- India

- /

- Diversified Financial

- /

- NSEI:PFS

PTC India Financial Services Limited's (NSE:PFS) Price Is Right But Growth Is Lacking

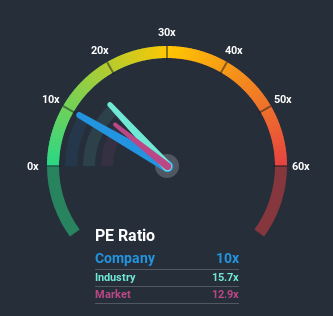

When close to half the companies in India have price-to-earnings ratios (or "P/E's") above 13x, you may consider PTC India Financial Services Limited (NSE:PFS) as an attractive investment with its 10x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

For example, consider that India Financial Services' financial performance has been poor lately as it's earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for India Financial Services

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as India Financial Services' is when the company's growth is on track to lag the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 40%. The last three years don't look nice either as the company has shrunk EPS by 71% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Comparing that to the market, which is predicted to shrink 0.6% in the next 12 months, the company's downward momentum is still inferior based on recent medium-term annualised earnings results.

With this information, it's not too hard to see why India Financial Services is trading at a lower P/E in comparison. Nonetheless, with earnings going quickly in reverse, it's not guaranteed that the P/E has found a floor yet. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability, which would be difficult to do with the current market outlook.

What We Can Learn From India Financial Services' P/E?

The price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of India Financial Services revealed its sharp three-year contraction in earnings is contributing to its low P/E, given the market is set to shrink less severely. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Although, we would be concerned whether the company can even maintain its medium-term level of performance under these tough market conditions. For now though, it's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware India Financial Services is showing 5 warning signs in our investment analysis, and 1 of those can't be ignored.

If P/E ratios interest you, you may wish to see this free collection of other companies that have grown earnings strongly and trade on P/E's below 20x.

If you’re looking to trade India Financial Services, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:PFS

PTC India Financial Services

A non-banking finance company, provides various financing solutions primarily in India.

Adequate balance sheet and slightly overvalued.