Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:ZYNE

Zynerba Pharmaceuticals, Inc. (NASDAQ:ZYNE): Are Analysts Optimistic?

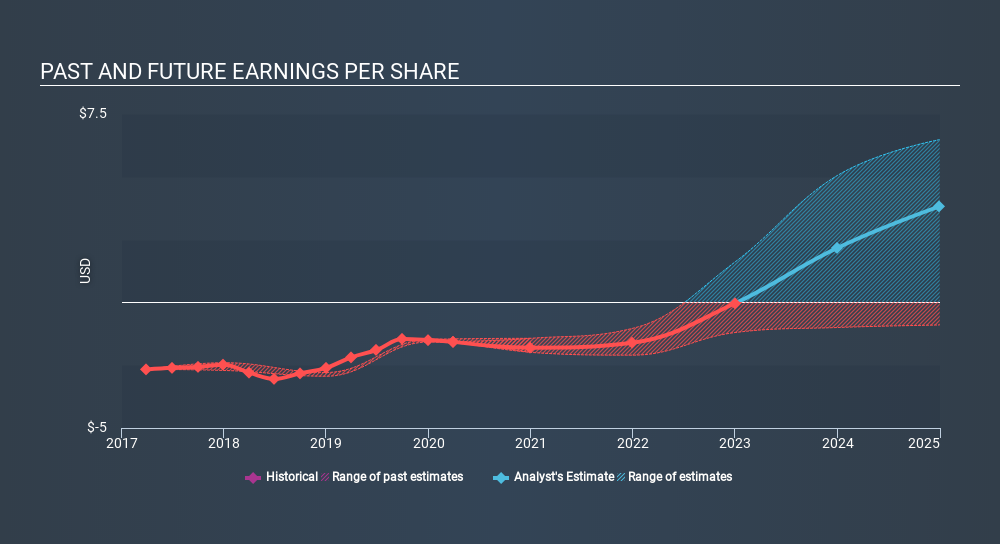

Zynerba Pharmaceuticals, Inc.'s (NASDAQ:ZYNE): Zynerba Pharmaceuticals, Inc. operates as a clinical stage specialty pharmaceutical company. With the latest financial year loss of -US$32.9m and a trailing-twelve month of -US$36.1m, the US$140m market-cap amplifies its loss by moving further away from its breakeven target. As path to profitability is the topic on ZYNE’s investors mind, I’ve decided to gauge market sentiment. Below I will provide a high-level summary of the industry analysts’ expectations for ZYNE.

See our latest analysis for Zynerba Pharmaceuticals

According to the 7 industry analysts covering ZYNE, the consensus is breakeven is near. They expect the company to post a final loss in 2021, before turning a profit of US$789k in 2022. ZYNE is therefore projected to breakeven around 2 years from today. How fast will ZYNE have to grow each year in order to reach the breakeven point by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 79% year-on-year, on average, which is rather optimistic! If this rate turns out to be too aggressive, ZYNE may become profitable much later than analysts predict.

Given this is a high-level overview, I won’t go into details of ZYNE’s upcoming projects, however, keep in mind that generally pharmaceuticals, depending on the stage of product development, have irregular periods of cash flow. This means that a high growth rate is not unusual, especially if the company is currently in an investment period.

One thing I’d like to point out is that ZYNE has no debt on its balance sheet, which is rare for a loss-making pharma, which typically has high debt relative to its equity. ZYNE currently operates purely off its shareholder funding and has no debt obligation, reducing concerns around repayments and making it a less risky investment.

Next Steps:

There are key fundamentals of ZYNE which are not covered in this article, but I must stress again that this is merely a basic overview. For a more comprehensive look at ZYNE, take a look at ZYNE’s company page on Simply Wall St. I’ve also put together a list of pertinent aspects you should further examine:

- Valuation: What is ZYNE worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether ZYNE is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Zynerba Pharmaceuticals’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NasdaqCM:ZYNE

Zynerba Pharmaceuticals

Zynerba Pharmaceuticals, Inc. operates as a clinical stage specialty pharmaceutical company.

Medium-low with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

160 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

JR

JRY on Bloom Energy ·

The Bloom Story is early days

Fair Value:US$386.143.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CH

ChuckN on NextEra Energy ·

Investor Thesis: Why the NextEra Energy / Dominion Energy Merger Could Be a Major AI Power Infrastructure Event

Fair Value:US$93.719.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

283 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

167 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0