Advertisement

We Think Excelpoint Technology's (SGX:BDF) Statutory Profit Might Understate Its Earnings Potential

Broadly speaking, profitable businesses are less risky than unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Excelpoint Technology's (SGX:BDF) statutory profits are a good guide to its underlying earnings.

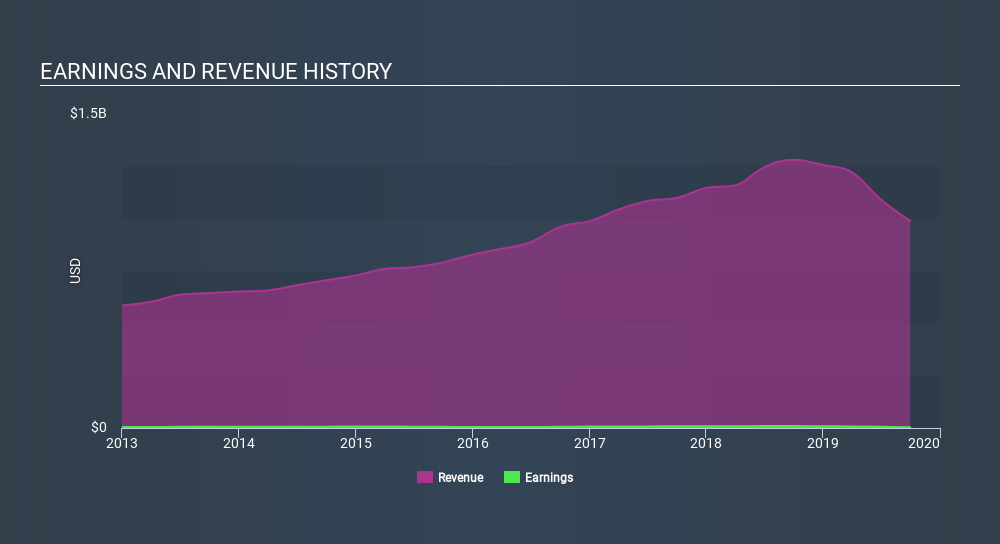

It's good to see that over the last twelve months Excelpoint Technology made a profit of US$3.19m on revenue of US$989.8m. As you can see in the chart below, its profit has declined over the last three years, even though its revenue has increased.

See our latest analysis for Excelpoint Technology

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. Therefore, we think it's worth taking a closer look at Excelpoint Technology's cashflow, as well as examining the impact that unusual items have had on its reported profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Excelpoint Technology.

A Closer Look At Excelpoint Technology's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Excelpoint Technology has an accrual ratio of -0.36 for the year to September 2019. That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow. To wit, it produced free cash flow of US$74m during the period, dwarfing its reported profit of US$3.19m. Notably, Excelpoint Technology had negative free cash flow last year, so the US$74m it produced this year was a welcome improvement.

However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

The Impact Of Unusual Items On Profit

Excelpoint Technology's profit was reduced by unusual items worth US$1.7m in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. This is what you'd expect to see where a company has a non-cash charge reducing paper profits. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. If Excelpoint Technology doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Excelpoint Technology's Profit Performance

In conclusion, both Excelpoint Technology's accrual ratio and its unusual items suggest that its statutory earnings are probably reasonably conservative. Based on these factors, we think Excelpoint Technology's underlying earnings potential is as good as, or probably even better, than the statutory profit makes it seem! Just as investors must consider earnings, it is also important to take into account the strength of a company's balance sheet. If you're interestedwe have a graphic representation of Excelpoint Technology's balance sheet.

After our examination into the nature of Excelpoint Technology's profit, we've come away optimistic for the company. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SGX:BDF

Excelpoint Technology

Excelpoint Technology Ltd., an investment holding company, provides electronic components, and engineering design, and supply chain management services.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on EPB Group Berhad ·

EPB: Strong Shareholder Backing, Continuous Insider Buying and Growth Opportunities Ahead

Fair Value:RM 0.548.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative