- United Arab Emirates

- /

- Consumer Services

- /

- ADX:DRIVE

Emirates Driving Company P.J.S.C.'s (ADX:DRIVE) Stock Has Seen Strong Momentum: Does That Call For Deeper Study Of Its Financial Prospects?

Most readers would already be aware that Emirates Driving Company P.J.S.C's (ADX:DRIVE) stock increased significantly by 16% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Particularly, we will be paying attention to Emirates Driving Company P.J.S.C's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for Emirates Driving Company P.J.S.C

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Emirates Driving Company P.J.S.C is:

18% = د.إ128m ÷ د.إ725m (Based on the trailing twelve months to December 2020).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each AED1 of shareholders' capital it has, the company made AED0.18 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Emirates Driving Company P.J.S.C's Earnings Growth And 18% ROE

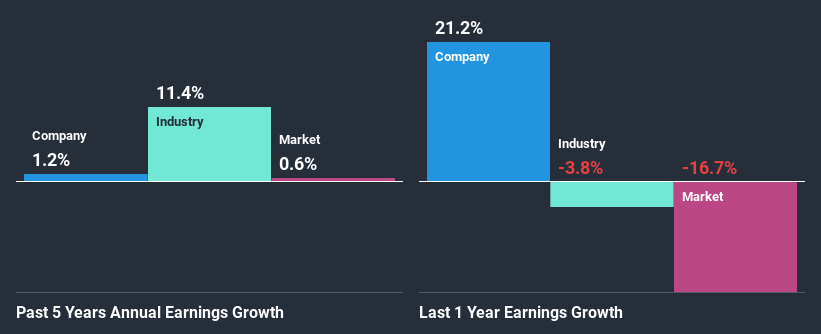

To start with, Emirates Driving Company P.J.S.C's ROE looks acceptable. Especially when compared to the industry average of 10% the company's ROE looks pretty impressive. Despite this, Emirates Driving Company P.J.S.C's five year net income growth was quite flat over the past five years. Therefore, there could be some other aspects that could potentially be preventing the company from growing. These include low earnings retention or poor allocation of capital.

Next, on comparing with the industry net income growth, we found that Emirates Driving Company P.J.S.C's reported growth was lower than the industry growth of 13% in the same period, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Emirates Driving Company P.J.S.C's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Emirates Driving Company P.J.S.C Efficiently Re-investing Its Profits?

With a high three-year median payout ratio of 72% (implying that the company keeps only 28% of its income) of its business to reinvest into its business), most of Emirates Driving Company P.J.S.C's profits are being paid to shareholders, which explains the absence of growth in earnings.

Moreover, Emirates Driving Company P.J.S.C has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Conclusion

On the whole, we do feel that Emirates Driving Company P.J.S.C has some positive attributes. However, while the company does have a high ROE, its earnings growth number is quite disappointing. This can be blamed on the fact that it reinvests only a small portion of its profits and pays out the rest as dividends. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. You can do your own research on Emirates Driving Company P.J.S.C and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

If you’re looking to trade Emirates Driving Company P.J.S.C, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Emirates Driving Company P.J.S.C, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Emirates Driving Company P.J.S.C might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ADX:DRIVE

Emirates Driving Company P.J.S.C

Manages and develops motor vehicles driving training in the United Arab Emirates.

Flawless balance sheet, undervalued and pays a dividend.