Advertisement

Is The Market Rewarding Emirates Integrated Telecommunications Company PJSC (DFM:DU) With A Negative Sentiment As A Result Of Its Mixed Fundamentals?

It is hard to get excited after looking at Emirates Integrated Telecommunications Company PJSC's (DFM:DU) recent performance, when its stock has declined 2.5% over the past week. It seems that the market might have completely ignored the positive aspects of the company's fundamentals and decided to weigh-in more on the negative aspects. Stock prices are usually driven by a company’s financial performance over the long term, and therefore we decided to pay more attention to the company's financial performance. In this article, we decided to focus on Emirates Integrated Telecommunications Company PJSC's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

See our latest analysis for Emirates Integrated Telecommunications Company PJSC

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Emirates Integrated Telecommunications Company PJSC is:

21% = د.إ1.9b ÷ د.إ8.9b (Based on the trailing twelve months to March 2024).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each AED1 of shareholders' capital it has, the company made AED0.21 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Emirates Integrated Telecommunications Company PJSC's Earnings Growth And 21% ROE

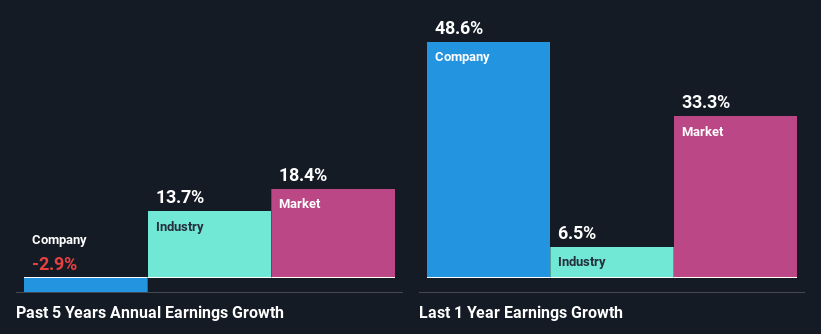

When you first look at it, Emirates Integrated Telecommunications Company PJSC's ROE doesn't look that attractive. Although a closer study shows that the company's ROE is higher than the industry average of 12% which we definitely can't overlook. However, Emirates Integrated Telecommunications Company PJSC's five year net income decline rate was 2.9%. Remember, the company's ROE is a bit low to begin with, just that it is higher than the industry average. Hence, this goes some way in explaining the shrinking earnings.

So, as a next step, we compared Emirates Integrated Telecommunications Company PJSC's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 14% over the last few years.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is DU fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Emirates Integrated Telecommunications Company PJSC Making Efficient Use Of Its Profits?

Emirates Integrated Telecommunications Company PJSC has a high three-year median payout ratio of 85% (that is, it is retaining 15% of its profits). This suggests that the company is paying most of its profits as dividends to its shareholders. This goes some way in explaining why its earnings have been shrinking. The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run.

Additionally, Emirates Integrated Telecommunications Company PJSC has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 92% of its profits over the next three years. As a result, Emirates Integrated Telecommunications Company PJSC's ROE is not expected to change by much either, which we inferred from the analyst estimate of 22% for future ROE.

Summary

In total, we're a bit ambivalent about Emirates Integrated Telecommunications Company PJSC's performance. Primarily, we are disappointed to see a lack of growth in earnings even in spite of a moderate ROE. Bear in mind, the company reinvests a small portion of its profits, which explains the lack of growth. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Valuation is complex, but we're here to simplify it.

Discover if Emirates Integrated Telecommunications Company PJSC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:DU

Emirates Integrated Telecommunications Company PJSC

Provides mobile, fixed services, broadband connectivity, and IPTV solutions to homes and businesses in the United Arab Emirates.

Outstanding track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|36.1% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|29.6% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|20.7% undervalued

MA

Community Contributor