Advertisement

- Finland

- /

- Consumer Durables

- /

- HLSE:YIT

Tread With Caution Around YIT Oyj's (HEL:YIT) 4.4% Dividend Yield

Is YIT Oyj (HEL:YIT) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a stock for its dividend and lose money because the share price falls by more than they earned in dividend payments.

In this case, YIT Oyj likely looks attractive to investors, given its 4.4% dividend yield and a payment history of over ten years. We'd guess that plenty of investors have purchased it for the income. Before you buy any stock for its dividend however, you should always remember Warren Buffett's two rules: 1) Don't lose money, and 2) Remember rule #1. We'll run through some checks below to help with this.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Looking at the data, we can see that 1310% of YIT Oyj's profits were paid out as dividends in the last 12 months. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. YIT Oyj paid out 113% of its free cash flow last year, which we think is concerning if cash flows do not improve. Cash is slightly more important than profit from a dividend perspective, but given YIT Oyj's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

We update our data on YIT Oyj every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

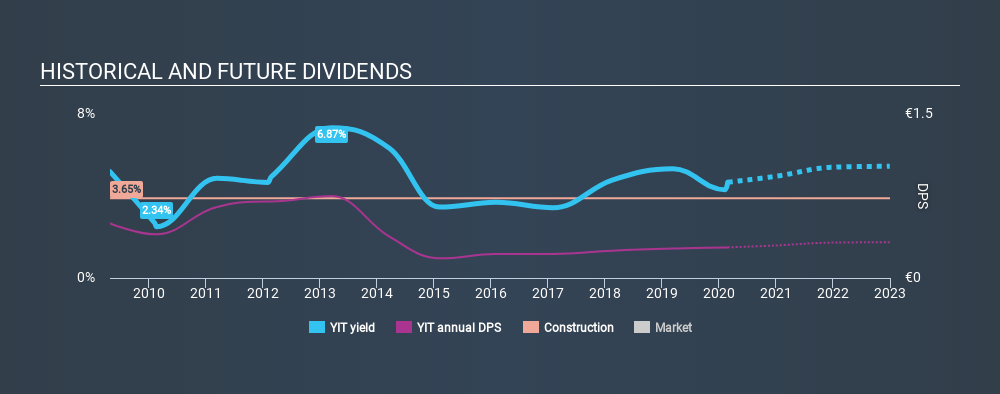

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of YIT Oyj's dividend payments. This dividend has been unstable, which we define as having been cut one or more times over this time. During the past ten-year period, the first annual payment was €0.50 in 2010, compared to €0.28 last year. This works out to be a decline of approximately 5.6% per year over that time. YIT Oyj's dividend has been cut sharply at least once, so it hasn't fallen by 5.6% every year, but this is a decent approximation of the long term change.

We struggle to make a case for buying YIT Oyj for its dividend, given that payments have shrunk over the past ten years.

Dividend Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Over the past five years, it looks as though YIT Oyj's EPS have declined at around 46% a year. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and YIT Oyj's earnings per share, which support the dividend, have been anything but stable.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. We're a bit uncomfortable with YIT Oyj paying out a high percentage of both its cashflow and earnings. Earnings per share are down, and YIT Oyj's dividend has been cut at least once in the past, which is disappointing. There are a few too many issues for us to get comfortable with YIT Oyj from a dividend perspective. Businesses can change, but we would struggle to identify why an investor should rely on this stock for their income.

Given that earnings are not growing, the dividend does not look nearly so attractive. Businesses can change though, and we think it would make sense to see what analysts are forecasting for the company.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About HLSE:YIT

YIT Oyj

Provides construction services in Finland, Estonia, Lithuania, Latvia, Czechia, Slovakia, and Poland.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on KKR ·

Incluso con un colapso brutal del crédito KKR mantendría beneficios relevantes

Fair Value:US$84.4511.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Microsoft ·

Microsoft no es una apuesta. Es una franquicia global de la que se puede ser socio durante décadas.

Fair Value:US$497.815.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥1.91k8.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative