Investors Could Be Concerned With Emirates Integrated Telecommunications Company PJSC's (DFM:DU) Returns On Capital

If you're looking at a mature business that's past the growth phase, what are some of the underlying trends that pop up? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This reveals that the company isn't compounding shareholder wealth because returns are falling and its net asset base is shrinking. Having said that, after a brief look, Emirates Integrated Telecommunications Company PJSC (DFM:DU) we aren't filled with optimism, but let's investigate further.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Emirates Integrated Telecommunications Company PJSC is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

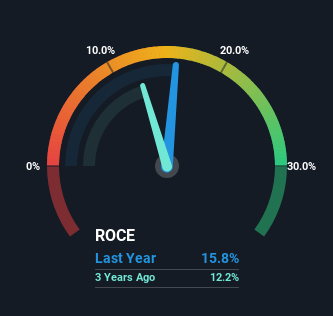

0.16 = د.إ1.7b ÷ (د.إ16b - د.إ5.5b) (Based on the trailing twelve months to September 2023).

So, Emirates Integrated Telecommunications Company PJSC has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Telecom industry average of 12% it's much better.

See our latest analysis for Emirates Integrated Telecommunications Company PJSC

Above you can see how the current ROCE for Emirates Integrated Telecommunications Company PJSC compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Emirates Integrated Telecommunications Company PJSC.

So How Is Emirates Integrated Telecommunications Company PJSC's ROCE Trending?

In terms of Emirates Integrated Telecommunications Company PJSC's historical ROCE movements, the trend doesn't inspire confidence. Unfortunately the returns on capital have diminished from the 24% that they were earning five years ago. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Emirates Integrated Telecommunications Company PJSC to turn into a multi-bagger.

The Bottom Line

In summary, it's unfortunate that Emirates Integrated Telecommunications Company PJSC is generating lower returns from the same amount of capital. Investors must expect better things on the horizon though because the stock has risen 35% in the last five years. Either way, we aren't huge fans of the current trends and so with that we think you might find better investments elsewhere.

Emirates Integrated Telecommunications Company PJSC does have some risks though, and we've spotted 1 warning sign for Emirates Integrated Telecommunications Company PJSC that you might be interested in.

While Emirates Integrated Telecommunications Company PJSC isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Emirates Integrated Telecommunications Company PJSC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:DU

Emirates Integrated Telecommunications Company PJSC

Provides carrier, data hub, internet exchange facilities, and satellite service primarily in the United Arab Emirates.

Outstanding track record with excellent balance sheet and pays a dividend.