Michael Binnion became the CEO of Questerre Energy Corporation (TSE:QEC) in 2000, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

See our latest analysis for Questerre Energy

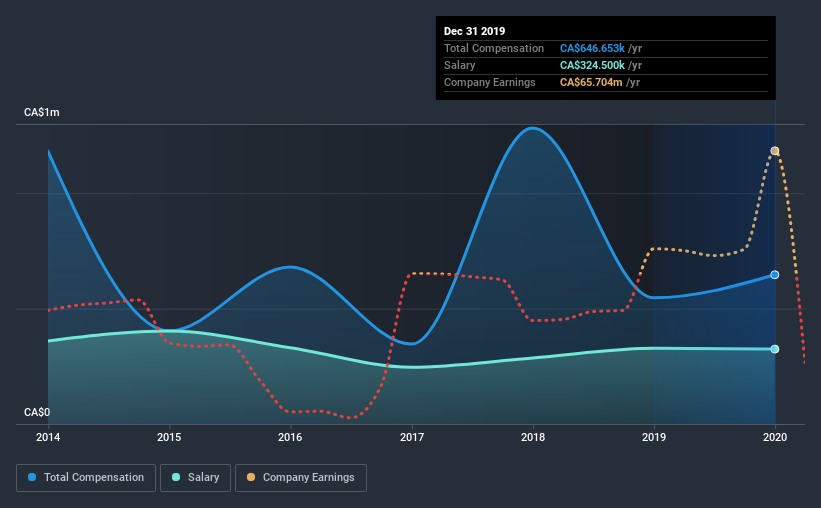

Comparing Questerre Energy Corporation's CEO Compensation With the industry

According to our data, Questerre Energy Corporation has a market capitalization of CA$51m, and paid its CEO total annual compensation worth CA$647k over the year to December 2019. Notably, that's an increase of 18% over the year before. In particular, the salary of CA$324.5k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under CA$266m, the reported median total CEO compensation was CA$369k. This suggests that Michael Binnion is paid more than the median for the industry. Furthermore, Michael Binnion directly owns CA$1.4m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | CA$325k | CA$328k | 50% |

| Other | CA$322k | CA$219k | 50% |

| Total Compensation | CA$647k | CA$547k | 100% |

On an industry level, around 43% of total compensation represents salary and 57% is other remuneration. According to our research, Questerre Energy has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Questerre Energy Corporation's Growth

Questerre Energy Corporation's earnings per share (EPS) grew 39% per year over the last three years. It achieved revenue growth of 6.9% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Questerre Energy Corporation Been A Good Investment?

Given the total shareholder loss of 86% over three years, many shareholders in Questerre Energy Corporation are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As previously discussed, Michael is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. But the company has impressed with its earnings per share growth, but shareholder returns — over the same period — have been disappointing. Considering overall performance, we can't say Michael is underpaid, in fact compensation is definitely on the higher side.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 2 warning signs for Questerre Energy that investors should look into moving forward.

Important note: Questerre Energy is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you decide to trade Questerre Energy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Questerre Energy, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Questerre Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TSX:QEC

Questerre Energy

An energy technology and innovation company, acquires, explores, and develops non-conventional oil and gas projects in Canada.

Adequate balance sheet minimal.