Advertisement

- Israel

- /

- Electronic Equipment and Components

- /

- TASE:HIPR

Undiscovered Gems in the Middle East to Explore This July 2025

Simply Wall St

Reviewed by Simply Wall St

In the midst of fluctuating Gulf bourses driven by US tariff concerns and weaker oil prices, investors are navigating a complex landscape where cautious optimism is tempered by global economic uncertainties. As major indices in the region experience varied movements, with some markets like Qatar reaching new highs while others face declines, identifying promising opportunities requires a keen eye for resilience and growth potential amidst broader market challenges. In this context, uncovering undiscovered gems in the Middle East involves looking for stocks that demonstrate strong fundamentals and adaptability to shifting economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Baazeem Trading | 8.48% | -2.02% | -2.70% | ★★★★★★ |

| MOBI Industry | 6.50% | 5.60% | 24.00% | ★★★★★★ |

| Sure Global Tech | NA | 11.95% | 18.65% | ★★★★★★ |

| Nofoth Food Products | NA | 15.75% | 27.63% | ★★★★★★ |

| Etihad Atheeb Telecommunication | 1.05% | 36.24% | 62.25% | ★★★★★★ |

| Najran Cement | 14.20% | -2.87% | -22.60% | ★★★★★★ |

| National General Insurance (P.J.S.C.) | NA | 14.55% | 29.05% | ★★★★★☆ |

| National Corporation for Tourism and Hotels | 19.25% | 0.67% | 4.89% | ★★★★☆☆ |

| National Environmental Recycling | 69.43% | 43.47% | 32.77% | ★★★★☆☆ |

| Saudi Chemical Holding | 79.49% | 16.57% | 44.01% | ★★★★☆☆ |

We'll examine a selection from our screener results.

National General Insurance (P.J.S.C.) (DFM:NGI)

Simply Wall St Value Rating: ★★★★★☆

Overview: National General Insurance Co. (P.J.S.C.) operates in the United Arab Emirates, focusing on underwriting life, general insurance, and reinsurance, with a market capitalization of approximately AED1.07 billion.

Operations: NGI generates revenue primarily from its insurance segment, amounting to AED869.21 million. The company reports a market capitalization of around AED1.07 billion and includes a segment adjustment of AED120.97 million in its financials.

With a price-to-earnings ratio of 8.1x, National General Insurance (NGI) stands out for its value compared to the AE market average of 13.2x. This debt-free company has shown impressive earnings growth, up 31.6% over the past year, significantly outperforming the insurance industry's -9.4%. Despite recent share price volatility, NGI's high level of non-cash earnings reflects strong quality in its financials. The company's Q1 2025 net income reached AED 35.58 million, an increase from AED 30.32 million last year, with basic earnings per share rising to AED 0.22 from AED 0.18.

Gipta Ofis Kirtasiye ve Promosyon Ürünleri Imalat Sanayi (IBSE:GIPTA)

Simply Wall St Value Rating: ★★★★★☆

Overview: Gipta Ofis Kirtasiye ve Promosyon Ürünleri Imalat Sanayi A.S. is engaged in the manufacturing of office stationery and promotional products, with a market capitalization of TRY14.99 billion.

Operations: Gipta generates its revenue primarily from the Paper & Paper Products segment, which brought in TRY1.89 billion.

Gipta Ofis Kirtasiye ve Promosyon Ürünleri Imalat Sanayi, a small player in the commercial services sector, has shown remarkable earnings growth of 375.7% over the past year, significantly outpacing the industry average of 8.7%. The company is financially robust with more cash than total debt and generates sufficient interest income to cover its obligations. Despite reporting a net loss of TRY 41.99 million for Q1 2025, down from TRY 96.49 million a year ago, Gipta remains profitable with positive free cash flow and high-quality non-cash earnings contributing to its financial health.

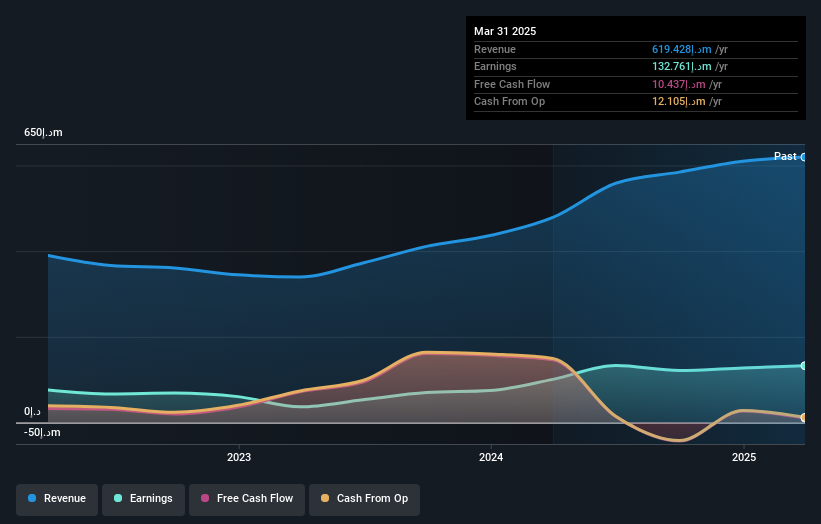

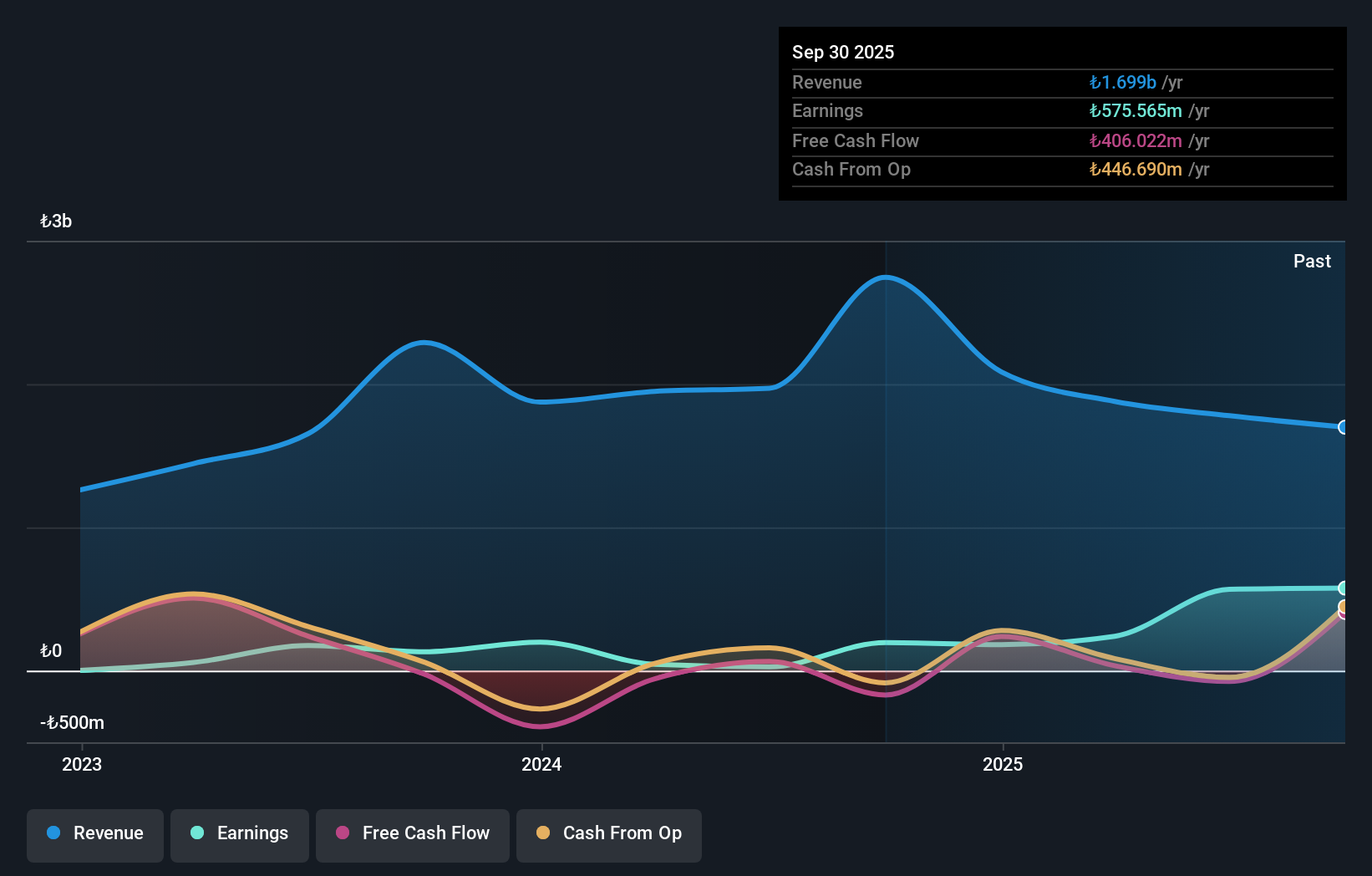

Hiper Global (TASE:HIPR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hiper Global Ltd. specializes in delivering computing solutions to OEM customers, with a market capitalization of ₪882.07 million.

Operations: Hiper Global Ltd. generates revenue primarily from its OEM activity, amounting to $268.34 million. The company's cost structure and profitability metrics are not detailed in the provided information, limiting further analysis of financial performance trends.

Hiper Global, a smaller player in the electronics sector, has demonstrated solid financial management over the past five years. The debt to equity ratio dropped from 53.5% to 29%, highlighting improved leverage control. Despite experiencing a -2.4% earnings growth last year, contrasting with the industry’s 10.3%, its net debt to equity ratio of 22.8% remains satisfactory and interest payments are well covered by EBIT at 16.9 times coverage. Recent earnings showed a dip in sales from US$85 million to US$80 million and net income slightly decreased from US$5 million to US$4 million, indicating some challenges ahead but also potential for recovery.

- Click here and access our complete health analysis report to understand the dynamics of Hiper Global.

Gain insights into Hiper Global's historical performance by reviewing our past performance report.

Key Takeaways

- Investigate our full lineup of 221 Middle Eastern Undiscovered Gems With Strong Fundamentals right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hiper Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:HIPR

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor