Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that ReadyTech Holdings Limited (ASX:RDY) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for ReadyTech Holdings

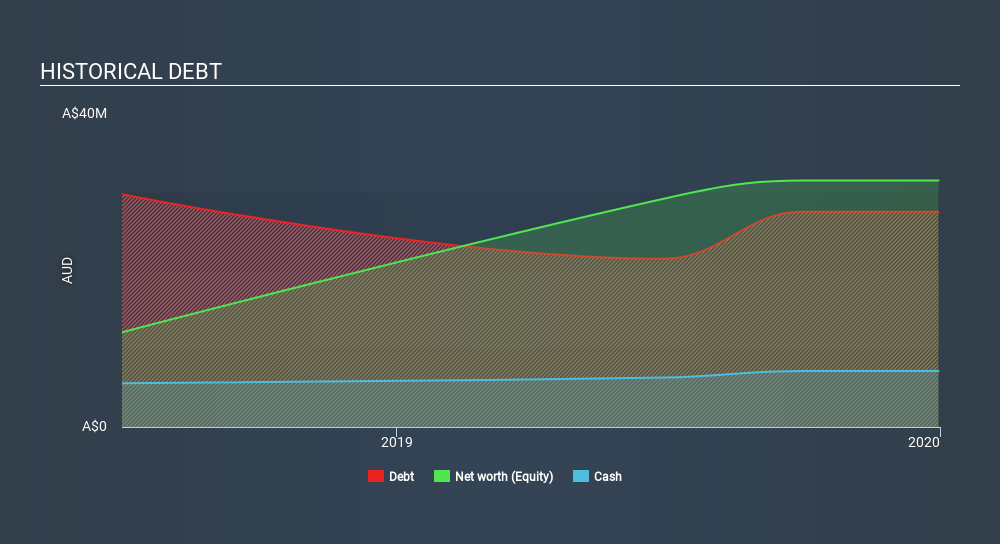

What Is ReadyTech Holdings's Debt?

As you can see below, at the end of December 2019, ReadyTech Holdings had AU$27.5m of debt, up from AU$21.5m a year ago. Click the image for more detail. On the flip side, it has AU$7.15m in cash leading to net debt of about AU$20.3m.

How Healthy Is ReadyTech Holdings's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that ReadyTech Holdings had liabilities of AU$22.6m due within 12 months and liabilities of AU$28.9m due beyond that. Offsetting these obligations, it had cash of AU$7.15m as well as receivables valued at AU$3.92m due within 12 months. So it has liabilities totalling AU$40.5m more than its cash and near-term receivables, combined.

This deficit isn't so bad because ReadyTech Holdings is worth AU$128.0m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

ReadyTech Holdings shareholders face the double whammy of a high net debt to EBITDA ratio (6.8), and fairly weak interest coverage, since EBIT is just 1.6 times the interest expense. This means we'd consider it to have a heavy debt load. One redeeming factor for ReadyTech Holdings is that it turned last year's EBIT loss into a gain of AU$2.7m, over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine ReadyTech Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, ReadyTech Holdings's free cash flow amounted to 35% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both ReadyTech Holdings's interest cover and its track record of managing its debt, based on its EBITDA, make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. Once we consider all the factors above, together, it seems to us that ReadyTech Holdings's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for ReadyTech Holdings (of which 1 is concerning!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ASX:RDY

ReadyTech Holdings

Provides technology-based solutions in Australia and New Zealand, the United Kingdom, and the United States of America.

Reasonable growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WA

wahyud on Perusahaan Perkebunan London Sumatra Indonesia ·

LSIP Revenue to Rise a Whopping 43.92% Amid Market Dynamics

Fair Value:Rp3.6k63.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Charoen Pokphand Indonesia ·

Charoen Pokphand Indonesia will soar with a 12.94% growth and a 10.67x future P/E

Fair Value:Rp4.53k4.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Medco Energi Internasional ·

Medco Energi's Revenue Will Increase by 2.45% Doors Opening

Fair Value:Rp1.75k23.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative