Advertisement

- United Kingdom

- /

- Personal Products

- /

- LSE:PZC

Should You Use PZ Cussons's (LON:PZC) Statutory Earnings To Analyse It?

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. Today we'll focus on whether this year's statutory profits are a good guide to understanding PZ Cussons (LON:PZC).

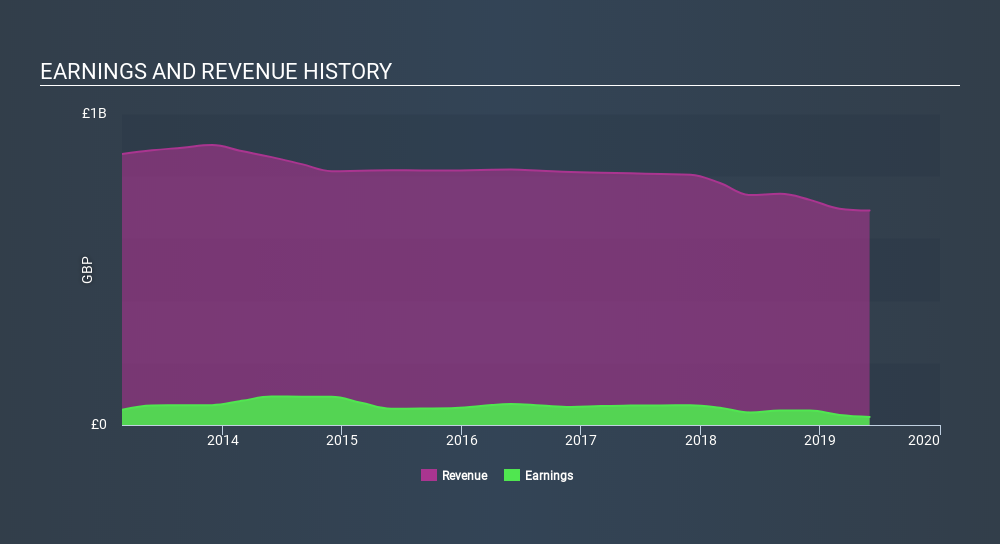

We like the fact that PZ Cussons made a profit of UK£26.1m on its revenue of UK£689.4m, in the last year. The chart below shows that both revenue and profit have declined over the last three years.

View our latest analysis for PZ Cussons

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. This article will focus on the impact unusual items have had on PZ Cussons's statutory earnings. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

How Do Unusual Items Influence Profit?

For anyone who wants to understand PZ Cussons's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit was reduced by UK£37m due to unusual items. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. PZ Cussons took a rather significant hit from unusual items in the year to May 2019. As a result, we can surmise that the unusual items made its statutory profit significantly weaker than it would otherwise be.

Our Take On PZ Cussons's Profit Performance

As we mentioned previously, the PZ Cussons's profit was hampered by unusual items in the last year. Based on this observation, we consider it possible that PZ Cussons's statutory profit actually understates its earnings potential! On the other hand, its EPS actually shrunk in the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. While it's really important to consider how well a company's statutory earnings represent its true earnings power, it's also worth taking a look at what analysts are forecasting for the future. So feel free to check out our free graph representing analyst forecasts.

This note has only looked at a single factor that sheds light on the nature of PZ Cussons's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:PZC

PZ Cussons

Manufactures, distributes, markets, and sells baby, beauty, and hygiene products in Europe, the Asia Pacific, the Americas, and Africa.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Ares Strategic Mining ·

Ares Strategic Mining: $250M Pentagon Contract vs C$76M Market Cap

Fair Value:CA$0.9371.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DS

DS2invest on PayPal Holdings ·

PayPal: Undervalued Cash Flow Machine or Value Trap?

Fair Value:US$69.0318.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MI

MineStackr on AbraSilver Resource ·

NAV $4B CAD

Fair Value:CA$3661.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0