Advertisement

- Singapore

- /

- Specialty Stores

- /

- SGX:AGS

These 4 Measures Indicate That Hour Glass (SGX:AGS) Is Using Debt Safely

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that The Hour Glass Limited (SGX:AGS) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Hour Glass

What Is Hour Glass's Debt?

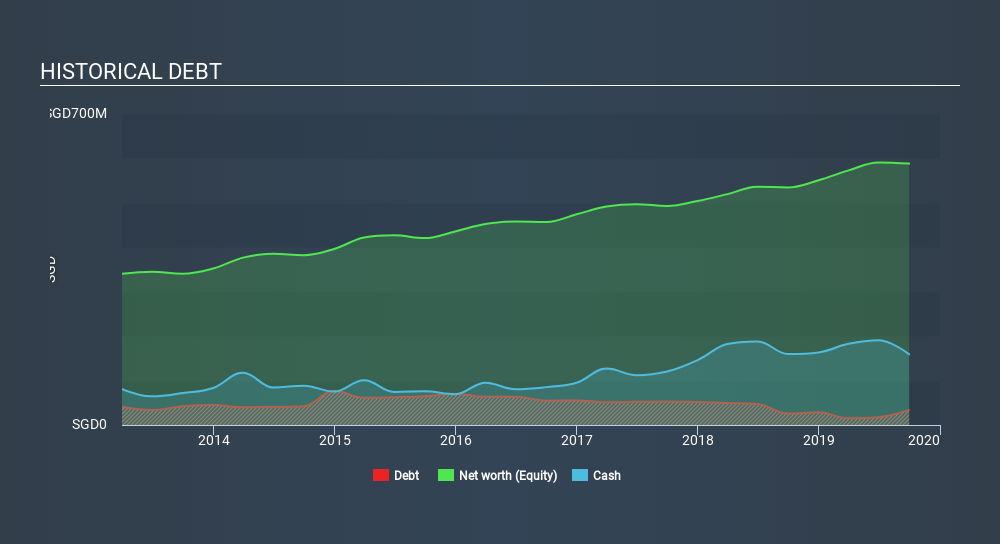

As you can see below, at the end of September 2019, Hour Glass had S$33.9m of debt, up from S$25.7m a year ago. Click the image for more detail. But on the other hand it also has S$159.1m in cash, leading to a S$125.2m net cash position.

How Healthy Is Hour Glass's Balance Sheet?

The latest balance sheet data shows that Hour Glass had liabilities of S$107.6m due within a year, and liabilities of S$95.9m falling due after that. Offsetting these obligations, it had cash of S$159.1m as well as receivables valued at S$19.2m due within 12 months. So it has liabilities totalling S$25.2m more than its cash and near-term receivables, combined.

Of course, Hour Glass has a market capitalization of S$514.7m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Hour Glass boasts net cash, so it's fair to say it does not have a heavy debt load!

And we also note warmly that Hour Glass grew its EBIT by 20% last year, making its debt load easier to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Hour Glass's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Hour Glass may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Hour Glass generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Hour Glass has S$125.2m in net cash. The cherry on top was that in converted 85% of that EBIT to free cash flow, bringing in S$54m. So is Hour Glass's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Hour Glass would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SGX:AGS

Hour Glass

An investment holding company, engages in the retailing and distribution of watches, jewellry, and other luxury products in Singapore, Hong Kong, Japan, Australia, New Zealand, Malaysia, Thailand, and Vietnam.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.0% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

24 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.7% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

CO

Coward_Nutlick on Elicio Therapeutics ·

Very Bullish

Fair Value:US$10090.1% undervalued

20 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

KA

kapirey on KKR ·

Incluso con un colapso brutal del crédito KKR mantendría beneficios relevantes

Fair Value:US$84.4512.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Microsoft ·

Microsoft no es una apuesta. Es una franquicia global de la que se puede ser socio durante décadas.

Fair Value:US$497.815.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.9% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6118.3% undervalued

1192 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative