- United States

- /

- Software

- /

- NYSE:S

SentinelOne (NYSE:S) Reports Increased Sales Despite Larger Net Loss; Announces US$200 Million Buyback

Reviewed by Simply Wall St

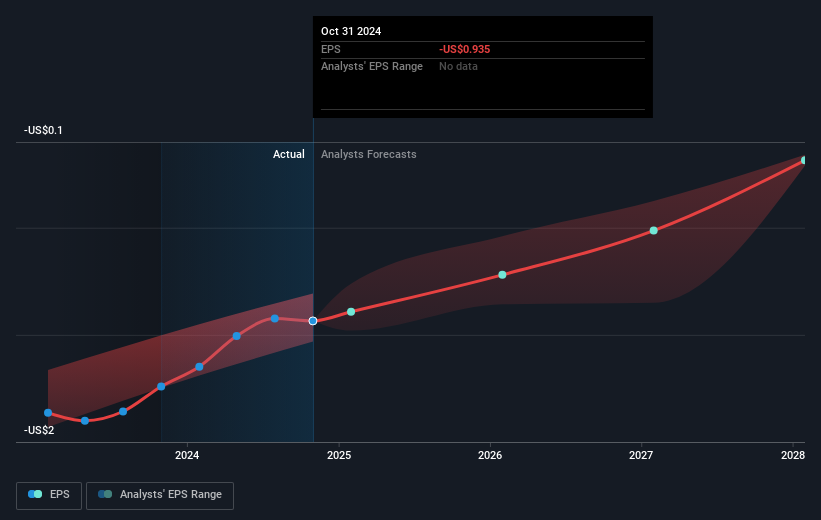

SentinelOne (NYSE:S) recently announced a $200 million share buyback program and delivered its Q1 2025 financial results, showing increased sales but a higher net loss compared to last year. These announcements coincide with mixed market movements, where strong Nvidia earnings buoyed the tech sector, while uncertainties linger due to legal action against Trump tariffs. Despite a challenging financial report featuring rising losses, SentinelOne's commitment to share repurchase might have provided support to its stock price. Overall, the company's 6.55% price increase aligns with broader market trends, particularly within technology stocks, which have seen fluctuations amid evolving trade policy tensions.

The announcement of a $200 million share buyback by SentinelOne, amidst rising losses, indicates a commitment to supporting its stock price, which aligns with broader tech sector trends. However, over the past year, the company's total return, including share price and dividends, experienced a 5.07% decline, reflecting challenges in maintaining investor confidence despite a recent 6.55% price gain. This decline contrasts with the US Software industry's 17.2% increase over the same period, suggesting SentinelOne has underperformed compared to its peers. This underperformance underscores the pressure on the company to leverage its AI-native cybersecurity transformation to drive growth.

SentinelOne's partnerships with Lenovo and MSSPs aim to expand its market reach and are expected to bolster revenue growth. Nonetheless, skepticism remains regarding earnings forecasts, as analysts are not predicting profitability in the near term. The company's current share price, US$18.78, stands about 22.8% below the consensus analyst price target of US$24.33, suggesting potential room for appreciation if SentinelOne's strategic initiatives translate into tangible financial improvements. Additionally, the price target's reliance on reaching US$1.5 billion in revenue by 2028 places emphasis on the company's ability to sustain its growth trajectory and improve profit margins over time. The strategic focus on AI innovations and phasing out legacy products could enhance efficiencies, but these efforts need to translate into measurable financial benefits.

Our valuation report here indicates SentinelOne may be undervalued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:S

SentinelOne

Operates as a cybersecurity provider in the United States and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)