Advertisement

- United Arab Emirates

- /

- Beverage

- /

- DFM:ERC

Emirates Refreshments (P.S.C.) (DFM:ERC) Is Posting Healthy Earnings, But It Is Not All Good News

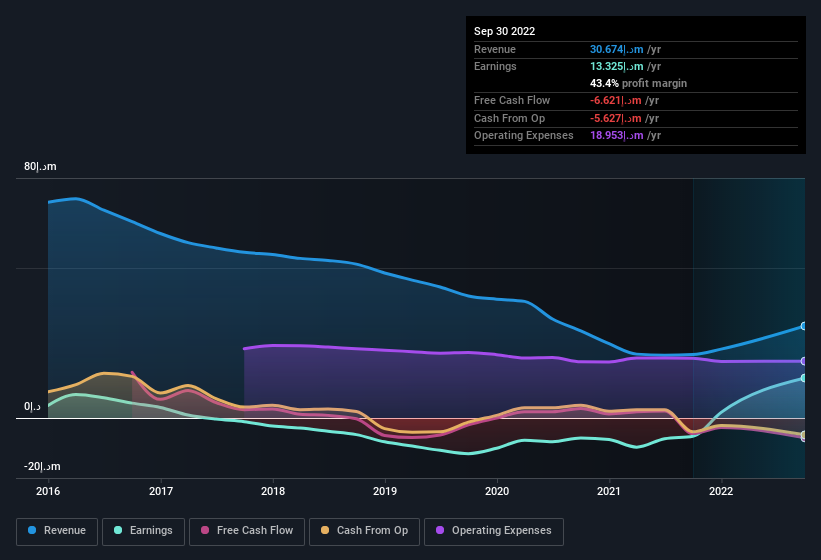

The latest earnings release from Emirates Refreshments (P.S.C.) (DFM:ERC ) disappointed investors. We did some digging and found some underlying numbers that are worrying.

Our analysis indicates that ERC is potentially overvalued!

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Emirates Refreshments (P.S.C.) issued 966% more new shares over the last year. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Emirates Refreshments (P.S.C.)'s historical EPS growth by clicking on this link.

A Look At The Impact Of Emirates Refreshments (P.S.C.)'s Dilution On Its Earnings Per Share (EPS)

Emirates Refreshments (P.S.C.) was losing money three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if Emirates Refreshments (P.S.C.)'s earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Emirates Refreshments (P.S.C.).

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Emirates Refreshments (P.S.C.)'s profit was boosted by unusual items worth د.إ19m in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Emirates Refreshments (P.S.C.) had a rather significant contribution from unusual items relative to its profit to September 2022. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Emirates Refreshments (P.S.C.)'s Profit Performance

In its last report Emirates Refreshments (P.S.C.) benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. On reflection, the above-mentioned factors give us the strong impression that Emirates Refreshments (P.S.C.)'sunderlying earnings power is not as good as it might seem, based on the statutory profit numbers. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Every company has risks, and we've spotted 3 warning signs for Emirates Refreshments (P.S.C.) (of which 1 shouldn't be ignored!) you should know about.

Our examination of Emirates Refreshments (P.S.C.) has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Emirates Reem Investments Company P.J.S.C might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:ERC

Emirates Reem Investments Company P.J.S.C

Engages in the bottling, distribution, and trading of mineral water, carbonated drinks, soft drinks, juices, and evaporated milk in the United Arab Emirates, rest of the Middle East, and Africa.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor