Advertisement

- Australia

- /

- Construction

- /

- ASX:NWH

Asian Undervalued Small Caps With Recent Insider Activity

Simply Wall St

Reviewed by Simply Wall St

Amidst global market fluctuations driven by trade policy uncertainties and shifting economic indicators, Asian small-cap stocks have captured investor attention due to their potential for growth in a volatile environment. In this context, identifying companies with strong fundamentals and recent insider activity can offer valuable insights into promising opportunities in the region's dynamic markets.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Infomedia | 30.5x | 3.4x | 37.21% | ★★★★★★ |

| Security Bank | 4.8x | 1.1x | 39.83% | ★★★★★☆ |

| Puregold Price Club | 9.0x | 0.4x | 26.55% | ★★★★★☆ |

| Hansen Technologies | 281.8x | 2.7x | 29.48% | ★★★★★☆ |

| Hong Leong Asia | 8.9x | 0.2x | 46.31% | ★★★★☆☆ |

| Dicker Data | 19.8x | 0.7x | -23.71% | ★★★★☆☆ |

| Sing Investments & Finance | 7.2x | 3.7x | 36.69% | ★★★★☆☆ |

| Viva Energy Group | NA | 0.1x | 14.77% | ★★★★☆☆ |

| Collins Foods | 20.1x | 0.7x | -1.68% | ★★★☆☆☆ |

| Integral Diagnostics | 147.7x | 1.7x | 43.36% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

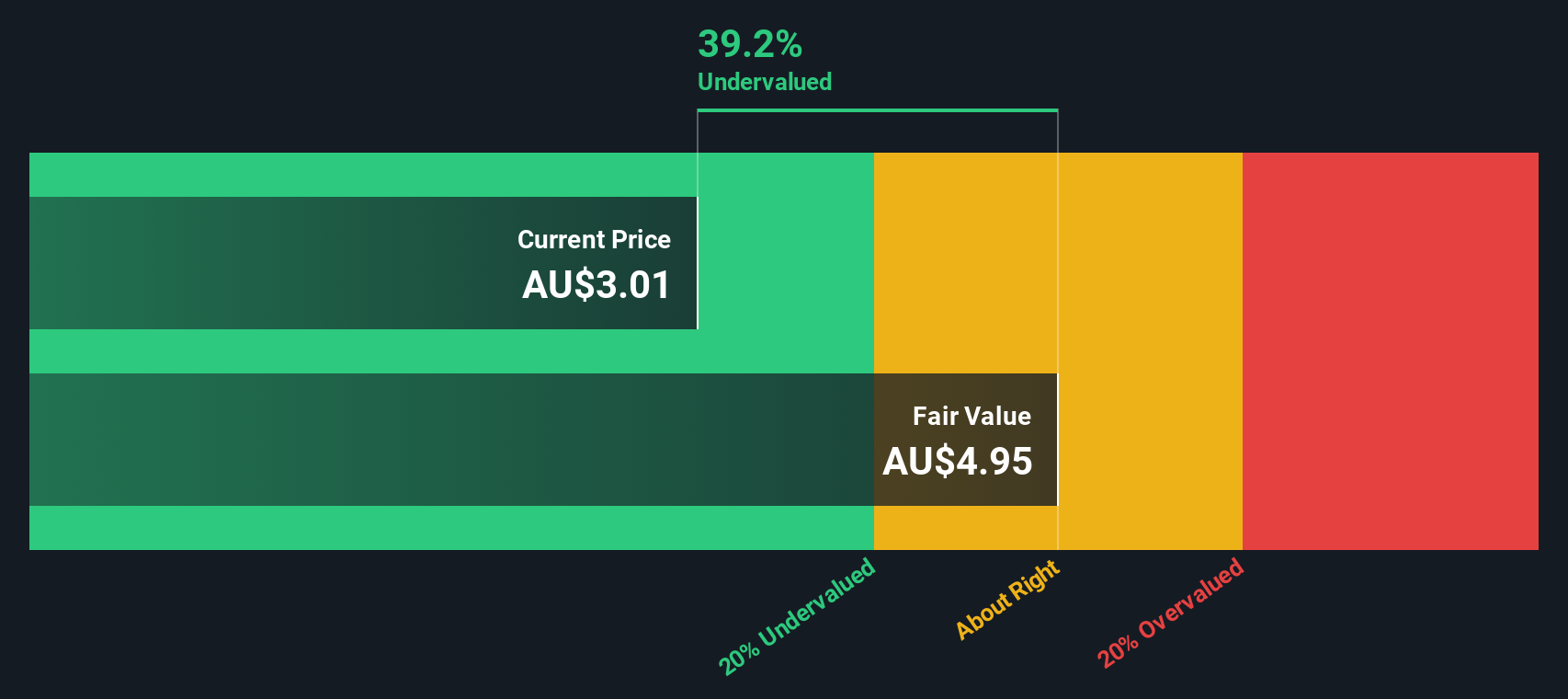

National Storage REIT (ASX:NSR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: National Storage REIT operates and manages storage centers, with a market capitalization of A$4.08 billion.

Operations: The primary revenue stream comes from the operation and management of storage centers, generating A$369.99 million. The gross profit margin has shown a gradual decrease to 87.25% by the end of 2024. Operating expenses, including general and administrative costs, have increased over time, impacting net income margins which stood at 5.87% as of December 2024.

PE: 133.5x

National Storage REIT, a smaller player in Asia's storage sector, recently reported half-year earnings with sales of A$173.9 million, up from A$161.6 million the previous year. Despite this growth in sales and revenue reaching A$190.5 million, net income fell to A$9.5 million from A$16.7 million due to large one-off items affecting results and lower profit margins at 5.9%. Insider confidence is evident through recent share purchases between December 2024 and February 2025, signaling potential value recognition by those closely involved with the company’s operations amidst its reliance on higher-risk external borrowing for funding needs. With earnings forecasted to grow by over 21% annually, NSR presents an intriguing opportunity for investors seeking undervalued stocks in Asia's dynamic market landscape.

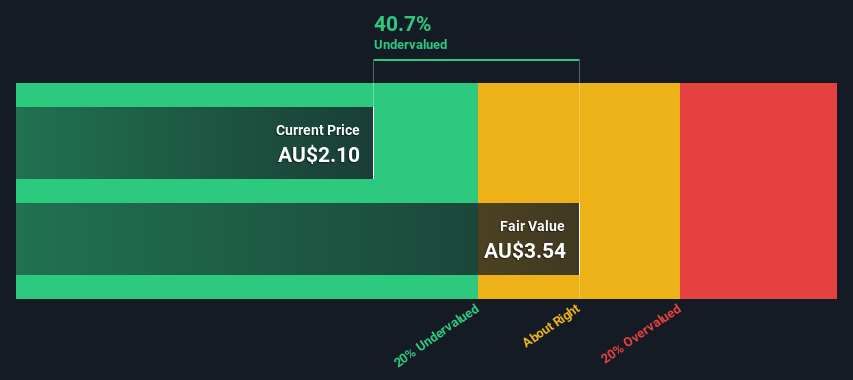

NRW Holdings (ASX:NWH)

Simply Wall St Value Rating: ★★★★★★

Overview: NRW Holdings is an Australian company specializing in mining, civil construction, and urban infrastructure services with a market capitalization of approximately A$1.49 billion.

Operations: NRW Holdings generates revenue primarily from its Mining, MET, and Civil segments, with the Mining segment being the largest contributor at A$1.56 billion. The company's gross profit margin has shown a gradual increase over recent periods, reaching 48.10% as of December 2024. Operating expenses are significant and include general and administrative costs which have been rising alongside revenue growth.

PE: 10.9x

NRW Holdings, a smaller player in the Asian market, showcases potential value with its recent earnings growth; sales for H1 2025 rose to A$1.65 billion from A$1.43 billion year-on-year, while net income increased to A$51.69 million from A$41.64 million. The company declared a dividend of A$0.07 per share payable in April 2025, signaling confidence despite CFO changes and reliance on external borrowing for funding. Earnings are projected to grow annually by 7.9%.

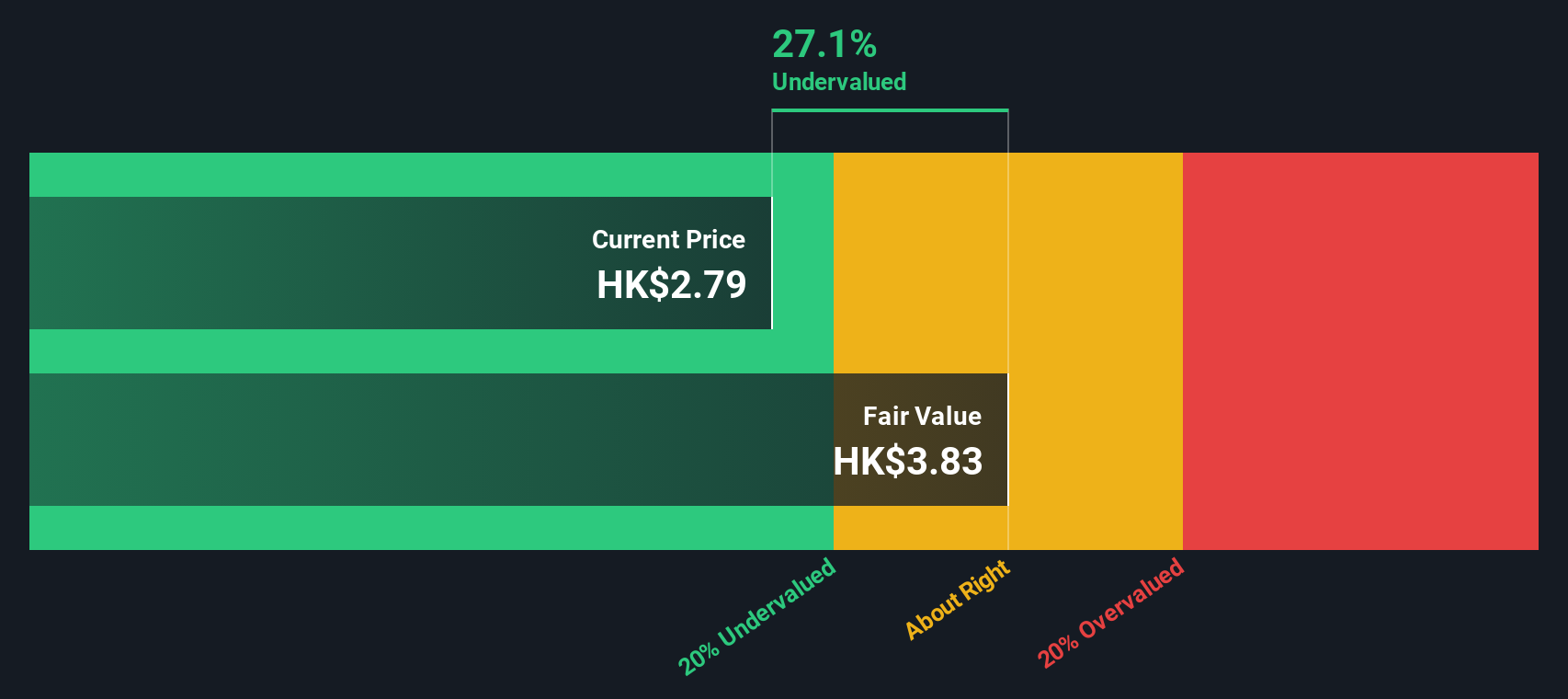

Ming Yuan Cloud Group Holdings (SEHK:909)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ming Yuan Cloud Group Holdings specializes in providing cloud services and on-premise software solutions, with a market cap of CN¥7.34 billion.

Operations: The company generates revenue primarily from Cloud Services and On-premise Software and Services, with Cloud Services contributing the majority. Over recent periods, the gross profit margin has shown a range of fluctuations, with a notable peak at 81.44% in December 2022 before declining to 79.48% by December 2023. Operating expenses are significant, driven largely by Sales & Marketing and R&D expenditures.

PE: -17.3x

Ming Yuan Cloud Group Holdings, a small company in Asia, recently saw insider confidence with Xiaohui Chen purchasing 2 million shares for approximately US$4.9 million. This activity suggests potential optimism about future prospects despite the company's current challenges. Ming Yuan faces profitability issues and relies solely on higher-risk external borrowing for funding, adding financial strain. Recent volatility in share prices further complicates its outlook. The appointment of Ernst & Young as auditors may enhance governance stability moving forward.

- Delve into the full analysis valuation report here for a deeper understanding of Ming Yuan Cloud Group Holdings.

Gain insights into Ming Yuan Cloud Group Holdings' past trends and performance with our Past report.

Summing It All Up

- Reveal the 56 hidden gems among our Undervalued Asian Small Caps With Insider Buying screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NRW Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:NWH

NRW Holdings

Through its subsidiaries, provides diversified contract services to the resources and infrastructure sectors in Australia.

Very undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor