Advertisement

- United States

- /

- Software

- /

- NasdaqGM:RPD

Rapid7 (NASDAQ:RPD) Is Making Moderate Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Rapid7, Inc. (NASDAQ:RPD) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Rapid7

How Much Debt Does Rapid7 Carry?

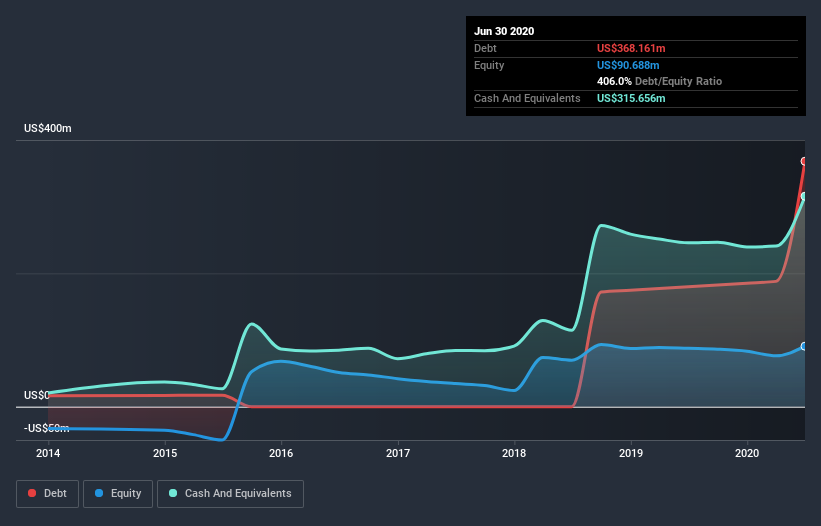

As you can see below, at the end of June 2020, Rapid7 had US$368.2m of debt, up from US$179.8m a year ago. Click the image for more detail. On the flip side, it has US$315.7m in cash leading to net debt of about US$52.5m.

How Strong Is Rapid7's Balance Sheet?

We can see from the most recent balance sheet that Rapid7 had liabilities of US$280.0m falling due within a year, and liabilities of US$489.7m due beyond that. Offsetting these obligations, it had cash of US$315.7m as well as receivables valued at US$78.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$375.7m.

Given Rapid7 has a market capitalization of US$3.23b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Rapid7 can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Rapid7 reported revenue of US$368m, which is a gain of 30%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Even though Rapid7 managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. To be specific the EBIT loss came in at US$57.1m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through US$18.7m of cash over the last year. So suffice it to say we do consider the stock to be risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Rapid7 (including 1 which is makes us a bit uncomfortable) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading Rapid7 or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGM:RPD

Rapid7

Provides cybersecurity software and services under the Rapid7, Nexpose, and Metasploit brand names.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

45 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

65 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

AN

AnimalDoctorKwon on Kuros Biosciences ·

How a Mispriced Medtech Engine is Disrupting $5,000 Bone Graft Giants.

Fair Value:US$342.1892.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Rezolve AI ·

⚡ Two-Minute Drill: Rezolve AI - The AI That Doesn't Recommend Products. It Buys Them.

Fair Value:US$80.7897.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Netcall ·

⚡ Two-Minute Drill: Netcall PLC - This £200M AI Stock Is Already Running the NHS

Fair Value:UK£2.1745.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

81 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

185 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Trending Discussion

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0