Advertisement

Should BrasilAgro - Companhia Brasileira de Propriedades Agrícolas (BVMF:AGRO3) Be Part Of Your Dividend Portfolio?

Today we'll take a closer look at BrasilAgro - Companhia Brasileira de Propriedades Agrícolas (BVMF:AGRO3) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

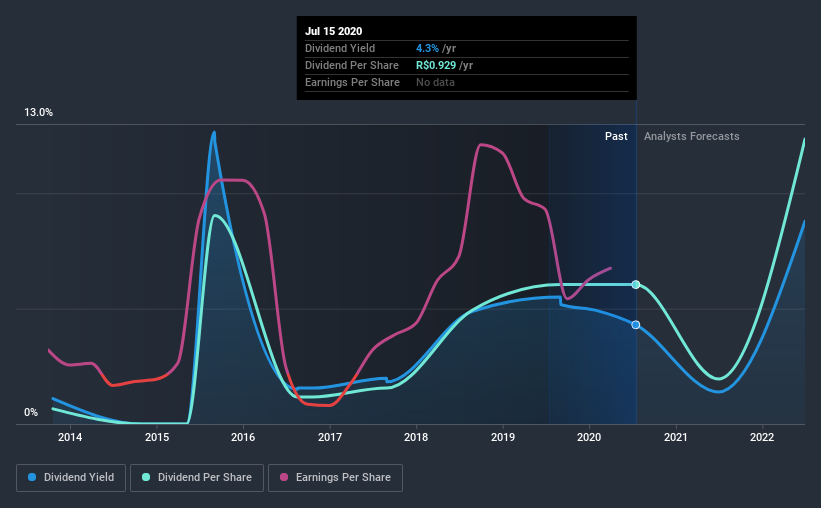

With a seven-year payment history and a 4.3% yield, many investors probably find BrasilAgro - Companhia Brasileira de Propriedades Agrícolas intriguing. We'd agree the yield does look enticing. There are a few simple ways to reduce the risks of buying BrasilAgro - Companhia Brasileira de Propriedades Agrícolas for its dividend, and we'll go through these below.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Looking at the data, we can see that 44% of BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's profits were paid out as dividends in the last 12 months. A medium payout ratio strikes a good balance between paying dividends, and keeping enough back to invest in the business. Plus, there is room to increase the payout ratio over time.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. The company paid out 84% of its free cash flow as dividends last year, which is adequate, but reduces the wriggle room in the event of a downturn. It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Is BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's Balance Sheet Risky?

As BrasilAgro - Companhia Brasileira de Propriedades Agrícolas has a meaningful amount of debt, we need to check its balance sheet to see if the company might have debt risks. A rough way to check this is with these two simple ratios: a) net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and b) net interest cover. Net debt to EBITDA measures total debt load relative to company earnings (lower = less debt), while net interest cover measures the ability to pay interest on the debt (higher = greater ability to pay interest costs). With net debt of 2.42 times its EBITDA, BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's debt burden is within a normal range for most listed companies.

We calculated its interest cover by measuring its earnings before interest and tax (EBIT), and dividing this by the company's net interest expense. Net interest cover of 7.87 times its interest expense appears reasonable for BrasilAgro - Companhia Brasileira de Propriedades Agrícolas, although we're conscious that even high interest cover doesn't make a company bulletproof.

Consider getting our latest analysis on BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's financial position here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. Looking at the data, we can see that BrasilAgro - Companhia Brasileira de Propriedades Agrícolas has been paying a dividend for the past seven years. It's good to see that BrasilAgro - Companhia Brasileira de Propriedades Agrícolas has been paying a dividend for a number of years. However, the dividend has been cut at least once in the past, and we're concerned that what has been cut once, could be cut again. During the past seven-year period, the first annual payment was R$0.1 in 2013, compared to R$0.9 last year. Dividends per share have grown at approximately 37% per year over this time. The dividends haven't grown at precisely 37% every year, but this is a useful way to average out the historical rate of growth.

So, its dividends have grown at a rapid rate over this time, but payments have been cut in the past. The stock may still be worth considering as part of a diversified dividend portfolio.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Strong earnings per share (EPS) growth might encourage our interest in the company despite fluctuating dividends, which is why it's great to see BrasilAgro - Companhia Brasileira de Propriedades Agrícolas has grown its earnings per share at 11% per annum over the past five years. Earnings per share have been growing at a good rate, and the company is paying less than half its earnings as dividends. We generally think this is an attractive combination, as it permits further reinvestment in the business.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. BrasilAgro - Companhia Brasileira de Propriedades Agrícolas's dividend payout ratios are within normal bounds, although we note its cash flow is not as strong as the income statement would suggest. Next, earnings growth has been good, but unfortunately the dividend has been cut at least once in the past. Overall we think BrasilAgro - Companhia Brasileira de Propriedades Agrícolas is an interesting dividend stock, although it could be better.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 4 warning signs for BrasilAgro - Companhia Brasileira de Propriedades Agrícolas that investors should know about before committing capital to this stock.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you’re looking to trade BrasilAgro - Companhia Brasileira de Propriedades Agrícolas, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BrasilAgro - Companhia Brasileira de Propriedades Agrícolas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:AGRO3

BrasilAgro - Companhia Brasileira de Propriedades Agrícolas

Engages in the acquisition, development, exploration, and sale of agricultural activities in Brazil, Paraguay, and Bolivia.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.5% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|13.0% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.5% undervalued

AG

Community Contributor