- Australia

- /

- Professional Services

- /

- ASX:MMS

McMillan Shakespeare Limited's (ASX:MMS) 26% Price Boost Is Out Of Tune With Earnings

McMillan Shakespeare Limited (ASX:MMS) shareholders have had their patience rewarded with a 26% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 55% in the last year.

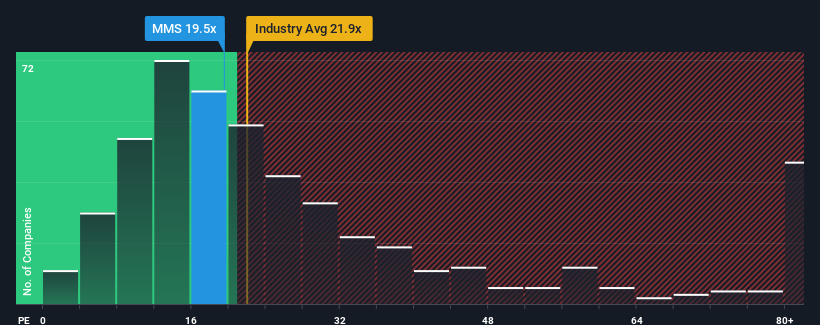

Even after such a large jump in price, there still wouldn't be many who think McMillan Shakespeare's price-to-earnings (or "P/E") ratio of 19.5x is worth a mention when the median P/E in Australia is similar at about 19x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

With earnings growth that's superior to most other companies of late, McMillan Shakespeare has been doing relatively well. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for McMillan Shakespeare

Is There Some Growth For McMillan Shakespeare?

In order to justify its P/E ratio, McMillan Shakespeare would need to produce growth that's similar to the market.

If we review the last year of earnings growth, the company posted a terrific increase of 22%. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 14% per year during the coming three years according to the six analysts following the company. That's shaping up to be materially lower than the 16% per annum growth forecast for the broader market.

With this information, we find it interesting that McMillan Shakespeare is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Key Takeaway

Its shares have lifted substantially and now McMillan Shakespeare's P/E is also back up to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that McMillan Shakespeare currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with McMillan Shakespeare, and understanding these should be part of your investment process.

Of course, you might also be able to find a better stock than McMillan Shakespeare. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:MMS

McMillan Shakespeare

Provides salary packaging, novated leasing, disability plan management, support co-ordination, asset management, and related financial products and services in Australia and New Zealand.

Very undervalued with proven track record.

Similar Companies

Market Insights

Community Narratives