Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGM:EVER

Market Sentiment Around Loss-Making EverQuote, Inc. (NASDAQ:EVER)

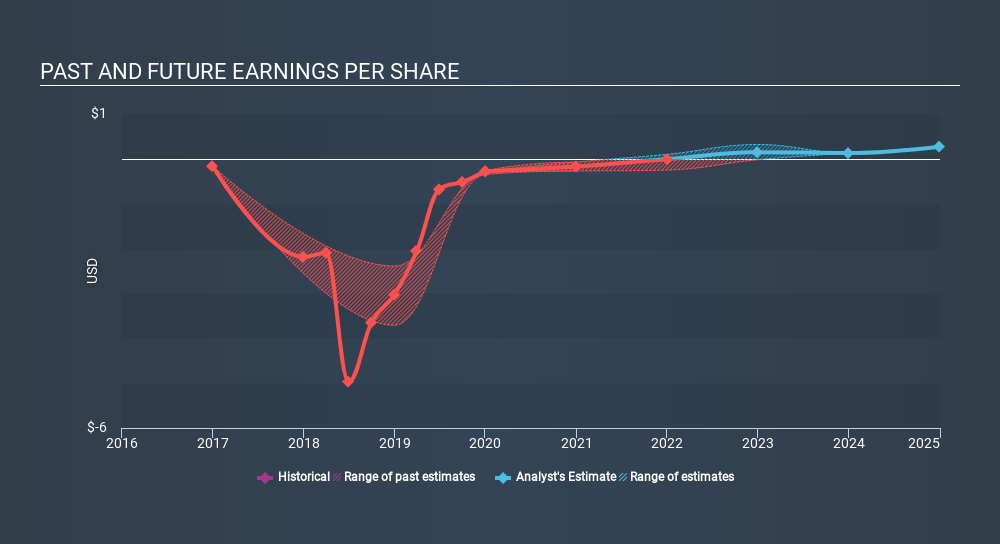

EverQuote, Inc.'s (NASDAQ:EVER): EverQuote, Inc. operates an online marketplace for insurance shopping in the United States. The US$1.0b market-cap company announced a latest loss of -US$7.1m on 31 December 2019 for its most recent financial year result. As path to profitability is the topic on EVER’s investors mind, I’ve decided to gauge market sentiment. I’ve put together a brief outline of industry analyst expectations for EVER, its year of breakeven and its implied growth rate.

Check out our latest analysis for EverQuote

According to the 8 industry analysts covering EVER, the consensus is breakeven is near. They expect the company to post a final loss in 2021, before turning a profit of US$4.2m in 2022. So, EVER is predicted to breakeven approximately 2 years from now. How fast will EVER have to grow each year in order to reach the breakeven point by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 68% year-on-year, on average, which is rather optimistic! If this rate turns out to be too aggressive, EVER may become profitable much later than analysts predict.

I’m not going to go through company-specific developments for EVER given that this is a high-level summary, though, keep in mind that by and large a high forecast growth rate is not unusual for a company that is currently undergoing an investment period.

One thing I’d like to point out is that EVER has no debt on its balance sheet, which is rare for a loss-making loss-making, growth company, which typically has high debt relative to its equity. EVER currently operates purely off its shareholder funding and has no debt obligation, reducing concerns around repayments and making it a less risky investment.

Next Steps:

There are too many aspects of EVER to cover in one brief article, but the key fundamentals for the company can all be found in one place – EVER’s company page on Simply Wall St. I’ve also compiled a list of pertinent factors you should further research:

- Valuation: What is EVER worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether EVER is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on EverQuote’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGM:EVER

EverQuote

Operates an online marketplace for insurance shopping in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.04612.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on CSL ·

Strong buy. World-leading healthcare company with steady growth

Fair Value:AU$143.1519.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

11 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative