Advertisement

What Westpac Banking (ASX:WBC)’s Full-Year Net Loss Reveals About Its Long-Term Earnings Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

- Westpac Banking Corporation announced its full-year financial results for the period ended September 30, 2025, reporting a net interest loss of A$93 million and an overall net loss of A$56 million.

- This marks a significant departure from previous periods, highlighting the impact of a challenging operating environment and rising cost pressures on one of Australia's major banks.

- Given the reported net loss for the year, we'll examine how this development could influence Westpac's longer-term earnings outlook and analyst expectations.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Westpac Banking Investment Narrative Recap

To be a Westpac shareholder, you need to believe the bank can weather challenging conditions in Australian banking and regain profitability despite short-term pressures like rising costs and compressed margins. The recent full-year net loss is a signal that the most important catalyst, the bank’s ability to restore stable earnings, faces meaningful short-term risk from ongoing margin and expense challenges, while the biggest risk is continued cost pressures impacting recovery. Although the impact is material, it remains to be seen if underlying operational changes can offset these headwinds.

Among recent announcements, Westpac’s board changes stand out, especially the appointment of a new Chief Executive, Consumer, in August 2025. Leadership reshuffles are closely linked to operational challenges and may play a key role as Westpac works to address ongoing risks and re-establish earnings stability. Contrast this with continual cost escalation, and it’s clear that effective management is essential as the business seeks a turnaround.

However, investors should be aware that ongoing cost pressures could still outweigh leadership changes if...

Read the full narrative on Westpac Banking (it's free!)

Westpac Banking's outlook forecasts A$24.7 billion in revenue and A$6.8 billion in earnings by 2028. This implies a 4.5% annual revenue growth rate and a decrease in earnings of A$0.3 billion from the current A$7.1 billion.

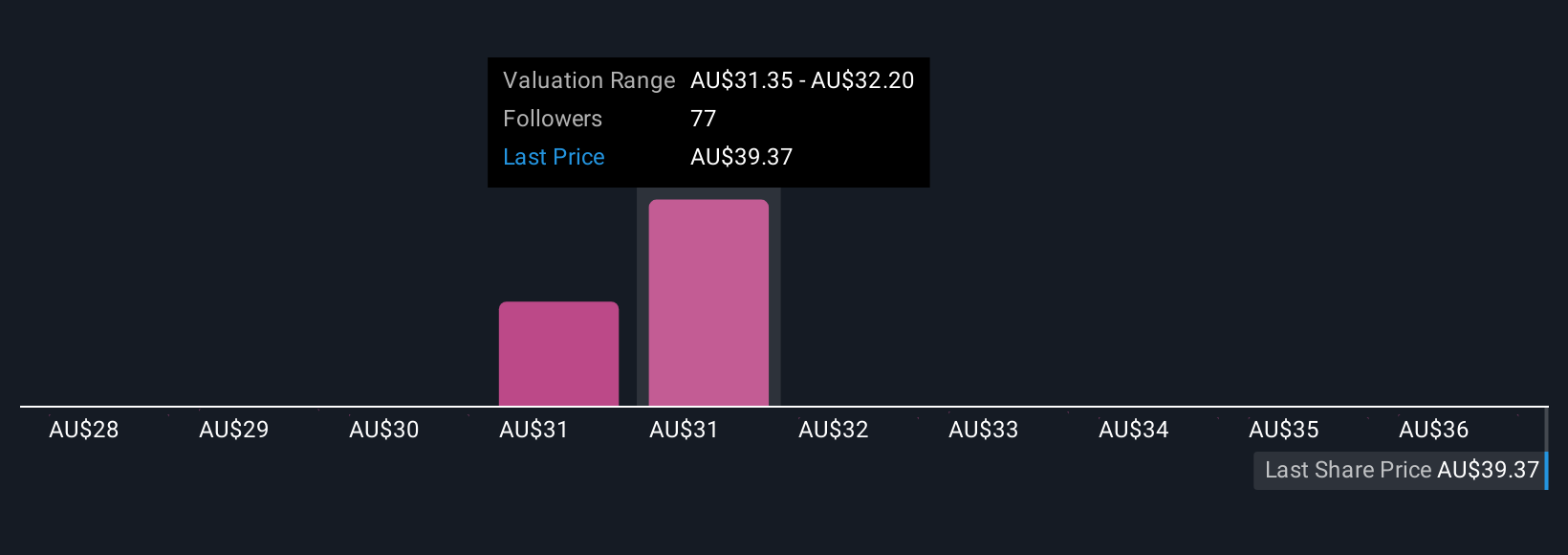

Uncover how Westpac Banking's forecasts yield a A$32.23 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members submitted 11 fair value estimates for Westpac shares ranging from A$27.95 to A$36.45, reflecting varied outlooks. With cost escalation remaining a top concern for future earnings, you can explore these differing perspectives for further insight.

Explore 11 other fair value estimates on Westpac Banking - why the stock might be worth 27% less than the current price!

Build Your Own Westpac Banking Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Westpac Banking research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Westpac Banking research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westpac Banking's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Westpac Banking might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:WBC

Westpac Banking

Provides banking and other financial services in Australia, New Zealand, the Pacific Islands, Asia, the Americas, and Europe.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor