Advertisement

- United Kingdom

- /

- Personal Products

- /

- AIM:W7L

What Warpaint London PLC's (LON:W7L) ROE Can Tell Us

While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. By way of learning-by-doing, we'll look at ROE to gain a better understanding of Warpaint London PLC (LON:W7L).

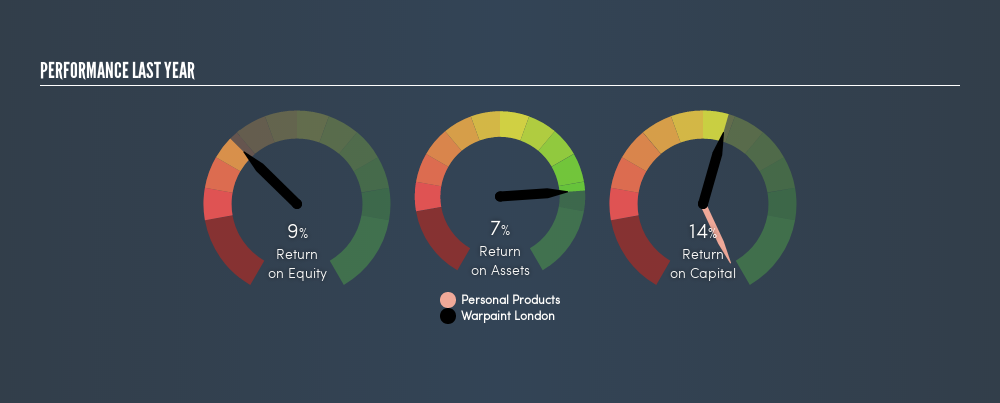

Our data shows Warpaint London has a return on equity of 8.7% for the last year. Another way to think of that is that for every £1 worth of equity in the company, it was able to earn £0.087.

View our latest analysis for Warpaint London

How Do I Calculate ROE?

The formula for ROE is:

Return on Equity = Net Profit ÷ Shareholders' Equity

Or for Warpaint London:

8.7% = UK£3.6m ÷ UK£41m (Based on the trailing twelve months to December 2018.)

Most readers would understand what net profit is, but it’s worth explaining the concept of shareholders’ equity. It is all the money paid into the company from shareholders, plus any earnings retained. Shareholders' equity can be calculated by subtracting the total liabilities of the company from the total assets of the company.

What Does ROE Mean?

ROE measures a company's profitability against the profit it retains, and any outside investments. The 'return' is the profit over the last twelve months. A higher profit will lead to a higher ROE. So, all else equal, investors should like a high ROE. Clearly, then, one can use ROE to compare different companies.

Does Warpaint London Have A Good ROE?

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. The limitation of this approach is that some companies are quite different from others, even within the same industry classification. You can see in the graphic below that Warpaint London has an ROE that is fairly close to the average for the Personal Products industry (8.7%).

That's neither particularly good, nor bad. ROE tells us about the quality of the business, but it does not give us much of an idea if the share price is cheap. If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

How Does Debt Impact ROE?

Most companies need money -- from somewhere -- to grow their profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the first and second cases, the ROE will reflect this use of cash for investment in the business. In the latter case, the debt used for growth will improve returns, but won't affect the total equity. In this manner the use of debt will boost ROE, even though the core economics of the business stay the same.

Warpaint London's Debt And Its 8.7% ROE

Warpaint London has a debt to equity ratio of just 0.052, which is very low. I'm not impressed with its ROE, but the debt levels are not too high, indicating the business has decent prospects. Careful use of debt to boost returns is often very good for shareholders. However, it could reduce the company's ability to take advantage of future opportunities.

The Key Takeaway

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. Companies that can achieve high returns on equity without too much debt are generally of good quality. If two companies have around the same level of debt to equity, and one has a higher ROE, I'd generally prefer the one with higher ROE.

But when a business is high quality, the market often bids it up to a price that reflects this. The rate at which profits are likely to grow, relative to the expectations of profit growth reflected in the current price, must be considered, too. So you might want to take a peek at this data-rich interactive graph of forecasts for the company.

But note: Warpaint London may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About AIM:W7L

Warpaint London

Produces and sells cosmetics.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

39 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

44 followersusers have followed this narrative

1 commentusers have commented on this narrative

12 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AN

AndyB72 on NNN REIT ·

NNN - National Retail Properties Inc. | I'm on 75% position and waiting to buy more.

Fair Value:US$46.422.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$123.1515.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AD

Addu0g on iShares Gold Trust ·

iShares Gold Trust will Boost Future PE by 2.7% over Five Years

Fair Value:US$10324.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative