- United States

- /

- Banks

- /

- NYSE:WFC

Wells Fargo (NYSE:WFC) Appoints Tim Ruby As New Division Executive For Key Sectors

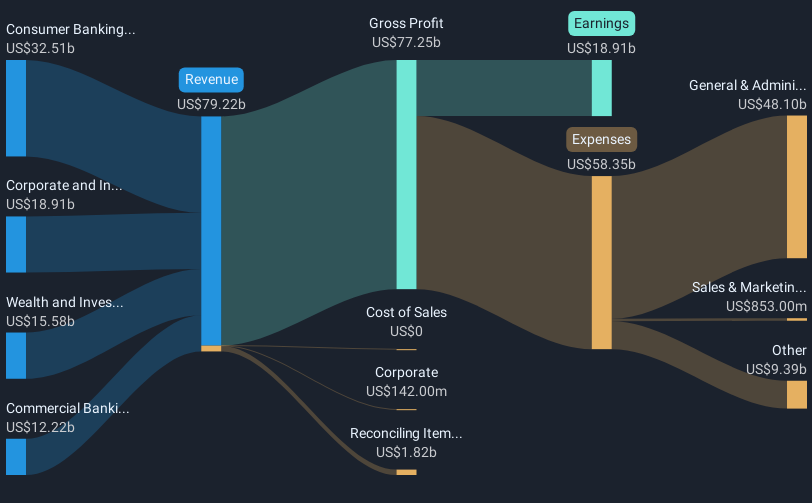

Wells Fargo (NYSE:WFC) recently appointed Tim Ruby as Division Executive for its Healthcare, Higher Education, and Not-for-Profit division. During this period, the company's share price rose by 32%, significantly outperforming the market's 13% increase over the past year. This impressive gain may have been supported by a series of developments, including the announcement of a $40 billion share repurchase program and increases in dividend payouts. These strategic moves potentially added weight to the upward price momentum, aligning with broader market trends, which forecast annual earnings growth of 15%.

We've discovered 1 risk for Wells Fargo that you should be aware of before investing here.

The recent appointment of Tim Ruby as Division Executive may bolster Wells Fargo's strategic focus, potentially enhancing its risk controls and efficiency, aligning with its aim to reduce regulatory burdens. This move could positively influence earnings, especially given the company's expansion into fee-based revenue streams and strategic partnerships in the credit and auto sectors. Analysts have forecasted increasing revenues and a potential stabilizing effect on earnings margins, highlighting the importance of management changes in driving these outcomes.

Over the past five years, Wells Fargo's total return, including dividends, has impressively reached nearly 270.34%, illustrating the company's strong performance. However, in the more immediate term, the company's share price has risen 32% over the past year, outperforming the broader market's 13% increase. This contrast showcases Wells Fargo's capacity to exceed industry expectations in the short term while maintaining substantial long-term growth.

The projected revenue growth, tied to recent developments such as consent orders and partnerships, indicates a promising outlook. Analysts expect a conservative annual revenue increase of 5.1% over the next three years and minor compression in profit margins. With the current share price of US$81.59 and an analyst consensus price target of US$86.45, the market perceives the stock as having modest headroom for appreciation. While the execution of these developments is crucial, they signal confidence in the bank's future profitability and shareholder value enhancements.

Take a closer look at Wells Fargo's potential here in our financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wells Fargo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WFC

Wells Fargo

A financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

When GPS fails: this small cap is fixing a $54B drone problem

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Recently Updated Narratives

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

$CRI Creotech Instruments (WSE:CRI): Two Minute Drill

LVMH’s Cash Flow Is Holding Up, But The Stock Still Needs A Better Entry Point

Popular Narratives

Mastercard: The Best Dividend Stock You're Ignoring

Adobe: A Probabilistic Case for Undervaluation

A Capital Allocation Favorite with Structural Importance

Trending Discussion