Advertisement

- United Arab Emirates

- /

- Insurance

- /

- ADX:HAYAH

Investors Appear Satisfied With HAYAH Insurance Company P.J.S.C.'s (ADX:HAYAH) Prospects As Shares Rocket 28%

HAYAH Insurance Company P.J.S.C. (ADX:HAYAH) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 34% in the last year.

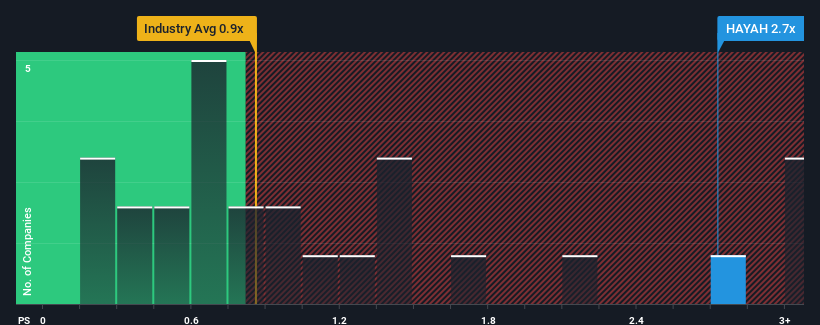

Since its price has surged higher, when almost half of the companies in the United Arab Emirates' Insurance industry have price-to-sales ratios (or "P/S") below 0.9x, you may consider HAYAH Insurance Company P.J.S.C as a stock probably not worth researching with its 2.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for HAYAH Insurance Company P.J.S.C

What Does HAYAH Insurance Company P.J.S.C's Recent Performance Look Like?

HAYAH Insurance Company P.J.S.C has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on HAYAH Insurance Company P.J.S.C will help you shine a light on its historical performance.How Is HAYAH Insurance Company P.J.S.C's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as HAYAH Insurance Company P.J.S.C's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 13% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 157% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to decline by 9.1% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this in mind, it's clear to us why HAYAH Insurance Company P.J.S.C's P/S exceeds that of its industry peers. Investors are willing to pay more for a stock they hope will buck the trend of the broader industry going backwards. However, its current revenue trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Final Word

HAYAH Insurance Company P.J.S.C shares have taken a big step in a northerly direction, but its P/S is elevated as a result. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of HAYAH Insurance Company P.J.S.C revealed its growing revenue over the medium-term is helping prop up its high P/S compared to its peers, given the industry is set to shrink. It could be said that investors feel this revenue growth will continue into the future, justifying a higher P/S ratio. We still remain cautious about the company's ability to stay its recent course and swim against the current of the broader industry turmoil. Otherwise, it's hard to see the share price falling strongly in the near future if its revenue performance persists.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for HAYAH Insurance Company P.J.S.C that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if HAYAH Insurance Company P.J.S.C might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ADX:HAYAH

HAYAH Insurance Company P.J.S.C

Provides health and life insurance solutions in the United Arab Emirates and internationally.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor