Advertisement

Ian Testrow became the CEO of Emeco Holdings Limited (ASX:EHL) in 2015, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Emeco Holdings pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

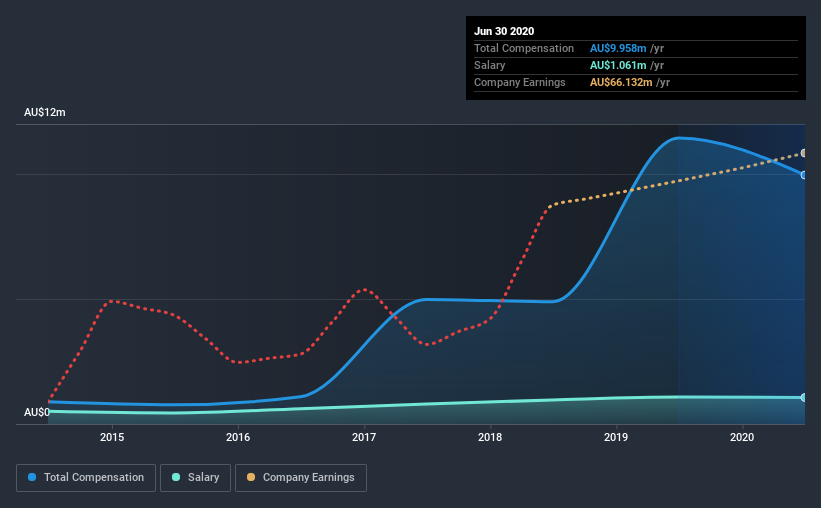

View our latest analysis for Emeco Holdings

How Does Total Compensation For Ian Testrow Compare With Other Companies In The Industry?

According to our data, Emeco Holdings Limited has a market capitalization of AU$612m, and paid its CEO total annual compensation worth AU$10.0m over the year to June 2020. That's a notable decrease of 13% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$1.1m.

For comparison, other companies in the same industry with market capitalizations ranging between AU$263m and AU$1.1b had a median total CEO compensation of AU$1.2m. This suggests that Ian Testrow is paid more than the median for the industry. What's more, Ian Testrow holds AU$13m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$1.1m | AU$1.1m | 11% |

| Other | AU$8.9m | AU$10m | 89% |

| Total Compensation | AU$10.0m | AU$11m | 100% |

On an industry level, roughly 66% of total compensation represents salary and 34% is other remuneration. It's interesting to note that Emeco Holdings allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Emeco Holdings Limited's Growth Numbers

Emeco Holdings Limited's earnings per share (EPS) grew 135% per year over the last three years. It achieved revenue growth of 16% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Emeco Holdings Limited Been A Good Investment?

Given the total shareholder loss of 52% over three years, many shareholders in Emeco Holdings Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

As we touched on above, Emeco Holdings Limited is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. However, we must not forget that the EPS growth has been very strong, but shareholder returns — over the same period — have been disappointing. Considering overall performance, we can't say Ian is underpaid, in fact compensation is definitely on the higher side.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for Emeco Holdings (2 make us uncomfortable!) that you should be aware of before investing here.

Important note: Emeco Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you decide to trade Emeco Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emeco Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:EHL

Emeco Holdings

Provides surface and underground mining equipment rental, complementary equipment, and mining services in Australia.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor