Advertisement

IPH (ASX:IPH) First Half 2025 Results

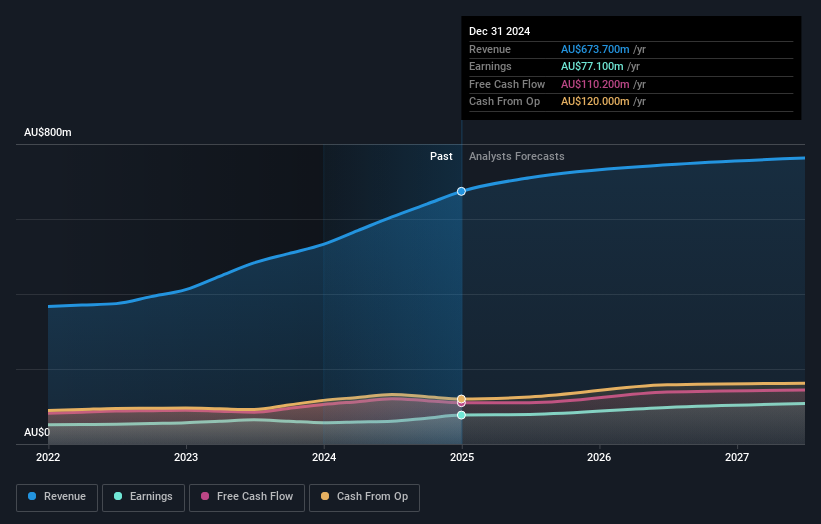

Key Financial Results

- Revenue: AU$341.6m (up 25% from 1H 2024).

- Net income: AU$37.3m (up 78% from 1H 2024).

- Profit margin: 11% (up from 7.7% in 1H 2024). The increase in margin was driven by higher revenue.

- EPS: AU$0.14 (up from AU$0.088 in 1H 2024).

All figures shown in the chart above are for the trailing 12 month (TTM) period

IPH Revenues and Earnings Beat Expectations

Revenue exceeded analyst estimates by 2.9%. Earnings per share (EPS) also surpassed analyst estimates by 6.0%.

Looking ahead, revenue is forecast to grow 4.0% p.a. on average during the next 3 years, compared to a 3.4% growth forecast for the Professional Services industry in Australia.

Performance of the Australian Professional Services industry.

The company's shares are up 1.9% from a week ago.

Risk Analysis

You should always think about risks. Case in point, we've spotted 1 warning sign for IPH you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:IPH

Very undervalued with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor