Advertisement

- Hong Kong

- /

- Industrials

- /

- SEHK:1

Returns On Capital - An Important Metric For CK Hutchison Holdings (HKG:1)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So on that note, CK Hutchison Holdings (HKG:1) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on CK Hutchison Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

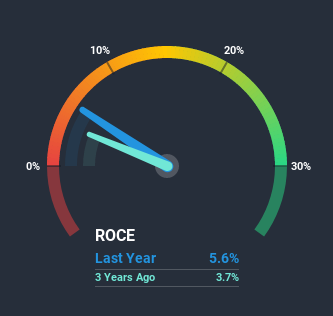

0.056 = HK$59b ÷ (HK$1.2t - HK$143b) (Based on the trailing twelve months to June 2020).

Therefore, CK Hutchison Holdings has an ROCE of 5.6%. In absolute terms, that's a low return, but it's much better than the Industrials industry average of 4.3%.

Check out our latest analysis for CK Hutchison Holdings

Above you can see how the current ROCE for CK Hutchison Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Can We Tell From CK Hutchison Holdings' ROCE Trend?

CK Hutchison Holdings' ROCE growth is quite impressive. Looking at the data, we can see that even though capital employed in the business has remained relatively flat, the ROCE generated has risen by 897% over the last five years. So it's likely that the business is now reaping the full benefits of its past investments, since the capital employed hasn't changed considerably. On that front, things are looking good so it's worth exploring what management has said about growth plans going forward.

The Key Takeaway

To sum it up, CK Hutchison Holdings is collecting higher returns from the same amount of capital, and that's impressive. And since the stock has fallen 42% over the last five years, there might be an opportunity here. So researching this company further and determining whether or not these trends will continue seems justified.

One more thing to note, we've identified 2 warning signs with CK Hutchison Holdings and understanding them should be part of your investment process.

While CK Hutchison Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading CK Hutchison Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1

CK Hutchison Holdings

An investment holding company, primarily operates in ports and related services, retail, infrastructure, and telecommunications businesses in Hong Kong, Mainland China, Europe, Canada, Asia, Australia, and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor