Advertisement

- United Kingdom

- /

- Luxury

- /

- LSE:BRBY

UK Market Highlights 3 Stocks Including Burberry Group That May Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

In recent times, the UK market has faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China and global economic uncertainties. As these conditions unfold, investors often seek opportunities in stocks that may be trading below their estimated value, offering potential for growth when broader market dynamics stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Topps Tiles (LSE:TPT) | £0.38 | £0.7 | 45.6% |

| TBC Bank Group (LSE:TBCG) | £48.55 | £96.40 | 49.6% |

| Moonpig Group (LSE:MOON) | £2.105 | £4.03 | 47.7% |

| Marlowe (AIM:MRL) | £4.39 | £8.37 | 47.5% |

| LSL Property Services (LSE:LSL) | £2.99 | £5.88 | 49.1% |

| Gooch & Housego (AIM:GHH) | £6.18 | £11.16 | 44.6% |

| Franchise Brands (AIM:FRAN) | £1.36 | £2.68 | 49.2% |

| Fintel (AIM:FNTL) | £2.37 | £4.28 | 44.6% |

| Essentra (LSE:ESNT) | £1.044 | £1.93 | 46% |

| Begbies Traynor Group (AIM:BEG) | £1.21 | £2.26 | 46.3% |

Here's a peek at a few of the choices from the screener.

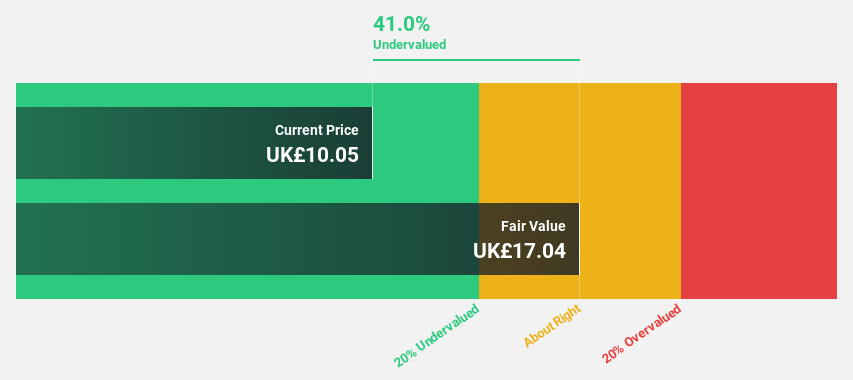

Burberry Group (LSE:BRBY)

Overview: Burberry Group plc, with a market cap of £4.80 billion, operates in the manufacturing, retail, and wholesale of luxury goods under the Burberry brand across regions including Asia Pacific, Europe, the Middle East, India, Africa, and the Americas.

Operations: The company's revenue is primarily derived from Retail/Wholesale at £2.40 billion and Licensing at £67 million.

Estimated Discount To Fair Value: 44.2%

Burberry Group is trading at £13.36, significantly below its estimated fair value of £23.93, suggesting it may be undervalued based on cash flows. Despite a recent revenue decline to £433 million and negative comparable store sales, Burberry's earnings are forecast to grow 48.51% annually, outpacing the UK market's average growth rate. However, challenges persist as the company reported a net loss of £75 million for the full year ended March 2025 and expects wholesale revenue declines in fiscal year 2026.

- Our comprehensive growth report raises the possibility that Burberry Group is poised for substantial financial growth.

- Dive into the specifics of Burberry Group here with our thorough financial health report.

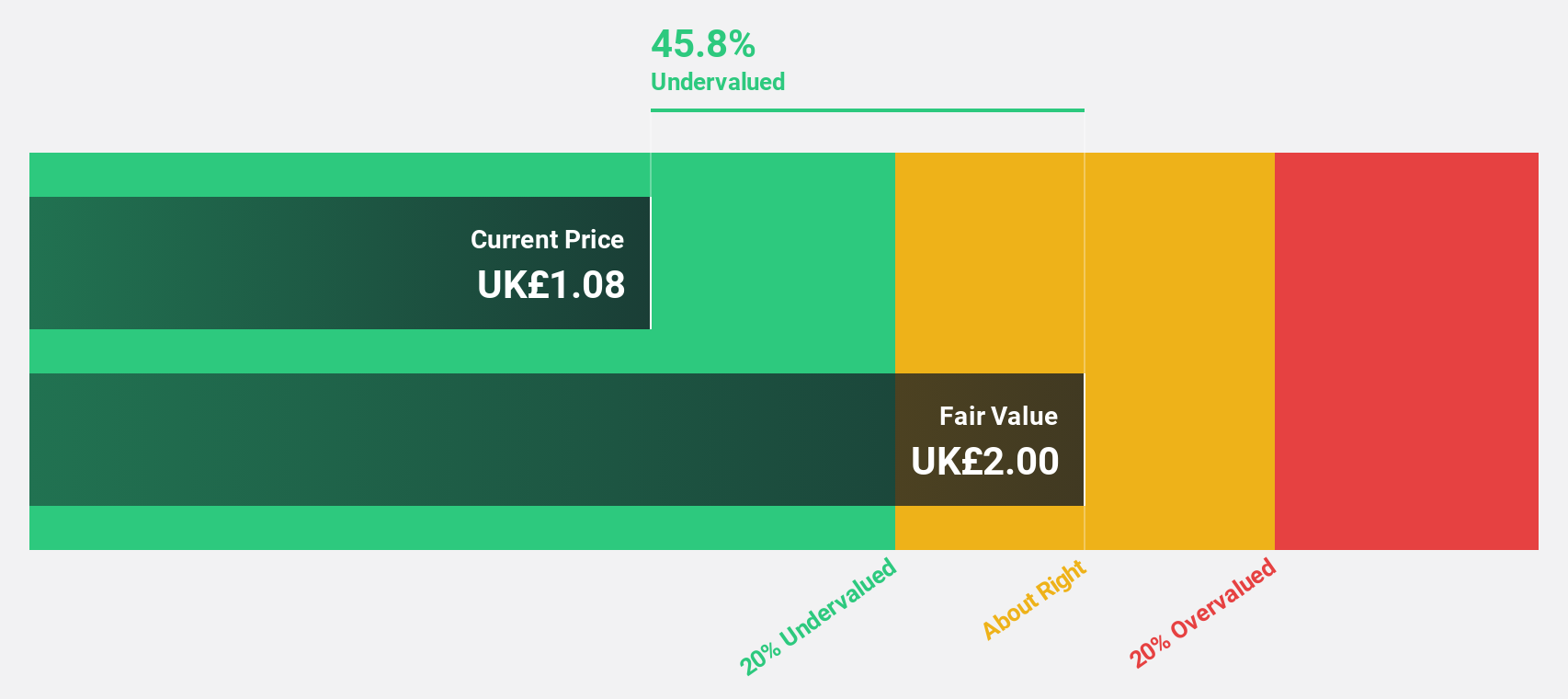

Essentra (LSE:ESNT)

Overview: Essentra plc is involved in the manufacturing and distribution of plastic injection moulded, vinyl dip moulded, and metal items across Europe, the Middle East, Africa, the Americas, and the Asia Pacific with a market cap of £298.29 million.

Operations: Essentra's revenue is derived from the manufacturing and distribution of plastic injection moulded, vinyl dip moulded, and metal products across its global markets.

Estimated Discount To Fair Value: 46%

Essentra is trading at £1.04, below its estimated fair value of £1.93, highlighting potential undervaluation based on cash flows. Despite a drop in sales to £152.4 million and net income to £0.3 million for H1 2025, earnings are forecast to grow significantly at 38.6% annually, surpassing UK market averages. However, the dividend yield of 2.68% is not well covered by earnings and recent large one-off items have impacted financial results.

- Our expertly prepared growth report on Essentra implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Essentra.

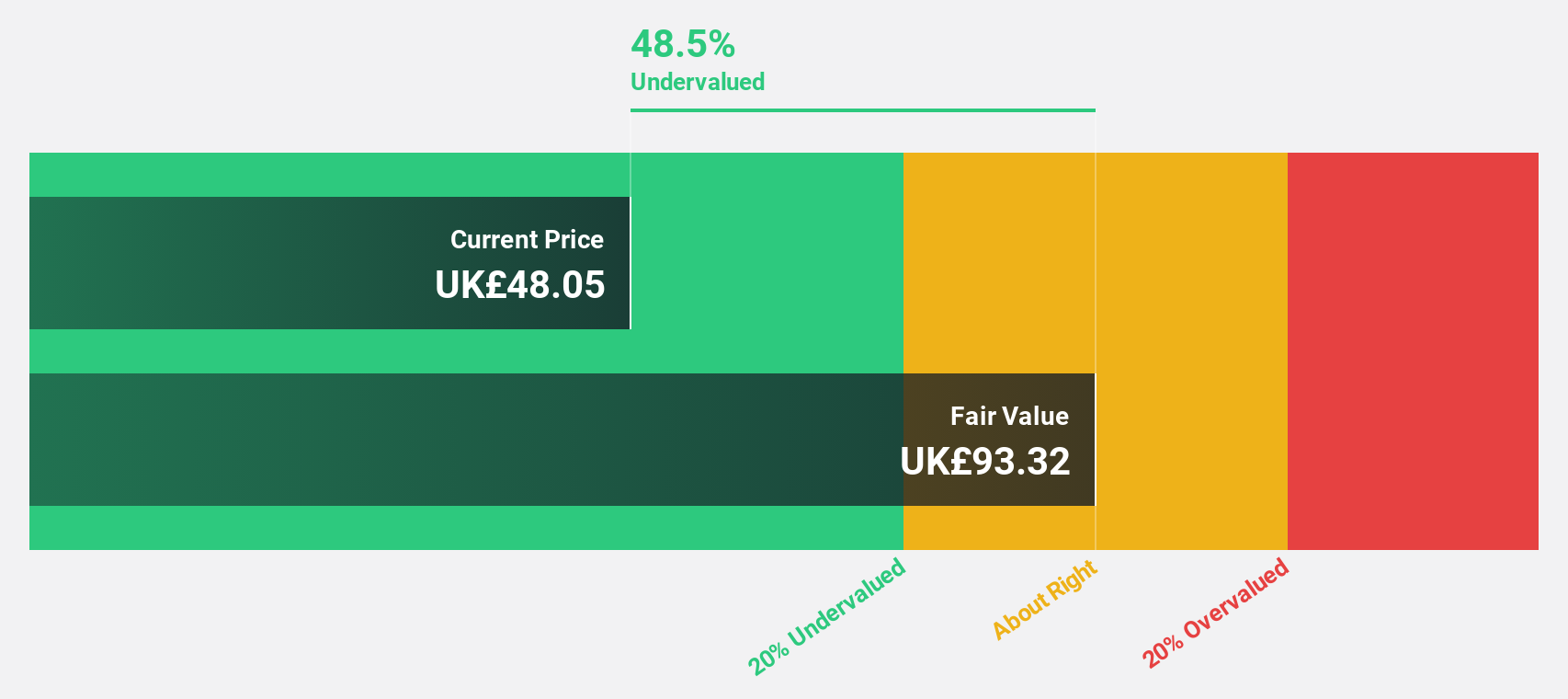

TBC Bank Group (LSE:TBCG)

Overview: TBC Bank Group PLC, with a market cap of £2.69 billion, operates through its subsidiaries to offer banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan.

Operations: The company's revenue is primarily derived from Georgian Financial Services, which generated GEL 2.34 billion.

Estimated Discount To Fair Value: 49.6%

TBC Bank Group is trading at £48.55, significantly below its estimated fair value of £96.4, suggesting potential undervaluation based on cash flows. The bank's earnings have grown 23.9% annually over the past five years and are forecast to grow 17.2% per year, outpacing the UK market average. Despite a high level of bad loans at 2.5%, TBC maintains strong revenue growth expectations at 21.6% annually, driven by robust net interest income increases.

- The growth report we've compiled suggests that TBC Bank Group's future prospects could be on the up.

- Take a closer look at TBC Bank Group's balance sheet health here in our report.

Turning Ideas Into Actions

- Gain an insight into the universe of 50 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Burberry Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:BRBY

Burberry Group

Engages in manufacturing, retail, and wholesale of luxury goods under the Burberry brand in the Asia Pacific, Europe, the Middle East, India, Africa, and the Americas.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor