Advertisement

- United States

- /

- Life Sciences

- /

- NYSE:WAT

When Should You Buy Waters Corporation (NYSE:WAT)?

Let's talk about the popular Waters Corporation (NYSE:WAT). The company's shares saw a significant share price rise of over 20% in the past couple of months on the NYSE. With many analysts covering the large-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Let’s take a look at Waters’s outlook and value based on the most recent financial data to see if the opportunity still exists.

View our latest analysis for Waters

Is Waters still cheap?

Good news, investors! Waters is still a bargain right now according to my price multiple model, which compares the company's price-to-earnings ratio to the industry average. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 26.64x is currently well-below the industry average of 41.8x, meaning that it is trading at a cheaper price relative to its peers. Another thing to keep in mind is that Waters’s share price is quite stable relative to the rest of the market, as indicated by its low beta. This means that if you believe the current share price should move towards its industry peers, a low beta could suggest it is not likely to reach that level anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range again.

What kind of growth will Waters generate?

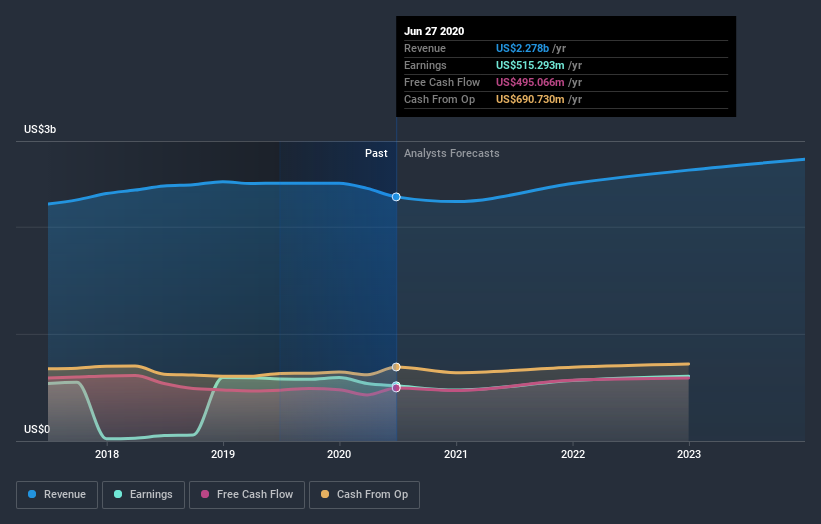

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to grow by a double-digit 13% over the next couple of years, the outlook is positive for Waters. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? Since WAT is currently trading below the industry PE ratio, it may be a great time to increase your holdings in the stock. With an optimistic profit outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as financial health to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on WAT for a while, now might be the time to make a leap. Its buoyant future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy WAT. But before you make any investment decisions, consider other factors such as the strength of its balance sheet, in order to make a well-informed investment decision.

With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. In terms of investment risks, we've identified 1 warning sign with Waters, and understanding it should be part of your investment process.

If you are no longer interested in Waters, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you’re looking to trade Waters, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Waters might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:WAT

Waters

Provides analytical workflow solutions in Asia, the Americas, and Europe.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

49 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

53 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$18326.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Rox Resources ·

Developer to Producer: Debt-Free Path, A$965M Post-Tax NPV, and Massive Gold Leverage

Fair Value:AU$6.1693.3% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

JO

John_Eric on MercadoLibre ·

MercadoLibre and the Spreadsheet Trick That Decides Everything

Fair Value:US$4.72k60.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

86 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7107.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative