP

QANTM Intellectual Property

Provides intellectual property services for start-up technology businesses, SMEs, multinationals, public sector research institutions, and universities in Australia, New Zealand, the United Kingdom, Singapore, Malaysia, and Hongkong.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor